NVIDIA 2025 Q4 Financials

It prints money!

Rounding out the 2024 earnings season well into Q1 of 2025, we have NVIDIA. The GPU company and its heavily offset fiscal year means that while most companies have been reporting on their 2024 earnings, what we’re technically looking at today from NVIDIA is their full fiscal year 2025 earnings, which covers the year up to January 26, 2025.

Nonetheless, one truth is always the same: NVIDIA is making money hand-over-fist. The second most valuable company in the world right now and the market leader on AI processors has been on a rapid growth spurt over the last couple of years that has since slowed a bit, but is still seeing the company’s revenue grow so much just in the past year! Suffice it to say, there is no other tech company quite like NVIDIA right now.

But with most of that growth coming from a single market segment – GPUs and associated hardware for AI training and inference – NVIDIA is reaping the benefits of what is fundamentally a very volatile market. The last quarter alone has seen the entire AI ecosystem shaken by the surprise release of DeepSeek’s latest model, which showcased the realization of a number of advances, some of which may propagate into the wider ecosystem to reduce the amount of computational time/cost needed to train and run a model. On the hardware side of matters, there are numerous companies gunning for a piece of what is primarily NVIDIA’s pie. Which is to say that while NVIDIA is flying high for now, continued success is not guaranteed – all of which makes NVIDIA’s latest efforts to diversify and grow in other markets an important element in ensuring their long-term success.

But for now, let’s talk about the results. Specifically, NVIDIA’s Q4’FY25 and full year FY2025 earnings. The company came into this quarter projecting $37.5B in revenue and a non-GAAP gross margin of 73.5% - and in increasingly traditional NVIDIA fashion, they’ve blown past their revenue projections once again while nailing the gross margin, thanks in large part to the exceptionally fast ramp of NVIDIA’s Blackwell architecture.

Key Takeaways (GAAP)

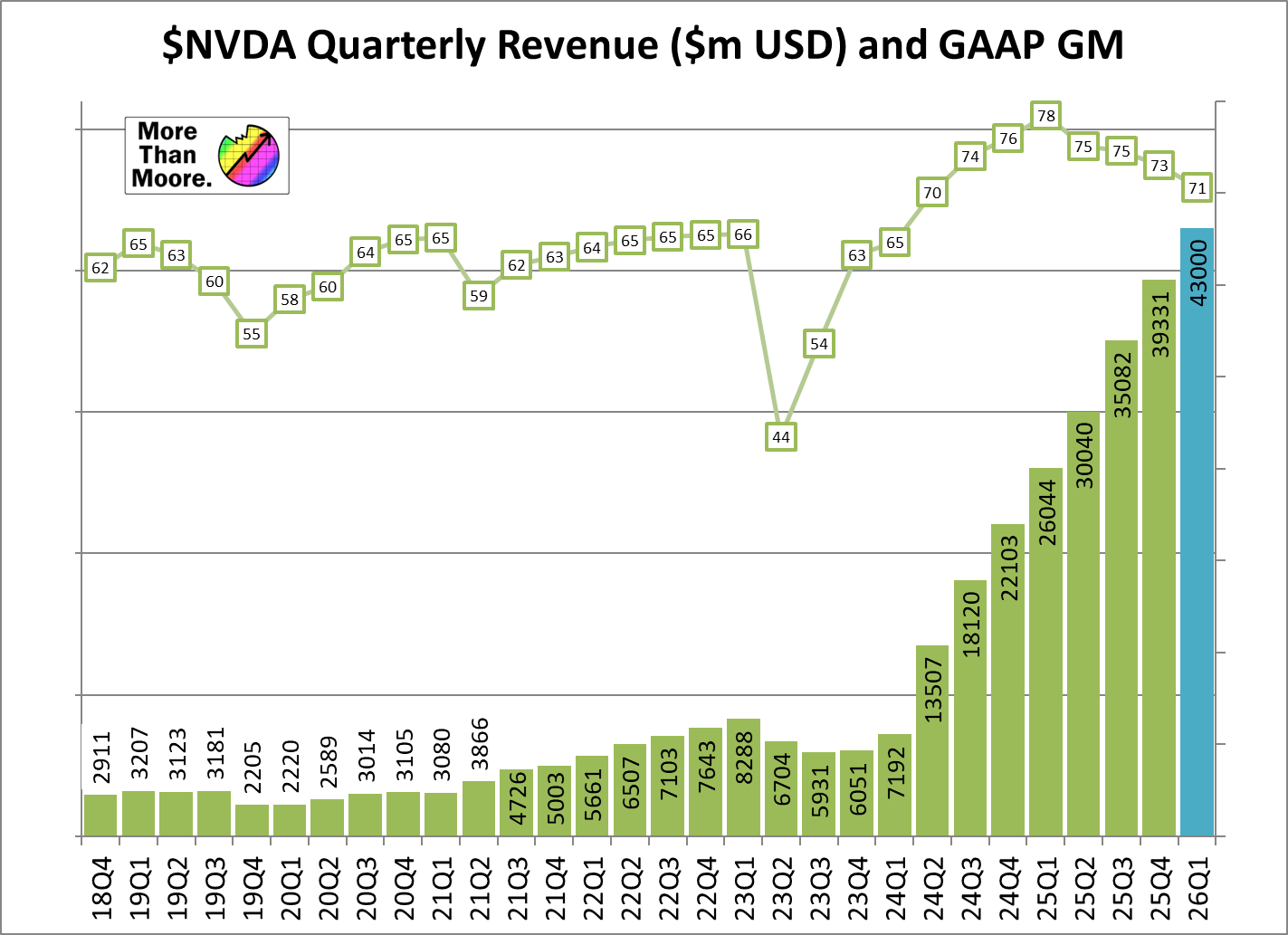

💵 Q4 Revenue, $39.3b, up 78% YoY from $22.1b and up 12% QoQ

📈 Q4 Gross Margin at 73%, down 3pp YoY and down 1.6pp QoQ

💰 Q4 Net Income of $22.1b, up 80% YoY from $12.3b and up 14% QoQ

🪙 Q4 EPS $0.89, up 82% YoY, up 14% QoQ

💵 FY Revenue, $130.5b, up 114% YoY from $60.9b

📈 FY Gross Margin at 75%, up 2.3pp YoY

💰 FY Net Income of $72.9, up 145% YoY from $29.8b

🪙 FY EPS $2.94, up 147% YoY

Highlights

💵 Record Quarterly Revenue

💵 Record Yearly Revenue

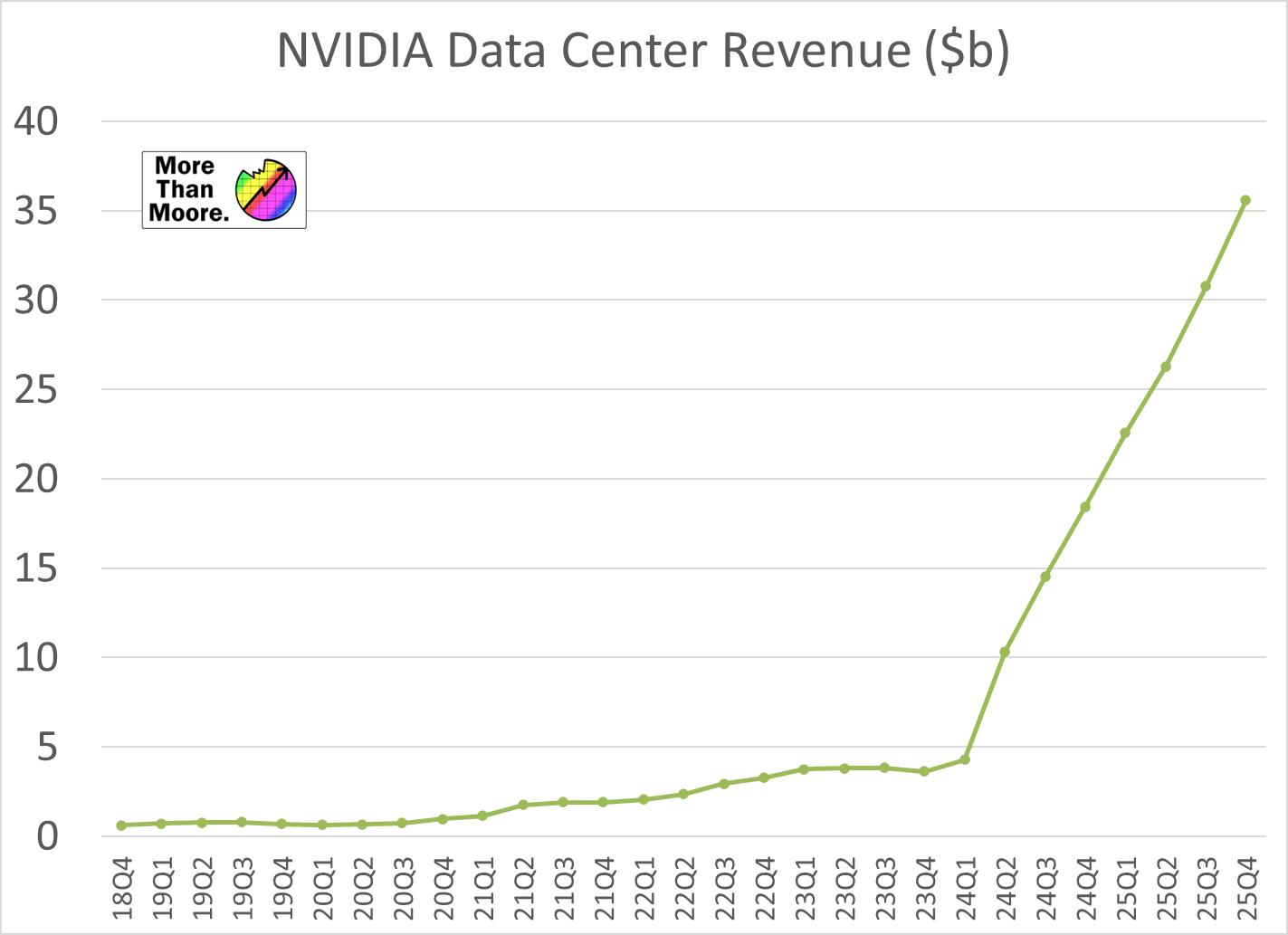

💵 Record Data Center Revenue

Outlook is as follows:

💵 Q1’26 Revenue, $43.0b, +/- $860m

📈 Q1’26 Gross Margins of 71% +/- 0.5pp (non-GAAP)

Financial Overview

Closing out NVIDIA’s offset fiscal year, the company booked $39.3b in revenue for Q4’25. Compared to Q4’24, that’s a massive 78% year-over-year increase in revenue. And if it were anyone besides NVIDIA, it would be stunning – but for NVIDIA, this has been par for the course over many of their preceding quarters. In fact, this is the 9th consecutive quarter of quarterly growth for the company. NVIDIA hasn’t seen a quarterly decline in revenue since Q3’23, bucking the trend of seasonality that impacts most other tech companies.

Going beyond NVIDIA’s top-line revenue, the rest of NVIDIA’s financials reflect this rapid growth as well. With a non-GAAP gross margin of 73.5%, NVIDIA still enjoys some of the highest gross margins in the industry for a hardware company. And the company’s net income is even outpacing their overall revenue growth, with net income for the quarter jumping 80% to $22.1b.

The worst thing you can say about an otherwise stellar quarter for NVIDIA is that their gross margins have begun to slip a bit. Whereas the company was at 76.7% margins for Q4’24, they’re seeing a 3.2 percentage point drop for Q4’25. This reflects the fact that while hardware sales are booming, NVIDIA is also producing Blackwell: it’s a more complex and more expensive hardware, particularly in the data center market. And those costs, it seems, are growing just a bit more than what NVIDIA can sell their hardware for. Though even that drop is apparently temporary; according to NVIDIA, as efficiency of scale kicks in, the company expects their gross margins to make it back to the mid-70s.

Overall, NVIDIA’s Q4’25 performance was a mix of meeting and beating the company’s guidance from the start of the quarter. NVIDIA was initially projecting $37.5b +/- 750m in revenue, with Q4 coming in at $1.8b ahead of that midpoint projection. Meanwhile, gross margins were dead on: NVIDIA hit 37.5% for their non-GAAP margin, exactly in the midpoint of their 73.5% +/- 0.5pp projection.

As for NVIDIA’s full year FY2025 results, virtually everything that can be said about Q4’25 applies to the full year as well. The company’s $130.5b in revenue for the year is another new record, blowing well, well past FY2024’s $60.9b – for an overall improvement of 114% year-over-year. $102b of that revenue comes directly from compute in its datacenter business. Net income grew even more, with NVIDIA ending the year with $74.3b (non-GAAP) in profits, 145% more than last year. And while NVIDIA’s gross margins have seemingly peaked on a quarterly basis, FY2025 will go down as NVIDIA’s best year ever, with a 75.5% non-GAAP gross margin for the year.

Finally, taking a quick look at NVIDIA’s business unit revenue and associated product mix, Q4 will be recorded as NVIDIA’s most lopsided year yet. Over 90% of NVIDIA’s revenue came from their Data Center segment in Q4’25, marking the first time Data Center revenue has ever crossed that threshold. We’ll get into the hows and whys in the coming sections, but in short it reflects the massive growth of the Data Center segment over the past several quarters, while NVIDIA’s other business units have seen far more modest growth – or even some sequential shrinking.

Data Center: Blackwell, Hopper, & Grace

💵 Q4 Revenue $35.6b, up 93% YoY

💵 FY Revenue $115.1b, up 142% YoY

For Q4’25, NVIDIA’s flagship market platform has once again delivered exceptional growth. Altogether, NVIDIA shipped $35.6b in DC products for the quarter, driving NVIDIA’s explosive growth and potent profitability. At over 90% of NVIDIA’s revenues, it is now safe to say that NVIDIA is primarily a data center company, with some side hobbies in gaming, automotive, and professional visualization.

Unfortunately, NVIDIA is pretty opaque about the underlying financials for their market platforms, and the company doesn’t disclose further details such as operating incomes or operating margins. The Data Center business is clearly stupidly profitable right now, but there isn’t the data available to say how that profitability compares to past quarters.

At any rate, Q4 saw the continued ramping of products based on NVIDIA’s Blackwell architecture, such as GB200, B100, and B200, allowing a larger number of customers to get their hands on the coveted accelerators. According to NVIDIA, the Blackwell ramp has been their fastest product ramp in the company’s history, with $11b of NVIDIA’s quarterly Data Center revenue being attributable to Blackwell products. And just to put that number in context, NVIDIA’s entire Data Center business 2 years ago was generating just $3.6b in revenue, underscoring how much NVIDIA has grown in the past couple of years. Now $11b of revenue is still the minority of NVIDIA’s Data Center compute sales.

On the flip side of the coin, NVIDIA does break out networking sales (Infiniband and Ethernet) from Data Center compute sales, in this case highlighting that at $3b in networking revenue for the quarter, sales are actually down on a quarterly and yearly basis. According to NVIDIA, customers are increasingly transitioning from racks of NVLink 8 systems connected via InfiniBand to larger NVLink 72 systems, which forgo the expensive InfiniBand for external NVLink and Ethernet connections. We believe NVLink is counted under compute, not networking.

This ultimately doesn’t do NVIDIA’s networking division any favors in terms of revenue, but it’s to be expected with NVIDIA’s heavier usage of Ethernet with Blackwell products. Still, NVIDIA is also saying that they expect their networking segment to return to growth later this year – so the current trend is being treated as a blip.

Those developments aside, NVIDIA’s messaging around the Data Center market right now is that things are progressing on schedule, with Blackwell continuing to ramp while NVIDIA’s overall Data Center revenue continues to soar. There are no product roadmap changes being announced today – especially not with GTC taking place in under a month – so what you see is what you get with regards to NVIDIA’s financials.

Gaming: GeForce

💵 Q4 Revenue $2.5b, down 11% YoY

💵 FY Revenue $11.4b, up 9% YoY

NVIDIA’s second biggest market platform, Gaming, is arguably the most interesting platform this time around, though not for good reasons. Of NVIDIA’s 5 major platforms, Gaming is the only platform to see a year-over-year (and QoQ) revenue decline. All told, Gaming revenue was $2.5b, which was down 11% from the $2.9b NVIDIA booked in Q4’24.

In their CFO commentary, NVIDIA was quick to address this drop by attributing it to a limited GPU supply. NVIDIA’s quarter ended 4 days before the retail launch of the Blackwell-based GeForce 50 series – and thus Q4 was in the middle of their transition from shipping Ada products to shipping Blackwell products. With NVIDIA ramping down production of Ada GPUs a bit earlier in the year to drain the market ahead of the GeForce 50 launch, the net result was that NVIDIA ended up shipping fewer GPUs overall. The company is careful to avoid calling it a shortage – so it’s not clear how many more Ada GPUs they could have even sold with Blackwell right around the corner – but one way or another, Q4 has become the lull between GeForce generations for NVIDIA.

That lull in sales also means there’s been very little new going on for this segment, despite the $2.5b in revenue. NVIDIA still holds the lion’s share of the PC graphics market, even if it is a smaller market ahead of the launch of the latest generation of video cards.

Professional Visualization

💵 Q4 Revenue $511m, up 10% YoY

💵 FY Revenue $1.9b, up 21% YoY

But even with Gaming being down, there were some bright points in the graphics market. Gaming’s counterpart, Professional Visualization (ProViz) booked its best quarter in almost 3 years, with $511m in revenue for Q4’25.

A relatively stable market, ProViz is normally slow to move in one direction or another. Most notably, the demand for ProViz products spiked immediately after the end of the COVID pandemic, when NVIDIA booked a record $643m in revenue. Q4’25, in turn, marks the first time in almost 3 years that quarterly revenues have surpassed $500m, following a string of $300-$400m quarters.

And despite the focus on graphics, according to NVIDIA it’s been AI that’s been driving the growth of this segment. Specifically, the company is citing “the continued ramp of Ada RTX GPU workstations for use cases such as generative AI-powered design, simulation, and engineering.”

Like gaming, ProViz should be positively impacted by the ramp of Blackwell GPUs throughout the year. As well, this will be the product segment that NVIDIA uses to book revenue from their DIGITS workstation, which has been attracting significant attention ahead of its launch.

Automotive/Embedded: Jetson, DRIVE

💵 Q4 Revenue $570m, up 103% YoY

💵 FY Revenue $1.7b, up 55% YoY

Another one of NVIDIA’s smaller divisions, their Automotive division was another winner for Q4’25 and FY2025, showcasing growth over the quarter and for the full year. For Q4, NVIDIA booked $570m in revenue, which at 103% in revenue growth, is actually NVIDIA’s fastest growing segment on a percentage basis. And while quarterly numbers aren’t nearly as strong, Auto revenue was still up 5% QoQ.

In fact, while NVIDIA’s press release doesn’t explicitly note this to be a record quarter for the Auto division, we cannot find a higher grossing quarter going back to 2019. So like the Data Center market, this would appear to be a record quarter for Automotive as well.

The big winner here appears to be NVIDIA’s DRIVE self-driving platforms, with the company attributing the majority of that revenue growth to increased sales there. The recent quarter did have a few other notable items for NVIDIA in this segment, particularly the launch of the Jetson Orin Nano single board computer, which is a cut-down SBC based on NVIDIA’s most recent Orin SoC.

OEM & Other

💵 Q4 Revenue $126m, up 40% YoY

💵 FY Revenue $389m, up 27% YoY

NVIDIA’s final market segment – and their smallest – is the OEM & Other unit. This catch-all unit has been used to account for things such as sales of GeForce MX GPUs (i.e. ultra low-end dGPUs for laptops) as well as NVIDIA’s revenue from Nintendo Switch sales.

For the quarter, the OEM&O segment booked $126m in revenue, which was up 40% from the year-ago quarter. Unfortunately, NVIDIA is not providing any background information for this segment on this year’s reports, so there are no customers or product developments that the revenue growth can be concretely attributed to.

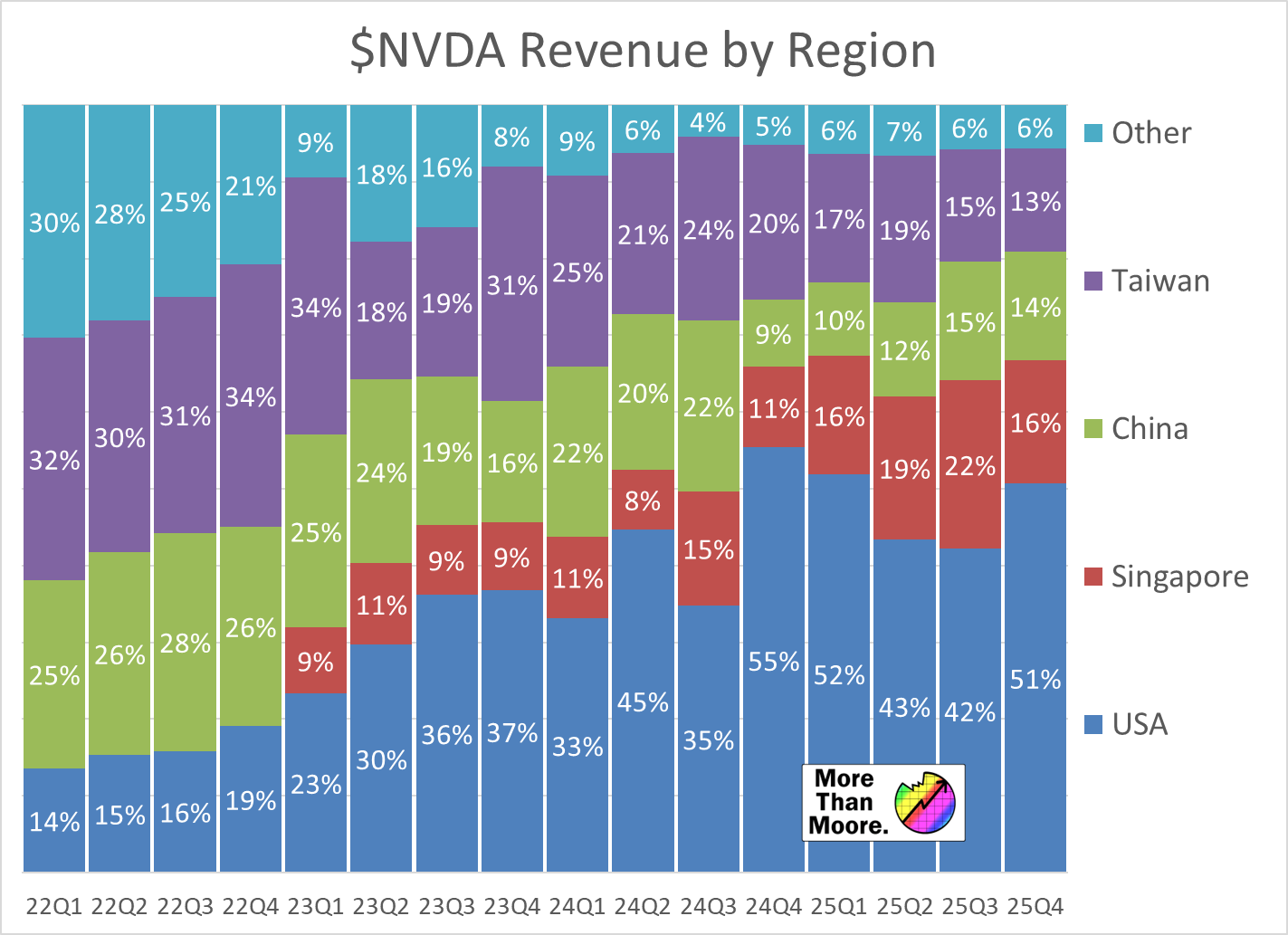

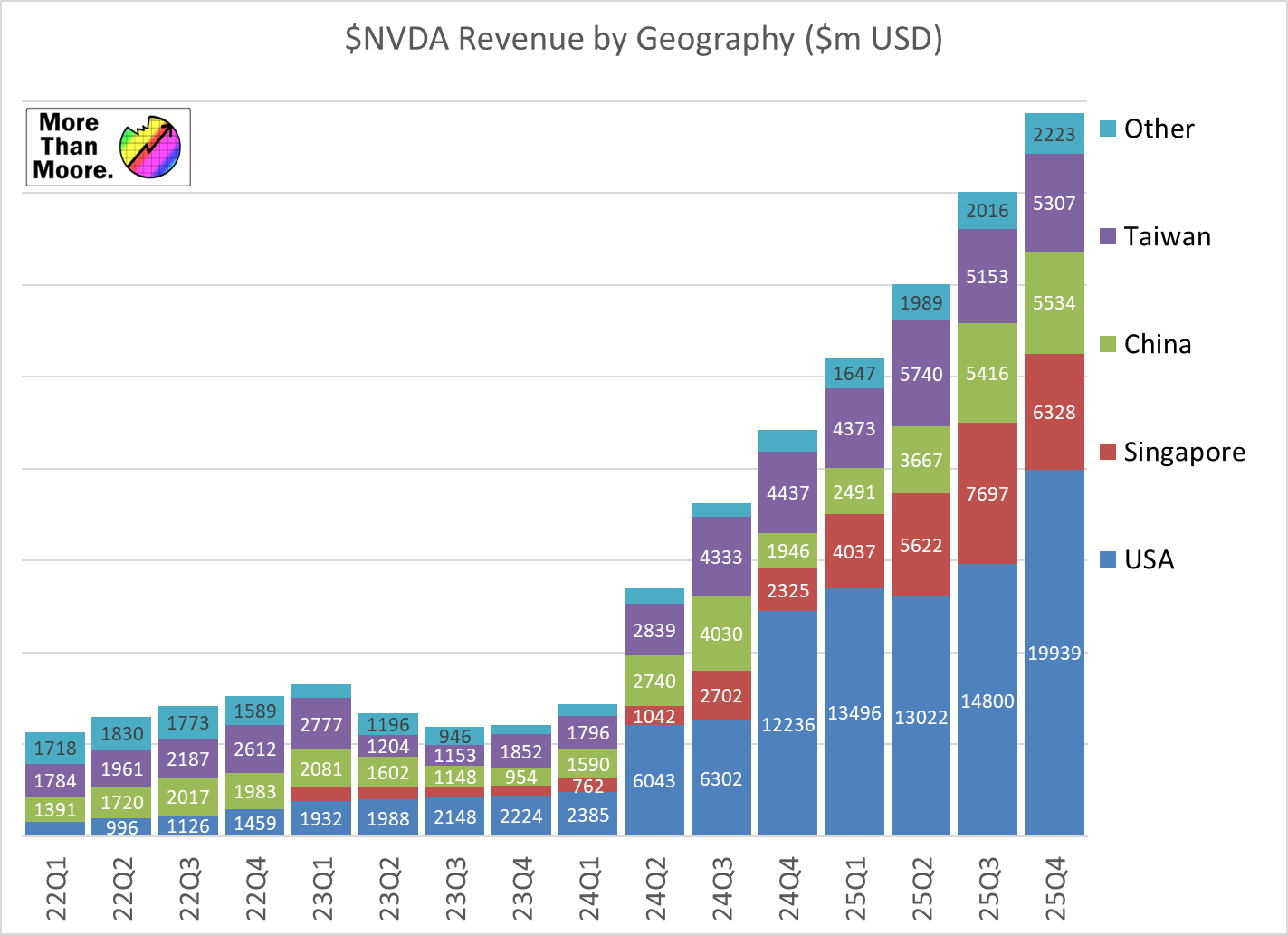

Regional Breakdown

We also have a quick look at NVIDIA’s regional revenue breakdown, which the company publishes as part of its more detailed SE filings.

NVIDIA has been under some heat in recent months, as it has become better known how much of their revenue has come from the small island city-state of Singapore. In short, while hardware shipments to Singapore amounted to less than 2% of NVIDIA’s revenue for FY2025, sales/billings to Singapore accounted for 18% of NVIDIA’s revenue. In other words, most of the hardware being billed to customers in Singapore isn’t actually being shipped to Singapore. According to NVIDIA, “Customers use Singapore to centralize invoicing while our products are almost always shipped elsewhere,” though it’s not clear where that hardware is being shipped – and critically for the US-based NVIDIA, how much of it is going to China.

Back at home, the US continues to be NVIDIA’s single largest region by revenue, with that lead growing in the fourth quarter and the US once again contributing to the majority of NVIDIA’s revenues. According to NVIDIA, that growth has been driven by the Blackwell launch.

Employee Counts

NVIDIA reports its employee counts once per year, in its full FY listings. At the end of FY2025, the company is reporting 36,000 employees, to the nearest hundred. This is quite a jump from last year, when the company only reported 29,600. This +6400 jump equates to around 20%, and we understand that most of these hires are in software development.

Given NVIDIA’s situation, it makes sense that the company is expanding fast as it enables customers to deploy its hardware. It will be interesting to see if this trend continues in line with sales going forward.

Outlook, Q1 FY2026

Outlook is as follows:

💵 Q1’26 Revenue, $43.0b, +/- $860m

📈 Q1’26 Gross Margins of 71% +/- 0.5pp (non-GAAP)

For the first quarter of their 2026 fiscal year, NVIDIA is once again projecting a record quarter for revenue – what would be their 10th consecutive quarter of growth. Gross margins will once again decline though, this time to 71%, as a further consequence of the Blackwell ramp. As noted earlier, NVIDIA does expect gross margins to recover later in the year, at which point they should get back to the mid-70s.

The primary driver for NVIDIA’s revenues in Q1 will continue to be the Data Center segment, as Blackwell production continues to ramp and NVIDIA is able to ship more of the high price tag AI processors. As well, this will be the first quarter in which NVIDIA’s Blackwell-based GeForce video cards will be on store shelves, which should provide a bump in gaming revenue. At least, barring any more unexpected roadblocks with that launch.

NVIDIA does have a key upcoming event, GTC, from March 17-21st 2025 in the San Jose Convention Center, San Francisco. CEO Jen-Hsun Huang will take the stage at the SAP center for the keynote on March 18th. Last year the company announced Blackwell, and while we’re not expecting a similarly shattering announcement this year due to timing (aka we know what Blackwell Ultra is), on the financial call JHH stated that they’ll be talking about Blackwell, Vera Rubin (next gen), and beyond. Other analysts are expecting a B300 announcement as well.

If you happen to be at the event or in the bay area that week, Ian will see you there!

More Than Moore, as with other research and analyst firms, provides or has provided paid research, analysis, advising, or consulting to many high-tech companies in the industry, which may include advertising on the More Than Moore newsletter or TechTechPotato YouTube channel and related social media. The companies that fall under this banner include AMD, Applied Materials, Armari, ASM, Ayar Labs, Baidu, Dialectica, Facebook, GLG, Guidepoint, IBM, Impala, Infineon, Intel, Kuehne+Nagel, Lattice Semi, Linode, MediaTek, NextSilicon, NordPass, NVIDIA, ProteanTecs, Qualcomm, SiFive, SIG, SiTime, Supermicro, Synopsys, Tenstorrent, Third Bridge, TSMC, Untether AI, Ventana Micro.

(Ian additional: here’s where we would have put a transcript of the analyst Q&A for subscribers, however it was mentioned at the beginning of the call we need written permission to do so. I’ll get that in advance for next quarter.)

| A guest post by

|