What Will Intel Cut Next?

Revenue Down, Margin Down: Q4 2022

2022 started off with a bang - demand was riding high, tech stocks were up, and Intel were already placing the fruits of its future in a large number of projects and new facilities that relied on that sustained growth rhetoric over a number of years. At the time, Intel (INTC 0.00%↑) CEO Pat Gelsinger stated that the company would be in for a high-investment phase in order to bring it back into the realm of competitive performance in the semiconductor market: the '5 nodes in 4 years' mantra combined with investments in infrastructure and manufacturing continue to be the crux of that leadership messaging, specifically competitive leadership. This record over-investment (following a period of multiple years of under-investment) was set to tax the company in multiple ways, particularly in CapEx and gross margins. At the outset of these plans, Gelsinger and then CFO Davis were pointing to a gross margin in the low 50%, down from Intel's typical mid-to-low 60%. However, the second half of 2022 seems to have caught everyone, not just Intel, by surprise.

There are the macroeconomic factors in play - demand for PC hardware seems to be at a substantial nadir, even when compared to previous cyclical performance. 2022 was expected to be a '360m unit year' for mobile and desktop processors, and all the major companies showcased these assumptions during Q1. However, with the 'ending' of the pandemic, the Russian invasion in Ukraine, and the downturn in the Chinese markets, the worst predictions showcase Q4 to be more on a '200m unit year' pace. That's a substantial cut, and that's not even including sell-through of systems: a lot of major players overbought inventory based on the expected high demand, and so now they're sitting on excess components and buying even fewer to replace that inventory, meaning that 200m units is actually less in sales. The enterprise market is fairing better, however not everything is rosy - even with new CPU launches, enterprise players aren't racing to buy new hardware as even Intel is presenting its assets with an 8-year life in its financials rather than a 5-year life. In the cloud, things are a little different, as cloud players are typically demanding of the new product lines, but Intel continues to state its major partners have digestion of components through late 2022 into 2023. As we'll show later, Intel at least stating it expects China to recover faster than other areas, as this is more of a unique soft spot for the company.

Now on top of all this, running a semiconductor fab (or lots of them), especially on the leading edge process nodes and on the brink of commercializing EUV technology, is a capital-intensive process. You simply can't have a semiconductor fab running below 90% utilization, or it costs money - somewhere in the region of $500-$1000 a minute by some metrics. In order to support that, you need a business model with a high revenue output, and a family of processes with customers that require volume and low overheads. According to some analysts, Intel 7 is a very expensive process, leading to a drop in GMs, coupled with investment in Intel 4, the actual commercialization of EUV for Intel. During a downturn, and a lull in revenue, Intel is spending more on building more capacity. It seems counter-intuitive, and as a result Intel has hedged its bets with investment, such as the 50/50 split with Blackrock on one of its new $20-30b facilities. Interestingly enough, the bare minimum was said about Intel's acquisition of Tower Semiconductor on the call, which should have completed by now.

Rambly thoughts aside, let's get into Intel's Q4 and FY 2022 financial numbers. As always, pretty graphs are here.

In Q4 2022:

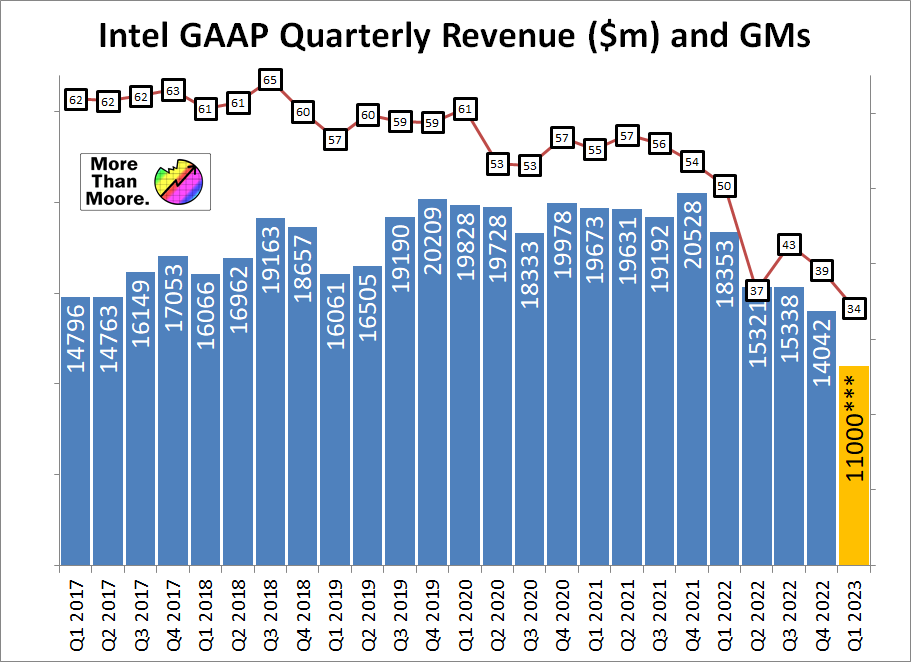

Overall Revenue was $14.0 billion, down 32% YoY and down 9% QoQ

This is Intel's lowest revenue quarter for at least 6 years

Gross Margins were 39.2% GAAP, down 14.5% YoY

Gross Margins were 43.8% Non-GAAP, down 12.1% YoY

This graph is actually fairly interesting as it shows a number of things. Aside from this being Intel's lowest quarter in revenue, it also shows that worldly high of 65% gross margins back in Q3 2018. We can see the drop from 61% to 53% GMs from Q1 2020 to Q2 2020, from which Intel has not yet recovered, but also the period from Q3 2019 to Q1 2022 shows a remarkable consistency in Intel's revenue. This is odd because at this time, a lot of other semi companies were having record revenue. While Intel had a lot of good consecutive quarters, there wasn't any overall revenue growth. Then with the 2022 set of results, the nose has been pitched down. A question I've already been asked is whether Intel is at the bottom or not - that depends on individual division performance.

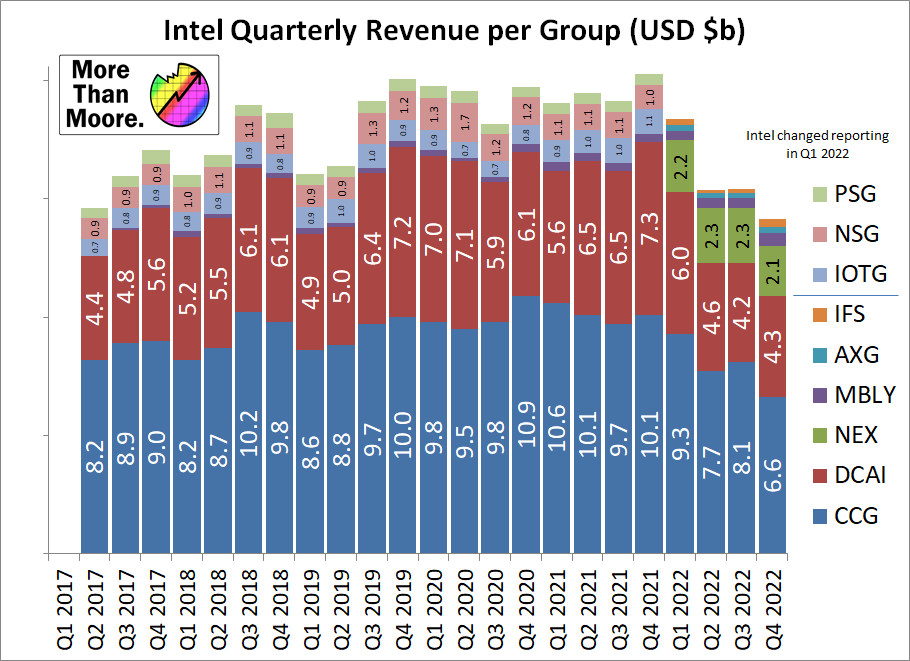

This is a similar graph to the last one, but I've split the revenue up by business group. The numbers are not exact sums here, as it doesn't include revenue that Intel counts outside these groups, such as Intel Capital, IP, and 'other'.

Now Intel changed its accounting strategy in Q1 2022, so that means a few things got moved around. The accelerated computing group, i.e. Graphics under Raja Koduri, was originally part of both CCG (Consumer) and DCG (Datacenter), but became its own division. The Altera acquisition, mostly under DCG, became its own group under PSG (Programmable Solutions), except for the networking side which became NEX. NSG (Non-Volatile Storage) disappeared as Intel sold those assets. Mobileye (MBLY) has been consistent, and IFS is the foundry services. IOTG, for internet of things, dissolved into other groups. I should add that back in the 2017/2018 timeframe, Intel's mantra was to try and become a 'datacentric' business, where consumer and datacenter were about 50/50 in revenue. If you add in all the other departments to DCG/DCAI over that time, it did happen in one or two quarters. Intel has since abandoned this messaging.

So going through each of the departments in Q4 2022:

CCG (Client Computing Group)

Key Products: Alder Lake, Raptor Lake

Key Markets: Desktop, Mobile, Consumer

Revenue $6.6 billion, down 36% YoY and down 19% QoQ

Operating Income $0.7 billion, down 82% YoY

Operating Margin 11%, down from 37% in Q4 2021

In the graph above, this is CCG's worst performing quarter, as this division has been particularly hit by the low demand in the industry. Still, an operating margin of 11% is quite the kick, and Intel puts this down to a few key areas. Aside from the demand lower in consumer and education, there's also the shift towards a product stack on Intel 7, which as we stated before, is a more expensive process node to Intel than 14nm was. The shift to Intel 7 hardware on base costs, coupled with the low sell through due to higher inventory reserves at OEM clients, isn't a great combo. Intel also states that some of the spend listed in CCG is related to the product roadmap - both new designs and new process nodes. It's going to be interesting if using other foundry nodes for its tiles/chiplets in Meteor Lake and beyond are causing those margins to go up, because of the smaller chips, or down, because external foundry plus packaging. I'm going to predict it's exerting negative pressure, and part of that comes down to Intel's tiling strategy, which doesn't seem to take advantage of doubling performance through doubling key tiles (this is deserving of a longer piece to explain what I mean, but tiling has some specific advantages and I fear MTL ignores one of them completely).

DCAI (Datacenter and AI)

Key Products: Ice Lake, Sapphire Rapids, Habana, Ponte Vecchio (ish), Intel Flex, Stratix/Agilex FPGAs

Key Markets: Server, Enterprise, Cloud, Telco, Machine Learning

Revenue $4.3 billion, down 33% YoY, up 2.3% QoQ

Operating Income $0.4 billion, down 84% YoY

Operating Margin 9%, down from 37%

Intel's Q4 for the DCAI was actually better than Q3, which I think is partly down to the introduction of Sapphire Rapids during Q4. (Technically it 'launched' Jan 10th, but top tier orders are taken before this.)

The only problem here is that Sapphire Rapids is at least two years late due to Intel's manufacturing issues that are well documented, as well as the need to continually respin the silicon to fix issues. Intel was ambitious on Sapphire Rapids, with lots of high-performance cores, new DDR5 and PCIe 5 controllers, new accelerators, new security, and a tiling strategy to help create 'one big chip' from 14 little ones. However, walking and running are different actions, and depending on the report, Intel required 7 or 12 respins of Sapphire Rapids to get a sufficient set of features for retail production - typically a large enterprise processor might have three or four, so this was somewhat unprecedented. On top of this, it requires the Intel 7 process node, which as we explained earlier, is an expensive process for Intel. Intel files this under 'higher unit costs', but we have to have a comparison here: Intel's SPR is 1600mm2+ of silicon for 60 cores while AMD's Genoa is ~1000mm2 of silicon for 96 cores and beats Intel by a generation on a number of key workloads. Intel still wins in optimized AI, acceleration, and the key workloads that it has its army of engineers optimize for, but the question I'm continually asked by the wider market is if it is enough? One of the analyst Q&A questions was on the topic of incumbency market share, which in the DC segment is often is led by the incumbent, but this has slowly been eroded for Intel. Intel cites competitive pressure as another reason why DCAI revenues are down.

Also on that list is Intel stating that its total addressable market (TAM) for DCAI is down compared to previous years - Intel has explained a number of TAM values over the years, but didn't provide such a metric this time around. A reducing TAM at the same market share will reduce revenue, but a combined market share reduction compounds the result. Intel was mum on ASPs, which for Sapphire Rapids should be higher, along with performance per dollar, but the angle of competitiveness is an important one.

For other product families, it's a more difficult read. Intel doesn't split out its Habana revenues, and the only big customer it likes to promote is Mobileye and cloud services. Ponte Vecchio, the high-end HPC compute product, is likely not to be revenue positive for a while - despite it also being announced as GPU Max in the Jan 10th launch, initial shipments are still heading to the Aurora supercomputer rather than other potential customers. Common thoughts are that Intel has already lost money on its Aurora project with the delays, and even with it complete the company still might not be in the black. While PVC is an impressive product, and there will be other sales, given the complexity overall, I'm going to have a stab here that even over the lifetime of the product, it probably is not an overall revenue positive play, but more an R&D experiment to pave the way for future multi-tile designs.

Other features like Intel Flex are new and are likely to get a lot of traction in those markets, and the FPGA market for Intel is a slow methodical march to filling out Intel's Agilex family. We're not hearing a lot from the former Programmable Solutions group, as Intel is likely keeping the custom designs it creates with customers under wraps from the public eye.

NEX (Network and Edge)

Key Products: Mount Evans IPU, Tofino, Various Edge Processors

Key Markets: Networking, Edge

Revenue $2.1 billion, down 1% YoY and down 8.7% QoQ

Operating Income $0.058b, down 84% YoY

Operating Margin 3%, down from 17%

While an effective revenue flat quarter for the network business unit, the drop in operating income and margin is considerable. Again, this is another victim to a the high costs associated with Intel's latest process nodes, but also the portfolio is shifting towards the IPU which seems to have got traction with a few key players (including the cloud provider who it was built for). Intel again reiterates that the NEX unit has had a TAM contraction, and the IPU ramp up has actually offset this. We also get the comment about investment in process, however what Intel stated in its prepared remarks was that the Tofino product line will be dissolved, at a time when demand for networking equipment is actually at a high.

Putting the halt on Tofino and future Tofino development falls under Intel's desire to make significant cost savings over the next five years by cutting business units it sees as non critical or not conducive to overall spend, revenues, and margin. Which is a shame, given that Tofino was often at the forefront of new innovations in networking and optics, and was going to be a spearhead for Intel's future optics development. That will now fall to future CPU/GPU integration, which is more of an orthogonal feature and comes with high packaging costs in those segments that might be more price sensitive than most. The latest Tofino chip currently in the market is also the only (we think) network switch silicon with a fully programmable P4 pipeline. This allowed customers to do custom metrics and routing between aggregate switches using their own software that adapts with the silicon, rather than simply a computer program on top. Tofino isn't the first program to be cut by Intel, and it won't be the last.

AXG (Accelerated Computing)

Key Products: Intel Arc GPUs, Development on PVC/Flex

Key Markets: Desktop graphics, laptop graphics

Revenue $0.247 billion, up $2m YoY, up 33.5% QoQ

Operating Income -$441 million, up $200m million YoY

AXG was actually one of the better performing business units, despite being negative to operating income, but it wasn't as negative as the equivalent last year. Intel said that integrated graphics shipments declined over the year, but it's hard to understand what this means: integrated graphics as in on-die, or integrated as in combined in a system as a discrete GPU (desktop or mobile)? It's true that we're not seeing any big systems sold with an Intel discrete GPU inside right now in volume, but integrated graphics weren't Arc anyway, or are sold under CCG, so it's hard to understand what Intel means here. Some of the HPC revenue is also in AXG, and this is the main reason why Intel said revenues were up slightly in the year.

Though again, the bad news is that AXG is being subsumed into other divisions. AXG head Raja Koduri is taking a more overall architectural role, and the different elements of AXG will be labelled under CCG and DCAI in future. Intel states this is because it makes more sense to have those teams work closer with the separate divisions, and even though there's a unified architecture the productization is actually very different. I've said to Intel that externally this feels like Intel is deprioritizing graphics, and when AMD did something similar almost a decade ago, graphics became a second class citizen and they put it back into its own division in order to inject enthusiasm and growth. Intel hasn't been 100% clear on what its AXG strategy is so far, aside from saying that they are still committed to future product lines as announced and they are still on track. Another angle is that it will be easier to merge some of these operating income losses, and give less visibility into the division. I expect that a number of financial analysts will be keeping close track on the top line personnel at AXG to see if they start moving elsewhere, as that could be a future indicator. The opposite is also true.

MBLY (Mobileye)

Key Products: EyeQ4, EyeQ5, EyeQ6, EyeQ Ultra

Key Markets: Automotive

Revenue $0.565 billion, up 59% YoY

Operating Income $0.210 billion, up 71% YoY

A perennial bright spot on Intel's financials during 2022, since its acquisition Mobileye's revenue has grown at a staggering 31.6% CAGR due to the consistent execution and agreements with car manufacturers with the new product ramps of EyeQ and Supervision. Mobileye has had continued deployment success in China, such as with the Geely Zeekr One, and under BU CEO Amnon Shashua, there has been significant revenue flow through on the portfolio. Just to put this into a graph:

It's still unclear if there is a cyclical nature to Mobileye's business and the automotive self-driving market - the Q2 2020 pandemic hit is the biggest divot, but the biggest quarters look to be Q4 and Q1 every year. Mobileye has been acting fairly independently, and a the big consumer of Habana AI processors. With the Mobileye IPO, I can imagine that Intel will leverage the Mobileye value in future if it needs to.

IFS (Intel Foundry Services)

Main Product: Chip manufacturing, packaging, IP and services

Revenue: $0.319 billion, up 30% YoY

Operating Income: -$31 million, down $34 million

As always, big question marks on Intel's Foundry strategy are still to find answers. I think most of the investment community understands the goal is to put all the manufacturing in the hands of IFS, to find external foundry customers to use the capabilities and to sell IP to them, and make IFS be profitable within its own right. While this quarter Intel is saying that automotive orders are a big source of revenue, the operating loss is due to increased spending in R&D. There is a big win here as well, as Intel also stated that it has a customer with a potential >$4b lifetime revenue deal on its upcoming EUV-based Intel 3 process. Given current timelines, that could be starting as early as 2024, though because Intel is saying 'lifetime revenue', that could be spread out over 5-10 years.

The one thing not addressed in the call was the Tower acquisition, which from my side of the fence is going to be a key part of what Intel Foundry Services will eventually morph in to. While Tower's own business has low margins (mid teens%), it does sell almost as many wafers as Intel per year and has hundreds if not thousands of customers, whereas Intel has a handful at most (and most of those are itself). Sure, Tower works on older process nodes, such as 40nm and above, but Tower's management team has experience in managing supply chains with that many customers, which for me is where the true value of the deal is. Sure, Intel can apply the benefits of scale to improve the margins of Tower's core business, and offer it under Intel branding, but that's only part of it all. Intel had expected to close the deal by the end of 2022 or the start of 2023, however China has put the brakes on the deal for now. I was expecting some sort of update on the call regarding Tower, but we only had a single comment on 'we are doing what we can to close the deal'. No timeline there, and none of the analysts probed the situation.

Other numbers and points worth considering

FY 2022, $6.0 billion dividends paid ($1.5b in Q4)

Non-GAAP Free Cash Flow was down $4.1 billion

Net Income was down $700m in Q4

No mention of currency corrections

Depreciable Life change from 5 years to 8 years

$700m liquid cooling research lab cancelled

$1b RISC-V Pathfinder Program cancelled

When Gelsinger initiated this strategy to resteer Intel in the right direction, on the whole it was seen as a positive. I was certainly looking forward to it, however we expected that correction to be as if a boat was steering 30 degrees to the right, and you'd plot a 45-degree correction to slowly get back on track. With the numbers we're seeing, it feels more like a 135-degree drift and it's amazing to see that this is what it's going to take. We've all heard the phrase 'go big or go home', well Gelsinger is going bigger than everyone else it seems. That being said, it has to weather the storm and they've said that it's going to be a rough few years, but the street didn't expect it to be this rough. In particular, a negative net income for the second quarter in a row, free cash flow is expected to decline, but one of the metrics we're seeing a clear dichotomy on is the dividend.

Through the storm, Intel is continuing to pay out a dividend to the tune of $6.0 billion in 2022. A lot of analysts I speak to are saying this is crazy - Intel is suffering overall net losses and net FCF losses while keeping its dividend this high. Typically during a corrective era where revenues and GMs decline, dividends are cut to keep the balance sheet healthy. It annoys investors who aren't getting a return, but it can help the company through rough patches where it needs to with the help of it being brighter on the other side. Dividends remain high if there's still plenty of money in the bank, or some financial leader is looking to bleed the company to the benefit of investors. That last point is somewhat cynical, and a gross simplification, but still.

When questioned on the dividend, Intel stated that it would continue to provide a competitive dividend. Normally that's to give the sense that the company is performing as it should in regular times, but is this a regular time? The CFO stated that the Q1 dividend will remain at 36.5%, similar to previous quarters, and the company remains committed to capital allocation. Again, a number of analysts I track are saying for the second Q in a row (or more) that Intel should cut the dividend.

On the point about currency corrections - while Intel is early in the financial reporting cycle for the quarter, a number of other companies (ASML, IBM, TSMC) have spoken about currency corrections in their financials. The adjustment of certain currencies, such as TWD to USD, have been rapid this quarter, making comparisons in different currencies more difficult, especially with a diversified revenue portfolio. Other companies with a currency mix are reporting up to a 6% difference in some of their financial metrics over the quarter, or 20% over 2022, however Intel didn't state anything on the issue. This could be for a number of reasons, but it's hard to speculate without a breakdown of geographic revenue sources. Also, the depreciable life change from 5 years to 8 years has been highlighted as a way for Intel to present a better picture with its finances.

On the cancellation side, the big downer here was the commitment to the RISC-V Pathfinder program. It technically ran for a few months, and Intel had earmarked $1b to help develop the RISC-V ecosystem for Intel's Foundry Services, with the hopes that it would be the main foundry for future RISC-V customers. It would appear that Intel no longer thinks that it's worth the spend, either because the return wouldn't be sufficient within an expected timeframe, or that the program wouldn't add much to the ecosystem. Some have called this a good cancellation given the finances, although a dividend drop could have paid for it.

Intel Comments on Roadmaps

Before we get onto some of the market forces commentary Intel provided, I want to scope out the updates to the roadmap that Intel also talked about. As we know, Intel's deployment of 10nm and 7nm (or Intel 7) was long and drawn out, then the '5 nodes in 4 years' indicated that Intel was trying to change its slowest update progress in history to its fastest. For those who I've not spoken to directly before or read this newsletter before, it's worth pointing out that when Intel says 5 nodes, it's actually 6 - there's a development node in the middle that won't be productized. But perhaps more important than that, it's not 6 'full' nodes, but rather six 'half' nodes.

The modern way of implementing a semi process is that there's the main base process, and then optimized 'half nodes' are built on top. So you get a full process, then ‘a half’. Intel is doing it slightly differently with its upcoming portfolio, by starting with the half, then adding the rest:

Intel 10nm is a traditional base node with all the features, and Intel 7 is a sub/half node

Intel 4 is really a 0.5 node and only contains features for high performance, not IO beyond SERDES

Intel 3 contains all the features

Intel 20A is really a 0.5 node and only contains features for high perf, not IO beyond SERDES

Intel 18A contains all the features

Classically a foundry would create a node with all the libraries available: high performance, IO, dense SRAMs, etc. What Intel is doing here is that the first node of a generation focuses on performance, and then only on the next half node is it filling out the portfolio of cells and libraries. Intel is doing this for two reasons.

First is that it can take advantage of new process node adjustments on the leakiest part of the design first, but also second is that these initial high-perf starting half-nodes won't actually be externally available until the next one in the stack. So we'll see some of Intel's own products use Intel 4 for example, but external customers will instead use Intel 3, because Intel 3 has all the customer features. Same with 20A being for Intel, and 18A for everyone.

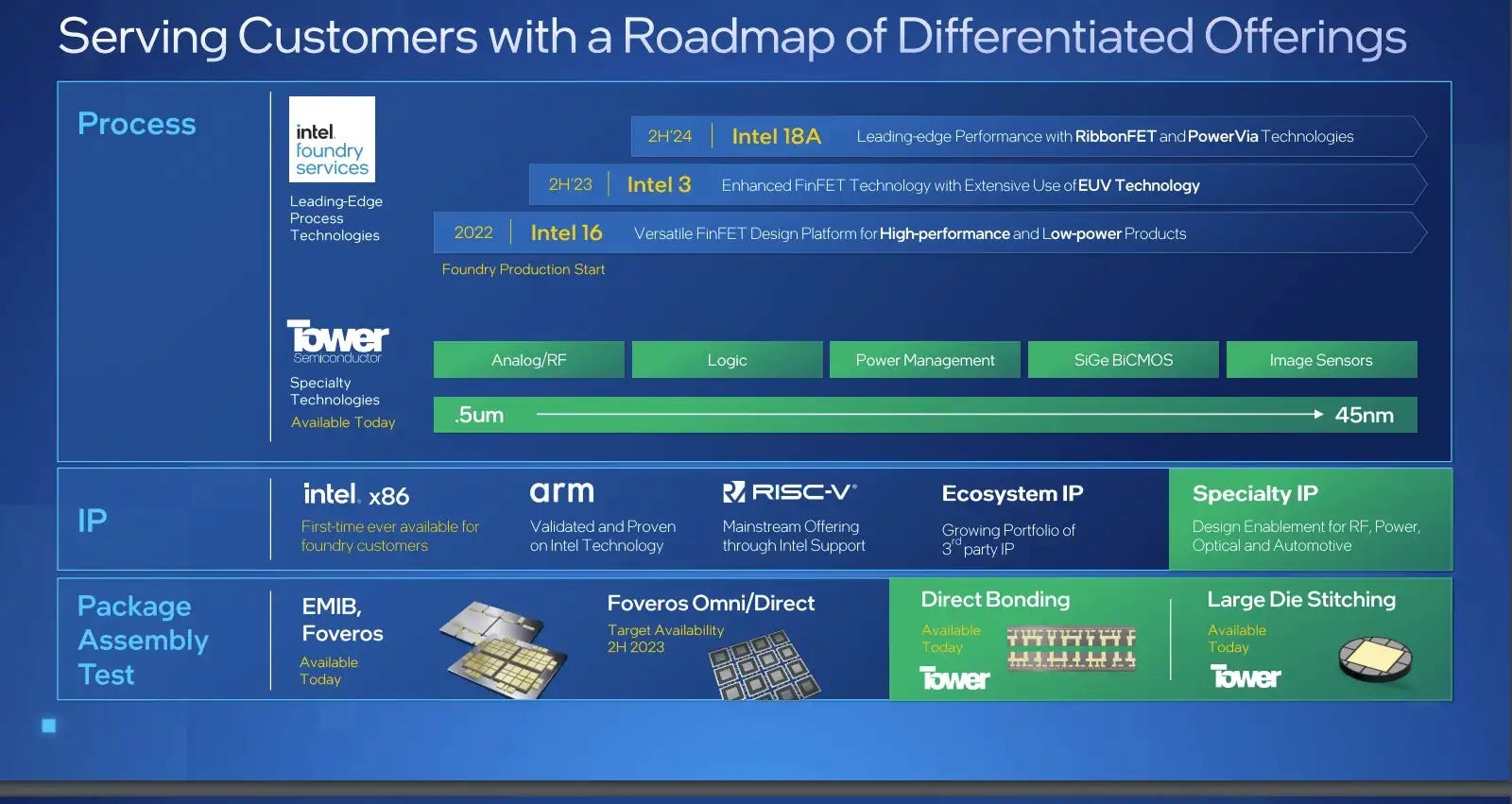

So if you ever see an IFS roadmap, like the one below, and ask why Intel is focusing on Intel 3 and Intel 18A for external customers, this is why. This is also why when you hear '5 nodes in 4 years', think half-nodes, just to put it in line with other foundry nomenclature.

But beyond this, product details.

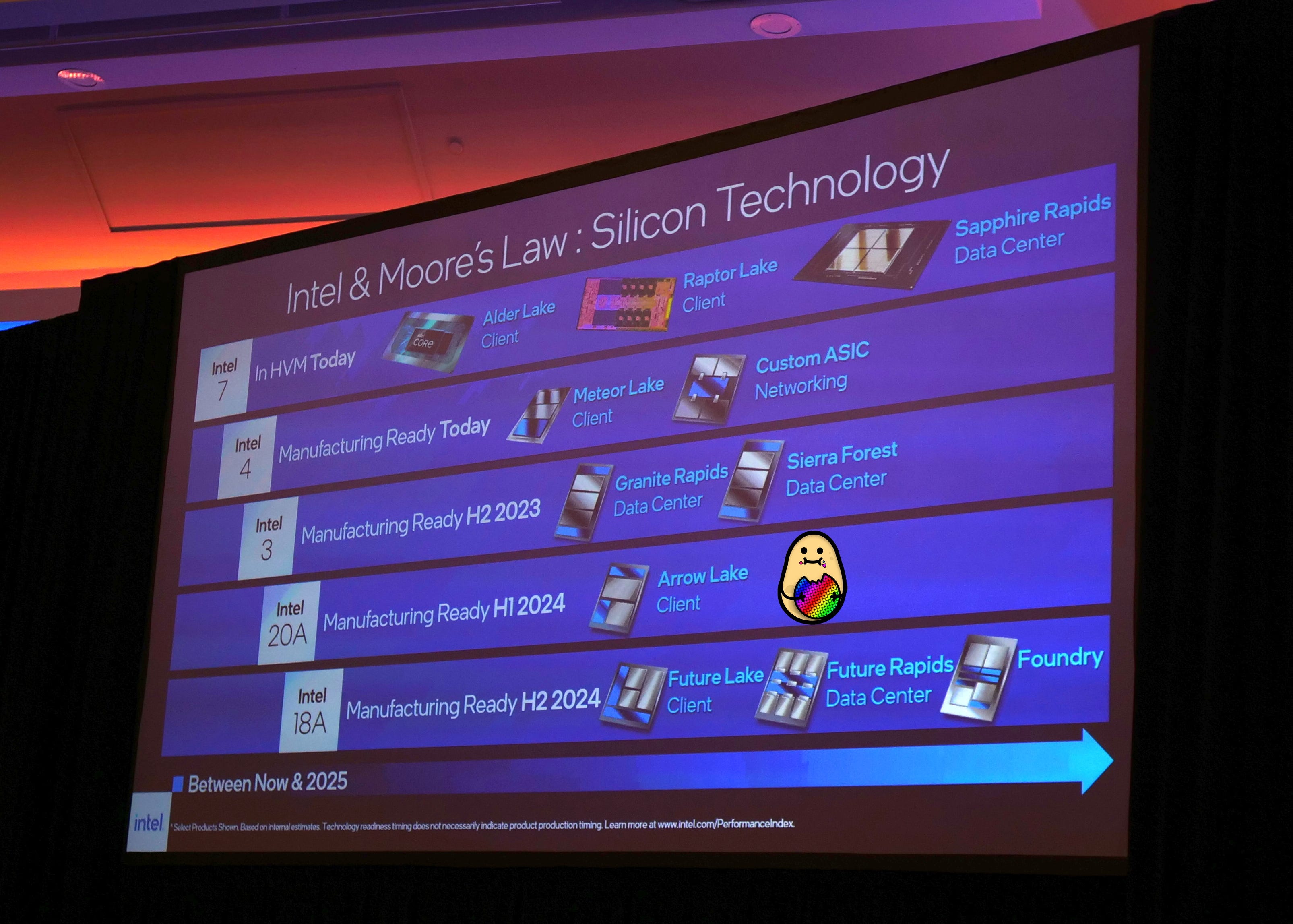

Intel 7 is in high volume manufacturing (Rocket Lake, Sapphire Rapids)

Intel 4 is Manufacturing Ready (Intel-code for ready to start to ramp)

CCG launched Rocket Lake in 2022, and Meteor Lake is on track for 2H2023

CCG's future generation LNL Lunar Lake (2024) has taped out the first tile (other tiles to come later)

CCG LNL is optimized for ultra-low-power and performance, sounds like notebook first

DCAI launched SPR Sapphire Rapids, and EMR Emerald Rapids (socket update) is on track for 2H2023

DCAI EMR Emerald Rapids is already sampling to early customers

DCAI Sapphire Rapids 1 million units shipped by mid-2023

DCAI GNR Granite Rapids and SRF Sierra Forest on Intel 3 are still on track for 2024 ramp

AXG Alchemist Ramp through 2023

20A/18A test chips are taping out

Intel at IEDM 2022, December

Of course any roadmap points are subject to change, but what interested me here most was that 1m unit number for Sapphire Rapids. Intel has maintained the narrative that SPR will be the fastest ramp in Intel history, however if I roll back to the launch of Ice Lake in Q4 2021, Intel mentioned that it shipped 1m units in December alone for Ice Lake. I'm not sure if someone got their numbers crossed somewhere, of if there's an order of magnitude, or something has changed (and SPR isn't the fastest enterprise ramp in Intel history. Perhaps the metric is more in Intel's fastest ramp of wafers consumed rather than chips sold given the size of the big SPR? It's worth noting that some of Intel's competitors often provide an after-earnings call for non-finance press to ask questions, but Intel does not - I might ask the team there to start doing this so we can get some insight into these comments.

2023 Q1 Outlook

Normally with an end-of year financial presentation, there's some commentary on the outlook for the whole of the next year. For this call however, Intel didn't want to say much about its full-year 2023 predictions, aside from some rough metrics:

Consumer market to be nearer 270m FY overall

Some key markets still rough during Q1 and Q2, but returning in Q3 and Q4

Outlook at the end of the year a lot better than the first half

Aside from the consumer market number, there's not much concrete to go on there, and the questions I've had so far from the community is regarding where the bottom is for Intel - are we there yet, or is it Q1? With the numbers given and the comments from Pat and others, Q1 is likely still to be rough, with a potential glimmer in Q2 maybe. Intel did give Q1 guidance:

1Q 2023 Revenue: $10.5 billion to $11.5 billion, down from $18.4 billion in 1Q 2022

1Q GAAP Gross Margin is 34.1%

1Q Operating Margin is expected to be negative.

A midpoint of $11.0 billion means that Intel is effectively at half the revenue of Q4 2021, only six quarters ago, and GMs are down 20%.

Erm, yes. Normally Q1 is a down point cyclically, for example in the consumer market, however Intel just launched new products both on the desktop and in the laptop markets. If revenue is down that much, partly due to the channel inventories being so high, and Intel is projecting for a 270m unit year in 2023, then there needs to be better-than-expected growth in the second half of the year. Any investor looking for a tail-wind with the new product lines is not going to see it in Q1 it seems.

Note that if Intel keeps the same ratio of revenue for CCG:DCAI:NEX etc, this means:

CCG will be at $5.2 billion, down 44.4% YoY

DCAI will be $3.4 billion, down 43.8% YoY

NEX will be $1.6 billion, down 25.3% YoY

MBLY will be $443 million, up 12.3% YoY

'AXG' will be $193 million, down 11.5% YoY

IFS will be $250 million, down 11.7% YoY

However, given the trends, MBLY might be higher than that, pushing the others down. AXG will be in others as well.

Other commentary: What's Next on the Chopping Block, How Does Intel Return to Competitiveness?

Sorry this analysis has been almost 5000 words deep at this point - Intel always has a lot to talk about with all of its business units. We've come about face from the time Intel was talking about TAM expansion, as we're going through a period of market contraction but also there are cuts to Intel's portfolio in order to focus on Intel's key product lines. Tofino is one, but this begs the question, what could be next on the chopping block?

I explore seven different options below the fold for subscribers. Also included will be a description on what I think Intel's main areas of focus should be to return to market competitiveness, with timelines. There's also a transcribed analyst Q&A from the financial call.