NVIDIA 2026 Q1 Financial Results

China Headwind, Networking Tailwind

As we look to close the book on the calendar year Q1 earnings season, we once again find ourselves closing things out with NVIDIA. The company’s quirky earnings calendar, which saw the company wrap up the first quarter of its 2026 fiscal year on April 27th of 2025, is both a boon and a bane for the company. By being shifted a month later than the rest of the industry, NVIDIA doesn’t have to vie for attention amongst a dozen other tech companies all releasing their earnings reports on the same days. But as the closing act for the earnings season, this also means that all eyes are on NVIDIA whether it’s good news or bad news.

Thankfully for NVIDIA, the first quarter of the year is another one to be proud of, with the company once again reporting record revenues. NVIDIA has now logged 9 consecutive quarters of double-digit revenue growth, and with gross margins over 60%, NVIDIA is printing money in a way that few other tech companies are right now.

And while NVIDIA continues to reap the benefits of the rapidly growing AI market – as well as a blockbuster quarter for gaming – Q1’26 will end up going into the record books with an asterisk next to it. With NVIDIA taking a $4.5b charge due to increased US export restrictions that have resulted in NVIDIA’s made-for-China H20 accelerator being banned from China (more on this in a bit), Q1’26 is technically a troubled quarter for NVIDIA. So to deliver record revenue despite those headwinds is a testament to the strong (if not unrelenting) growth of the company, which in turn has allowed it to shrug off a major market disruption as barely a speedbump.

As a result, for Q1’26 NVIDIA has delivered its best quarter ever. Again.

Key Takeaways (GAAP)

💵 Q1 Revenue, $44.1b, up 69% YoY from $26.0b and up 12% QoQ

📈 Q1 Gross Margin at 60.5%, down 17.9pp YoY and down 12.5pp QoQ

💰 Q1 Net Income of $18.8b, up 26% YoY from $14.9b and down 15% QoQ

🪙 Q1 EPS $0.76, up 27% YoY, down 15% QoQ

Highlights

💵 Record Quarterly Revenue

💵 Record Data Center Revenue

💵 Record Gaming Revenue

Financial Overview

Opening up NVIDIA’s 2026 fiscal year, for Q1’26 the company booked a record $44.1b in revenue. Compared to Q1’25, that’s a hefty 69% year-over-year increase in revenue. And while this is a bit slower than the year-ago quarter, when revenue growth was a gobsmacking 262%, that’s about the worst you can say about NVIDIA’s financial performance.

All told, this is now the 9th consecutive quarter of revenue growth for the company. NVIDIA hasn’t seen a quarterly decline in revenue since Q3’23, repeatedly bucking the trend of seasonality that impacts most other mature tech companies. Especially in the first quarter of the year, it’s notable that NVIDIA is pulling off quarterly revenue growth when most other companies pull back from their peak Q4 results.

Going beyond NVIDIA’s top-line revenue, the rest of NVIDIA’s financials are quite strong as well. NVIDIA’s non-GAAP gross margin of 61% is a distinct drop for a company that in recent quarters has been holding to better than 70% margins, though it’s still highly profitable on the whole. As a result, NVIDIA was able to book $18.8b in net income for the quarter, which was up 26% over the year-ago quarter.

As mentioned previously, the albatross around NVIDIA’s neck for their most recent quarter has been their H20 accelerators. Owing to ongoing US export restrictions on high performance accelerators to China, NVIDIA re-designed the Hopper architecture into a product called the H20, specifically for the Chinese market, essentially designing as powerful an accelerator as US export restrictions would allow. However, following updated US export restrictions that went into effect in April, the H20 now requires a license to be exported to China – all but blocking further shipments there.

As a result, NVIDIA’s top-line revenue and bottom-line profitability both took separate hits in the most recent quarter. According to NVIDIA, had the new export restrictions not gone into effect, the company would have been able to ship another $2.6b in H20 accelerators for Q1’26. Meanwhile, the company is separately taking a $4.5b charge for H20 excess inventory and purchase obligations, reflecting the cost of building H20 accelerators they can’t immediately sell.

Because of the unusual – if not capricious – nature of the H20 export restrictions, NVIDIA is being very quick to note the situation in their earnings report, as well as outlining where their results would be if they didn’t need to take the H20 write-down. Excluding the H20, NVIDIA’s gross margin for Q1’26 would have been 71.3%, which is roughly in line with their historical performance. Which is to say that, NVIDIA’s one-off export problems aside, their core business remains sound.

Overall, NVIDIA’s Q1’26 performance was a mix of meeting and beating the company’s guidance from the start of the quarter. NVIDIA was initially projecting $43b +/- $860m in revenue, so NVIDIA’s $44.1b in revenue beat even the high-end of their revenue projections – and that’s despite the loss of sales of H20 accelerators. Meanwhile NVIDIA’s gross margins (sans H20) were once again dead on: the company would have hit 71.3% for their non-GAAP margin, coming in at the higher-end of their forecast range.

Meanwhile, as pointed out by Ian, NVIDIA’s free cash flow is quickly growing as well. The company is up to $26.1b in free cash flow, a $11.2b improvement over Q1’25. Altogether, NVIDIA now has $53.7b of cash and marketable securities on-hand, a $22.3b increase over the year-ago quarter. Even with the company’s rapid growth, NVIDIA is struggling to spend all of the cash it’s quickly amassing. Which means that CEO Jensen Huang may need to take up diving lessons, as his company is now swimming in cash.

Data Center: Blackwell, Hopper, & Grace

💵 Q1 Revenue $39.1b, up 73% YoY

For Q1’26, NVIDIA’s flagship market platform has once again delivered exceptional growth. Altogether, NVIDIA shipped $39.1b in DC products for the quarter, driving NVIDIA’s explosive growth and potent profitability.

Surprisingly, even with this continued NVIDIA’s data center revenue as a percentage of total revenue has actually fallen from the previous quarter, dropping below the 90% mark to 88.7%. This reflects no specific weakness on the data center side, but rather a strong quarter for NVIDIA’s gaming business unit, allowing it to claw back some of its revenue share. But even with this shift, NVIDIA remains primarily a data center company, with some side hobbies in gaming, automotive, and professional visualization.

Driving their record business unit revenue, Q1 saw the continued ramping of products based on NVIDIA’s Blackwell architecture, such as GB200, B100, and B200, as well as the company’s massive rack-scale NVL72 systems, which are now in full production. And while it remains farther down the line, NVIDIA has their eye on their mid-generation upgraded Blackwell chips, Blackwell Ultra and Grace Blackwell GB300 compute nodes.

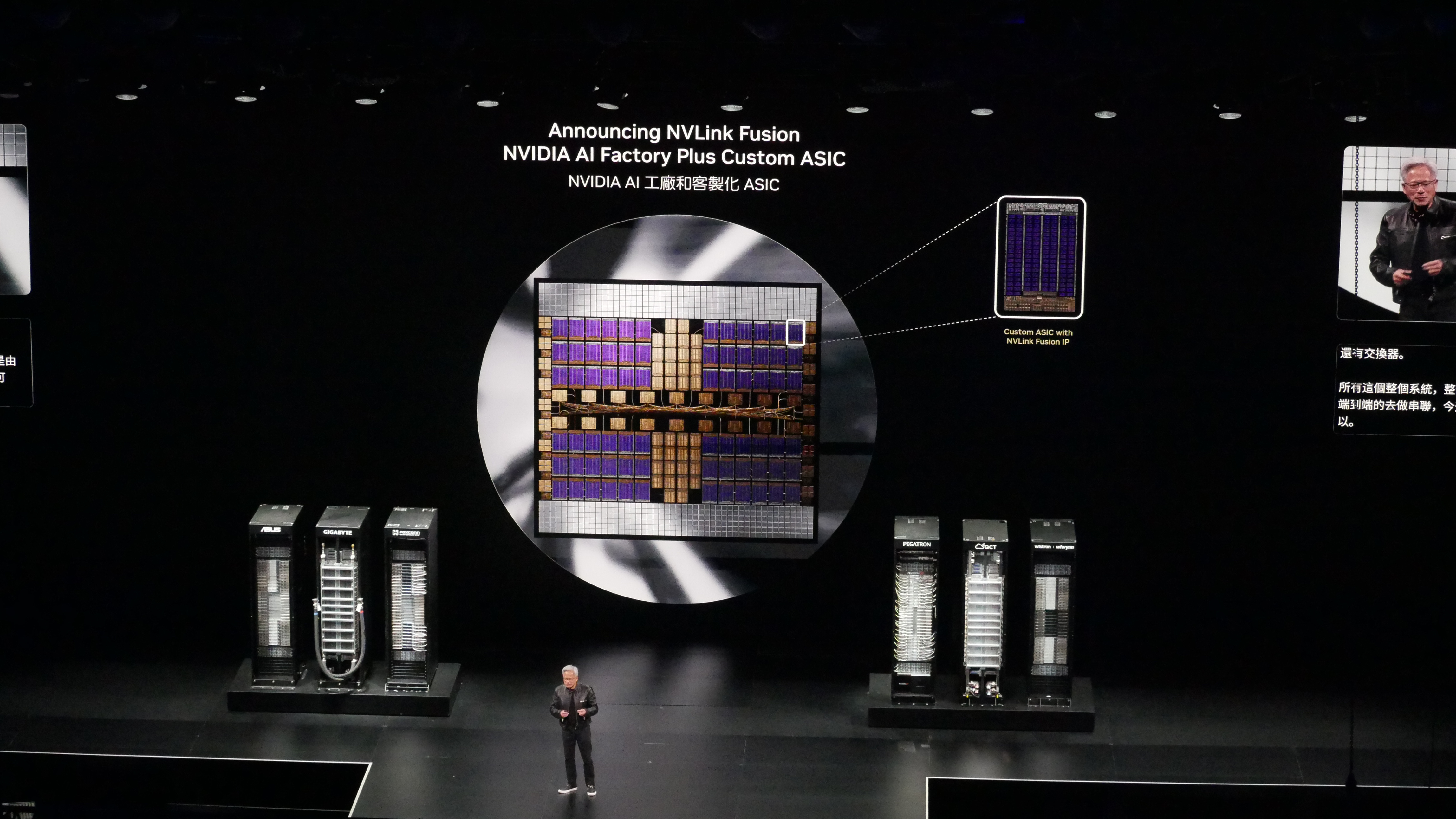

Overall, $34.1b of NVIDIA’s DC revenue came from compute products. The remaining $5.0b came from networking products, the first time that sub-segment has crossed the $5b mark, representing an incredibly rapid 64% QoQ revenue growth. According to NVIDIA, this was primarily driven by growth in demand for hardware for NVLink fabric networks – and which NVIDIA recently doubled-down on with NVLink Fusion – as well as increased sales of classical Ethernet product sales for AI customers and consumer internet companies alike. NVIDIA’s official commentary doesn’t allude much to NVL72, but it’s notable that the rack-scale system makes extensive use of NVLink to interconnect all 72 of its Blackwell GPUs. Which means that NVIDIA’s networking hardware sales are set to scale up significantly with NVL72 sales now that it’s in full production.

Meanwhile, NVIDIA’s data center segment faces the question of what to do with the remaining H20 accelerators that were originally bound for China. Although initial speculation was that NVIDIA would simply cut back their performance further to meet the new US export restrictions, in this afternoon’s earnings call, Jensen Huang ruled that out. Citing that H20 was already cut down by as much as possible while remaining a viable product, Huang has indicated that Huang won’t be retooling their remaining H20 inventory for China.

"The new limits pretty much make it impossible to reduce Hopper any further for any productive use. The new limits, mean it's the end of the road for Hopper (for China). We have limited options."

Whether this means that NVIDIA can find other customers for the already significantly cut-down H20 remains to be seen. At best, NVIDIA would need to sell the accelerators for a significantly lower price tag, never mind the fact that they’d be trying to sell Hopper hardware to markets that can freely buy the otherwise superior Blackwell hardware.

All told, prior to the H20 ban, NVIDIA had H20 orders going out to Q3 that have since been cancelled. Which is why NVIDIA’s Q1 H20 charge is so significant: the company is essentially eating the costs of nearly a year’s worth of accelerators they were intending to sell.

Gaming: GeForce

💵 Q1 Revenue $3.8b, up 42% YoY

Besides NVIDIA’s seemingly evergreen data center segment, another major growth segment for NVIDIA in Q1 was their gaming segment. Following a painful Q4’25 that saw gaming revenues decline on a quarterly and yearly basis, NVIDIA has turned things around on the back of the GeForce RTX 50 series (Blackwell) launch for consumers, posting significant quarterly and yearly revenue gains.

Altogether, NVIDIA booked $3.8b of revenue for its gaming segment in Q1’26, an all-time revenue record for the gaming segment. This was a 42% YoY revenue increase, and an even sharper 48% QoQ revenue increase. It also helped NVIDIA’s gaming segment claw back some of its total revenue share in the company – now up to 8.5% – pushing the data center segment back below 90%.

With Q4’25 being the calm before the storm of the launch of the bulk of the GeForce RTX 50 series, Q1 is when NVIDIA is finally beginning to reap most of that revenue. By the close of Q1, all but NVIDIA’s highest-volume xx60 series parts had launched, so Q1 reflects a full quarter of revenue for most – but not all – of NVIDIA’s GeForce RTX 50 series product lines. With NVIDIA now solidly shipping Blackwell hardware to consumers and add-in board partners alike, according to NVIDIA this has been their fastest consumer hardware ramp in the company’s history.

Looking forward, the final piece of the puzzle will be NVIDIA’s GeForce RTX 5060 cards, which launched last week, a few weeks into Q2. This is NVIDIA’s highest volume segment of consumer cards, but it’s also thought to be the thinnest in terms of margins. So its release bodes well for NVIDIA’s top-line gaming revenue, though it may not move the needle much on NVIDIA’s overall profitability (which is dwarfed by data center sales even at the best of times).

Professional Visualization

💵 Q1 Revenue $509m, up 19% YoY

As with NVIDIA’s gaming segment, their professional visualization segment is starting to benefit from the recent release of NVIDIA’s Blackwell architecture GPUs.

Coming off of its best quarter in almost 3 years, the ProViz segment booked $509m in revenue for Q1. This is a trivial drop from Q4’25, and a 19% year-over-year increase. A relatively stable market, ProViz is normally slow to move in one direction or another.

As with ProViz’s record performance in Q4’25, NVIDIA is attributing the strong performance of this segment more to AI than graphics, saying that the YoY increase was driven by “broader adoption of Ada RTX workstation GPUs, addressing workflows in AI acceleration, real-time graphics rendering and data simulation.” ProViz revenue should shift over to RTX Pro Broadwell cards now that those are shipping, though looking at historical trends, it will take a while for OEMs to swap over to the newer cards in their pre-built systems.

This segment will also be the beneficiary of NVIDIA’s DGX Spark (née, DIGITS) and DGX Station systems as those start shipping. Though with NVIDIA partnering with OEMs to help them develop their own versions of those systems, NVIDIA will not hold the entire pre-built Spark/Station market to itself. As mentioned at Computex and again on the financial call, Spark is expected to be available in Q3 this year, with Workstation coming to market later. Between GTC, Computex, and other conversations, we’ve heard reports that Spark has been delayed due to manufacturing defects that should now be solved, but it has meant a later-than planned launch.

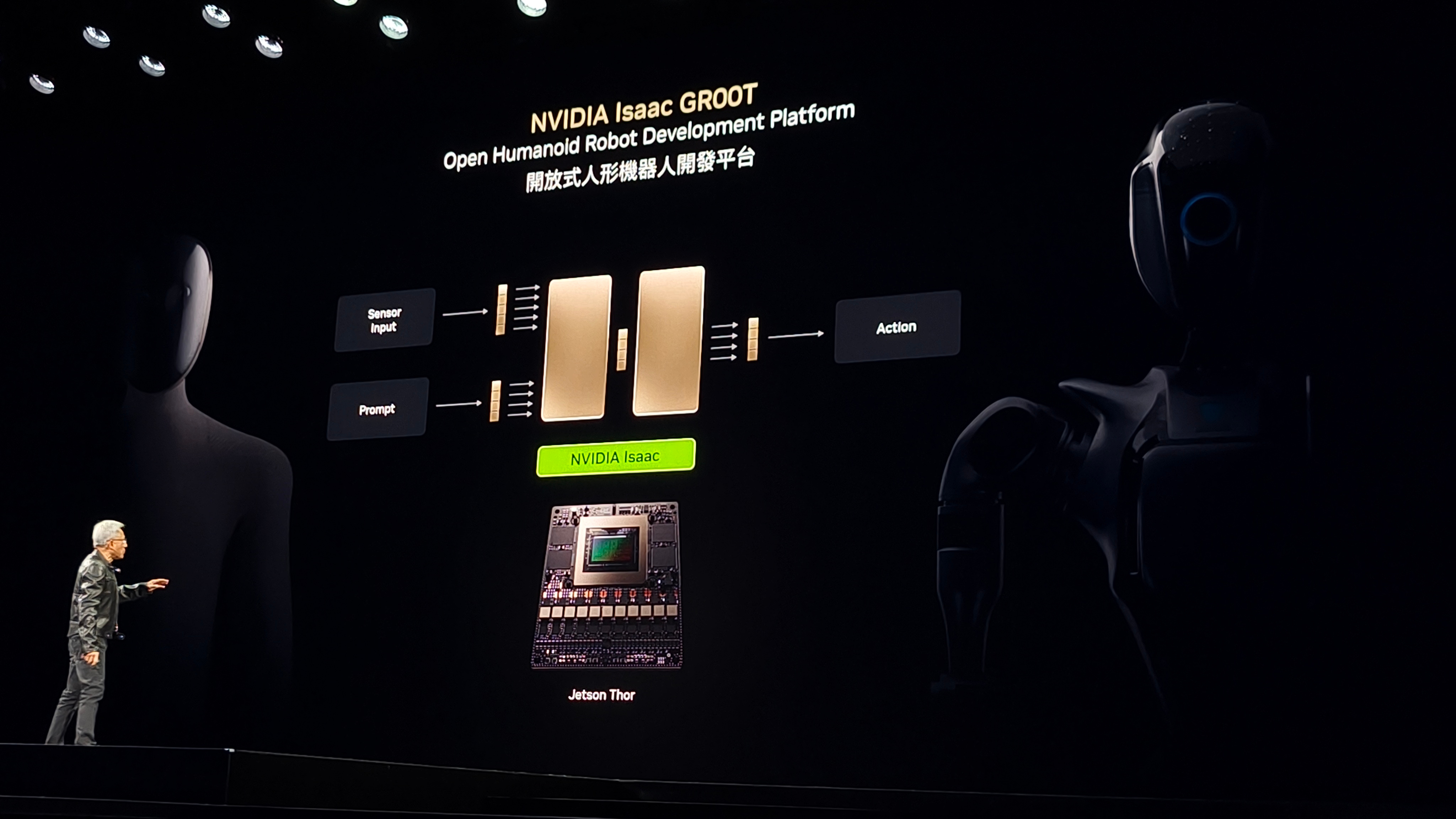

Automotive/Robotics: etson, DRIVE, Isaac

💵 Q1 Revenue $567m, up 72% YoY

Like its ProViz segment, NVIDIA’s third largest segment, automotive, embedded computing, and robotics is coming off of a very strong Q4 with only the slightest drop in revenue. For Q1’26, NVIDIA booked $567m in revenue, a marginal quarterly decrease and a 72% year-over-year increase. This puts the automotive segment’s revenue growth at just a percentage point behind NVIDIA’s data center business segment, underscoring how this remains another high-growth business for NVIDIA on a year-over-year basis.

While NVIDIA has not recently launched any new hardware products in this segment – everything continues to be driven by the Thor SoC and its predecessors – the company has enjoyed improving sales of its self-driving platforms, which it’s citing as the primary driver for this segment's revenue growth. A key highlight being a partnership with Mercedes for a full-stack solution that is now bearing fruit.

Nonetheless, NVIDIA has been making a hard push on the robotics front as well in its messaging, currently relying on the same hardware platforms. At this point, NVIDIA isn’t breaking out how much revenue they’re generating from robotics specifically, implying that sales are still relatively low while NVIDIA puts in the legwork to grow this business segment, however NVIDIA is expecting this segment to grow over the next decade quite significantly.

Ian: Last week I was at an industry event of one of NVIDIA’s key ecosystem partners, and they provided the following numbers.

$35 billion TAM in Robotics in 2030 (Statistica)

1 in 10 cars will be self driving in 2030 (Forbes)

1.3 billion robots by 2035 (citi)

4.0 billion robots by 2050 (citi), 650m of which will be humanoid robots

If we envision a ‘$10000’ price tag that Elon wants for humanoid robots, that would be a $6.5 trillion dollar market before we consider the infrastructure. Something to think about.

OEM & Other

💵 Q1 Revenue $111m, up 42% YoY

Rounding out NVIDIA’s reporting segments, we have the OEM & Other category. This catch-all unit has been used to account for things such as sales of GeForce MX GPUs (i.e. ultra low-end dGPUs for laptops) as well as NVIDIA’s revenue from Nintendo Switch 1 sales.

For the quarter, the OEM&O segment booked $111m in revenue, which was up 42% from the year-ago quarter. Unfortunately, NVIDIA is not providing any background information for this segment on this year’s reports, so there are no customers or product developments that the revenue growth can be concretely attributed to.

It's also unclear how NVIDIA is accounting for Nintendo Switch 2 SoC (T239) sales. In the company’s press release, they’ve specifically cited the Switch 2 as among their gaming developments; but given how OEM & Other is purposely a catch-all category, NVIDIA’s press release is not a reliable indicator of how they’re booking their Switch 2 revenue. NVIDIA did highlight on the call that over 150 million original Switch consoles have now been shipped.

Outlook, Q2 FY2026

Outlook is as follows:

💵 Q2’26 Revenue, $45.0b, +/- $900m

📈 Q2’26 Gross Margins of 72% +/- 0.5pp (non-GAAP)

For the second quarter of their 2026 fiscal year, NVIDIA is once again projecting a record quarter for revenue – albeit not by much. Assuming NVIDIA’s Q2 revenue goes as predicted, the company is expecting $45b +/- $900m in revenue, meaning that they will see some kind of revenue growth, but not the kind of double-digit growth that they’ve recorded over the past two years. This is mostly down to the $8b loss of H20 revenue already being factored into the upcoming quarter.

Meanwhile with the one-off H20 charge now behind them, NVIDIA expects gross margins to recover back to 72%, plus or minus half a point. As with their Q1 outlook, NVIDIA has reiterated that they’re targeting a non-GAAP gross margin in the mid-70s, which they expect to be able to reach later in the year as Blackwell finishes ramping.

Looking at NVIDIA’s top-line revenue outlook, the company’s conservative revenue growth prediction for Q2 is primarily rooted in the loss of H20 sales. While the H20 charge is one-off, according to NVIDIA the company was previously expecting to sell even more H20 accelerators in Q2 than Q1, with H20 sales once projected to reach $8b for the quarter, a 13% increase over what would have been Q1’s unrestricted sales. It should be noted that this is substantially higher than what most analysts were modelling, according to the Q&A. NVIDIA is seeing plenty of growth with its other products – and in other regions – more than offsetting the loss of business in China. But it’s essentially stunting their revenue growth for one more quarter. The good news? According to NVIDIA’s earnings call, the company is eating all the losses from H20 now as opposed to stringing it out over multiple quarters, so Q3 and beyond should not be impacted by the H20 export restrictions.

Otherwise, the major drivers for NVIDIA’s revenues in Q2 will continue to be all things Blackwell: more high margin Blackwell servers for the data center segment, more Blackwell-based GeForce cards for the consumer segment, and a ramp-up in sales of Blackwell-based ProViz cards. In other words: even with some headwinds from export restrictions, NVIDIA expects to keep firing on all cylinders going into the second quarter of their fiscal year.

Normally this is the point at which we’d post a full transcript of the analyst Q&A. NVIDIA requires permission in advance to be able to post it, so instead we’re just putting a summary of the main themes from the analysts here.

NVIDIA Analyst Q&A Summary

The post-earnings analyst session for NVIDIA's Q1 FY26 underscored five key themes: the emergence of reasoning-based AI as a compute supercycle, the strategic implications of China export controls, the framing of AI infrastructure as the next global buildout, the rising importance of networking, and a shifting geopolitical tone around U.S. tech diffusion.

1. Reasoning AI Is Redefining Inference Demand

Jensen framed the shift from prompt-based generation to reasoning-capable agents as a fundamental transformation in compute demand. These agents don’t just answer, he explained - they plan, access tools, analyze content, and generate vastly more internal tokens before producing output. The NVL72, built on GB200, is being positioned as the optimal platform for this new class of workloads, with Jensen emphasising his presentation at GTC where he showcased GB200 with 40x the throughput of Hopper. The company believes this will dramatically reduce latency and cost per result, even as workloads become more complex.

2. Export Controls Shut the Door on Hopper for China

With $2.5 billion in unshipped H20 revenue and a $4.5 billion charge tied to unsellable inventory, the China overhang is substantial. Huang made clear that the new export limits effectively terminate Hopper’s relevance in that region:

“The new limits pretty much make it impossible to reduce Hopper any further for any productive use. The new limits mean it’s the end of the road for Hopper [for China]. We have limited options.”

No alternative product is currently available or announced. While management is exploring options, the restrictions are too tight to repurpose Hopper-derived designs effectively. NVIDIA explained the long-term opportunity in China could be worth $50 billion - a TAM it now cannot serve under current policy. Jensen explained there is no ‘other’ chip in the pipe. If the US administration were to ease the rules, they will meet with them and organize appropriately.

3. AI Factories Become Global Infrastructure

Similar to his GTC and Computex keynotes, Jensen drew parallels between AI infrastructure and foundational utilities like electricity and the internet. With over 100 AI factories reportedly in the planning stages - and many more not yet publicly announced - NVIDIA sees every major economy and sector beginning to construct local intelligence-generation capacity. Cloud remains the starting point, but enterprise and sovereign demand are accelerating, especially in sectors where data sensitivity or latency prevents full migration to public cloud.

4. Networking Now a Competitive Edge

NVIDIA’s networking division reported sharp sequential growth, with Spectrum-X emerging as a key win. By porting InfiniBand-like latency and congestion controls into Ethernet, Spectrum-X boosts performance across large AI clusters by up to 95%. With NVLink and BlueField rounding out the stack, NVIDIA now offers multiple paths to optimize data movement, especially for shared and multi-tenant environments. A pair of new cloud providers adopted Spectrum-X this quarter, suggesting its positioning is resonating.

5. Policy Reversal Reinforces Global Diffusion Strategy

The reversal of U.S. AI diffusion rules - previously limiting full-stack exports - was characterized as both timely and strategically aligned. The company sees this as enabling the US AI ecosystem to spread internationally, just as demand from governments and industrial sectors is surging. Agentic AI is now considered “past the skepticism phase,” and Jensen believes that enterprise software stacks are finally ready to integrate reasoning-capable models - a shift that could redefine productivity across IT, telecom, and manufacturing.

More Than Moore, as with other research and analyst firms, provides or has provided paid research, analysis, advising, or consulting to many high-tech companies in the industry, which may include advertising on the More Than Moore newsletter or TechTechPotato YouTube channel and related social media. The companies that fall under this banner include AMD, Applied Materials, Armari, ASM, Ayar Labs, Baidu, Dialectica, Facebook, GLG, Guidepoint, IBM, Impala, Infineon, Intel, Kuehne+Nagel, Lattice Semi, Linode, MediaTek, NextSilicon, NordPass, NVIDIA, ProteanTecs, Qualcomm, SiFive, SIG, SiTime, Supermicro, Synopsys, Tenstorrent, Third Bridge, TSMC, Untether AI, Ventana Micro.

| A guest post by

|

2026?