Intel 2024 Q4 Financials

Outlook is Looking Better after Q3

While 2024 has been a wild year for most tech companies in one way or another, there is arguably no company with a wilder year than Intel. The company posted disastrous results for Q3’24 that saw Intel lose some $16.6b on the books as the company undertook a serious restructuring and staff layoff process in order to fix some long-term structural problems at the company that increasingly left it uncompetitive. And before all was said and done for 2024, the company’s turnaround CEO, Pat Gelsinger, quit the company, leaving the company’s transition in the hands of newly minted interim co-CEOs Michelle Johnston Holthaus and David Zinsner. Two new members also joined the board only a few days later.

But with all of that upheaval has come a chance for Intel to reset the playing field, and to try to find its footing in a world where the company has found itself losing relevance. How that will play out in the coming months and years remains to be seen. But for now, the company is doing what it can to claw back revenue, market share, and profitability, all the while preparing for the incredibly important release of the Intel 18A fab process, Intel’s first-generation GAAFET-based process that former CEO Pat Gelsinger all but bet the company on.

In the interim, there have been a couple much-needed wins for Intel. The company finally secured its US CHIPS Act funding, with the US Department of Commerce awarding Intel $7.86b to help fund new fab construction. Some of that money has already been received. And on the earnings side of matters, Intel is turning the page on 2024 by beating their Q4 outlook, showcasing some important short-term improvements.

Key Takeaways (GAAP)

💵 Q4 Revenue, $14.3b, down 7% YoY from $15.4b and up 7% QoQ

💵 FY Revenue, $53.1b, down 2% YoY from $54.2b

📈 Q4 Gross Margin at 39.2%, down 6.5pp YoY and up 24.2pp QoQ

📈 FY Gross Margin at 32.7%, down 7.3pp YoY

💰 Q4 Net Income of -$126m, down 105% YoY from $2.7b and up 99% QoQ

💰 FY Net Income of -$18.8b, down 1100% YoY from $1.7B

🪙 Q4 EPS -$0.03, down 105% YoY, up 99% QoQ

🪙 FY EPS $4.38, down 1100% YoY

Highlights

Before we go into the details, it’s worth highlighting some news from the financial results and the prepared remarks.

Intel has confirmed that the successor to Panther Lake (the consumer CPU set for 2025H2) is called Nova Lake and is due to market in 2026.

Intel has officially set the launch date for Clearwater Forest, its 18A-based E-core product for the datacenter, to the first half of 2026. Intel originally announced that the ramp for this product would happen in 2025H2, however it was unclear when the general availability was going to be. Intel now confirms this.

The next-generation AI product after Gaudi 3, called Falcon Shores, is becoming a de-risk design but won’t be coming to market in order to assist and accelerate Jaguar Shores, the updated model. Reasons for this boil down to a fast changing AI market and customer build outs becoming more rack-scale, which Jaguar is more suited for.

Financial Overview

For the final quarter of Intel’s tumultuous 2024, the company booked $14.3b in revenue. As previously projected by the company, this is a decline of several percent for what was overall a stronger Q4’23, with gross margins dropping to a problematic (and unprofitable) 39.2%. Consequently, Intel was once again operating in the red this year, with a net loss of $126m.

But on a GAAP basis, at least, the weak quarter was a major improvement for Intel, with revenue, gross margins, and net income all well above Intel’s restructuring-heavy Q3. And even the non-GAAP numbers are a similar story, with Intel swinging into profitability on a non-GAAP basis while pushing gross margins above 42%. On the whole, Intel exited Q3 while undertaking some very hard changes to improve the trajectory of the company over the longer term, and with that behind them, they can begin the hard process of climbing back out of the red.

And amidst all of these trials and tribulations, Intel has been able to take a small win by coming in ahead of their previous projections for the quarter. At the end of Q3, Intel was forecasting $13.3b to $14.3b in revenue, and a gross margin of 36.5%. Ultimately Intel has come in at the high-end of that revenue estimate by booking $14.3b in revenue. And more importantly, they came in well ahead of their gross margin estimate, with a final gross margin of 39.2%, putting the company much closer to (but just shy of) profitability than Intel was previously expecting.

Otherwise, for the full year, Intel’s FY2024 financials are largely dominated by their Q3 restructuring changes. With $53.1b in revenue, Intel recorded a slight, 2% dip compared to FY2023’s $54.2b. However, the company’s profitability was all but obliterated thanks to those restructuring changes, closing the year with a gross margin of just 32.7%, and a staggering net income loss of $18.8b.

Now let’s go through each of the different business unit results. It’s worth noting that Intel has done some changes to its reporting structure. Mobileye and Altera, the two business units that Intel has/is in the process of enabling partial IPOs for, used to be separate orders of business - but are now combined into the Other unit. Edge computing is moving from NEX to CCG, and as a result Intel’s numbers have all been updated accordingly. But it does make this graph look a bit wonky.

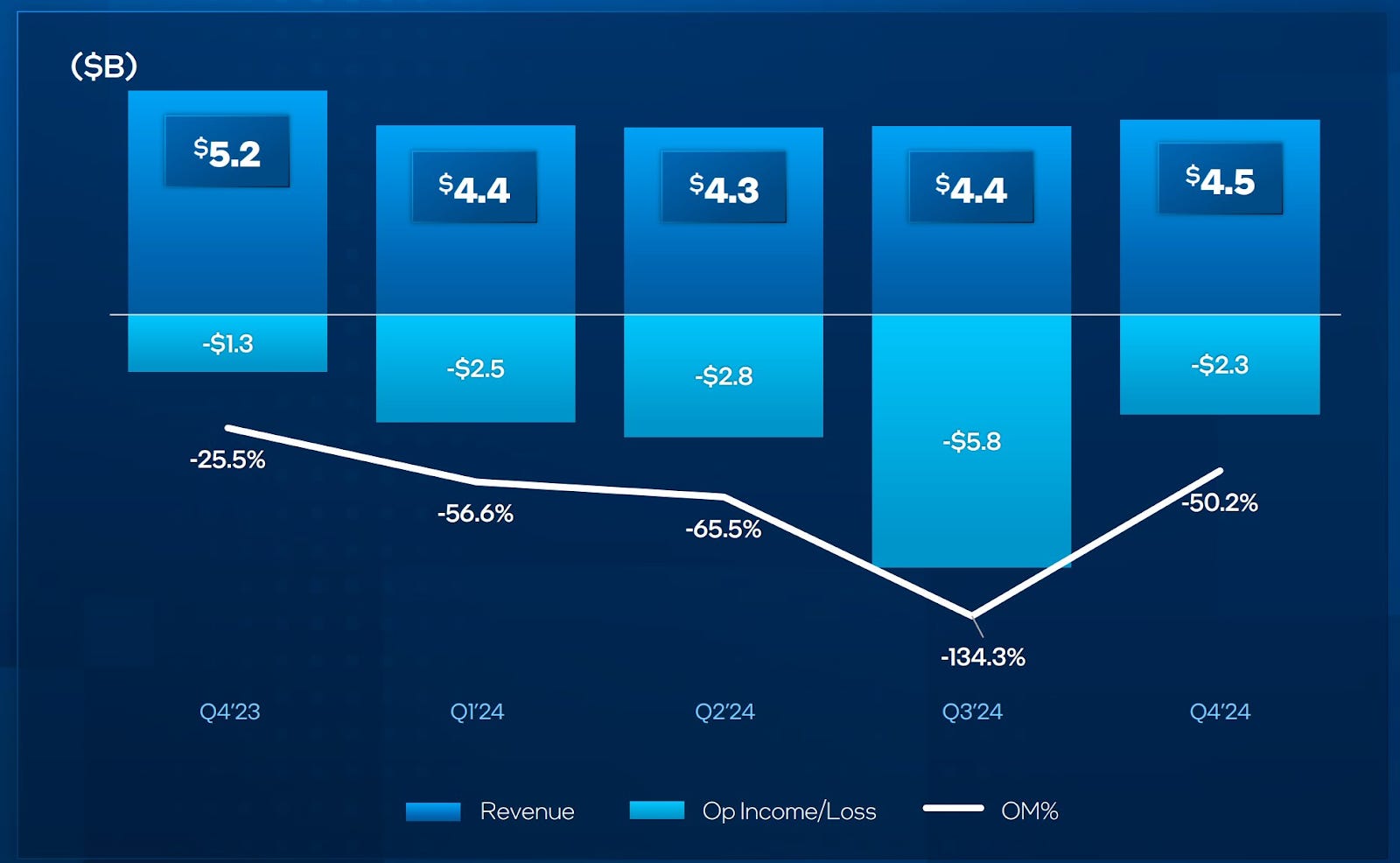

Intel Foundry

💵 Q4 Revenue $4.5b, down 13% YoY

💵 FY Revenue $17.5b, down 7% YoY

💰 Q4 Operating Loss $2.3b, down from $1.3b loss YoY

💰 FY Operating Loss $13.4b, down from $7.0b loss YoY

📈 Q4 Operating Margin -50%, down from -25% YoY

📈 FY Operating Margin -77%, down from -37% YoY

The most beleaguered segment of Intel has and continues to be the manufacturing side of the business, which is in the midst of its own turnaround as Intel pushes to become a major contract foundry. Along with preparing a manufacturing unit that previously wasn’t accustomed to working with outside customers – and is still in the process of learning how to best develop PDKs for external customers – Intel’s foundry unit is also preparing for the release of their radical 18A process node. All of which means that Foundry is spending a lot more right now than it is making – a fact laid bare now that Intel is operating on an internal foundry operating model where those costs are attributed to the foundry rather than the product groups.

With an operating loss of $2.3b for the quarter, Intel’s foundry unit is still looking at an operating margin of over negative 50%, so there is still a good distance to go to close that gap – and one that cannot be closed without landing some major external customers. As things stand, Intel’s leadership is focusing on getting Intel Foundry to break even by the end of 2027, 3 years (12 quarters) from now.

Complicating matters, Intel’s product groups have opted to use rival TSMC’s 3nm process nodes for both of Intel’s current-gen (200 series) Core processors, Lunar Lake and Arrow Lake, so Intel’s fabs are not enjoying as much business from themselves as they’d normally see. Co-CEO Michelle Johnston Holthaus says that for every generation of product, they need the right product on the right node for the right time - and so Foundry has to win the Products business. That’s going to be true for Panther Lake, as 70% of that silicon will be in house - as part of the Q&A Holthaus stated that Nova Lake, the generation beyond, will also be a mix of foundry offerings. Nonetheless, back to the numbers here, Q4 foundry revenue was down 13% year over year, and Lunar/Arrow are still ramping.

Financials aside, Intel is full-steam ahead with preparing for the 18A rollout. While today’s financial release doesn’t provide new figures on where yields are – just comments on the “progress that Intel Foundry is making on performance and yields” – the company is noting that they’re installing new equipment to further the ramp-up for high volume production, with Intel Fab 52 (Arizona) installing additional process tools to expand 18A manufacturing. Overall, Intel is expecting to kick off volume production on Intel 18A in the second half of this year, which will support the launch of Panther Lake for clients and Clearwater Forest for servers.

(Side note here from Ian - I’ve spoken with Intel about their yield numbers. Unfortunately I can’t share exact values and refer you to Intel’s publicly available comments, but I can confirm the yield curves are following standard industry trends as we get closer to high-volume manufacturing.)

The bigger news for the Foundry group however is that they are finally getting their US CHIPS Act funding, being awarded $7.86b back in the middle of the quarter. Those funds are being paid out on a milestone basis; Intel has received the first $1.1b in Q4, and according to the company, they’ve received another $1.1b this month (which will show up in their Q1’25 financials). Compared to Intel Foundry’s financial losses, this isn’t enough to completely close the gap, but it helps to fund Intel’s major infrastructure investments while improving what would have otherwise been an even rougher quarter for the foundry. CFO David Zinsner has said that some of that first batch of money has already applied to offset the costs involved in the hardware.

Data Center and AI (DCAI)

💵 Q4 Revenue $3.4b, down 3% YoY from $3.3b

💵 FY Revenue $12.8b, up 1% YoY from $12.6b

💰 Q4 Operating Income $233m, down from $738m YoY

💰 FY Operating Income $1.3b, down from $1.6b YoY

📈 Q4 Operating Margin 6.9%, down from 21.1% YoY

📈 FY Operating Margin 10.4%, down from 12.8% YoY

At one point in its history, Intel’s focus was on becoming a “data-centric” company with a 50/50 split between data-center and consumer. But those dreams have gone by the wayside for now. While Intel’s Data Center and AI (DCAI) business unit is still operating in the black, its revenues and operating margins have taken a hit as Intel has lost business to both rival CPU firm AMD, as well as clients looking to invest in AI hardware (e.g. GPUs) that they can’t get from Intel.

With an operating margin of 6.9% for Q4, this is the weakest performance from the DCAI unit since Intel broke out its reporting in its current fashion. Some of this follows from business changes – having spun-off FPGA specialist Altera, Intel no longer has that revenue contributing to DCAI – but it also follows ongoing market share losses to AMD and its EPYC lineup of processors. Still, in terms of total hardware volume, $12.8b in sales for the year is no small feat; it’s just that Intel isn’t making much in the way of profits from it.

Consequently, while DCAI is decidedly the smaller of Intel’s two major chip groups in revenue at this time, it’s getting an outsized share of focus from the company’s leadership, as Intel still strives to bring back the kind of revenues and margins the business unit was once known for. In the short term, the goal is to stanch the market share losses to AMD by ensuring that Intel’s Xeon offerings are more competitive. Granite Rapids, released at the tail-end of Q3, is the start of that for Intel - and it was reported recently that those parts already on the market are set for a price-cut to remain competitive (cutting prices is something Intel rarely does publicly, even though most big customers aren’t paying list price anyway). Clearwater Forest, Intel’s first 18A server part, will be a bigger piece of that puzzle. Though that will not launch until the first half of 2026.

As for Intel’s DCAI GPU efforts, bigger changes are afoot. As part of today’s earnings release, Intel is announcing that their upcoming Falcon Shores GPU will no longer be coming to market.

To be sure, the chip is not cancelled. But Intel has opted not to sell the chip – or rather, not to take the final steps necessary to make it a retail product – based on what the company is calling “industry feedback.” Instead, Falcon Shores will be an internal test chip, the learnings from which Intel will be using to bring its successor, Jaguar Shores, to market.

Reading between the lines, I’m left with the impression that Intel doesn’t expect Falcon Shores to be a competitive product by the time it would be ready for a commercial release. Falcon Shores has had already a difficult upbringing – because Falcon Shores was an amalgamation of IP, the fact that one part of its predecessor, Rialto Bridge, was cancelled wasn’t a good thing. Falcon itself was at one point intended to be an XPU, combining CPU and GPU and AI, before pivoting to being a GPU – so this is merely the latest knock for Intel’s datacenter GPU efforts. Still, following the Rialto Bridge cancellation, it’s an especially bad look for the market for Intel to effectively cancel another datacenter GPU - even if they say their customers would prefer waiting for Jaguar Shores.

We have a full video on this announcement, which you can find here.

Nonetheless, Falcon Shores development is being finished and used internally. This means it will end up serving as a prototype of sorts for Jaguar Shores, which is now slated to be Intel’s next commercial datacenter GPU. Though for the time being, Intel isn’t providing any guidance on when Jaguar Shores may be available. Customers that are looking to develop on Jaguar are advised to start using Gaudi 3 as their base platform, and Intel will be enabling the up-convert when Jaguar hits the market.

Client Computing Group (CCG)

💵 Q4 Revenue $8.0b, down 9% YoY from $8.8b

💵 FY Revenue $30.3b, up 4% YoY from $29.3b

💰 Q4 Operating Income $3.1b, down from $3.6b YoY

💰 FY Operating Income $10.9b, up from $9.5b YoY

📈 Q4 Operating Margin 38.1%, down from 40.3% YoY

📈 FY Operating Margin 36.1%, up from 32.5% YoY

With Intel’s DCAI business unit taking a hit in recent quarters, it’s the Client Computing Group (CCG) that is once again largely carrying Intel on its back. With higher revenues – and more importantly still, a much higher operating margin – CCG in 2024 has done what it’s always done, which is to trudge on and continue making money for Intel.

The later half of 2024 was marked by the launch of both Intel’s ultra-mobile focused Lunar Lake CPU, as well as their broader market Arrow Lake CPU. Both rely on Intel’s in-house tiled (chiplet) construction, but both rely on Intel fab rival TSMC for producing their critical compute tiles.

Intel has made it clear from the start that being so reliant on TSMC would impact their operating margins, and unsurprisingly, we see just this in Q4, where the margin slips from 40.3% to 38.1% year-over-year. Nonetheless, that’s still a respectable margin for the group, albeit keeping in mind that Arrow Lake in particular is still ramping, and its laptop SKUs weren’t even launched until a few weeks ago during Q1’25.

On a yearly basis, revenue for the quarter was down versus Q4’23. Intel doesn’t make any specific citations for this, but take your pick between product buying cycles, competition from AMD, and that for Q4’24 Intel needed to ramp a new chip with complex packaging requirements.

And with that ramp underway, for the purposes of Intel’s financial results release, the company has already turned its collective eye to what’s next. Panther Lake will be Intel’s 2025 client product release when it launches in the second half of the year. Serving as Intel’s lead product for their 18A process, Panther Lake represents a critical milestone for the company. Not only will it prove (or disprove) the performance of Intel’s 18A process, but it will be the point where Intel brings the manufacturing of compute tiles back in-house to their own fabs. So the ramifications aren’t just for the production side of matters, but for the finance side of matters as well.

Following Panther Lake, Intel has confirmed that 2026 will see the launch of Nova Lake. Details on this chip are few and far between, but as Intel is aiming for a yearly chip cadence for the next couple of years, it’s a chip that’s already less than two years away.

Speaking of years, while Q4’24 was down on a year-over-year basis for CCG, 2024 as a whole was a win for the group. Revenue, operating income, and operating margins all meaningfully improved over FY2023, with Intel booking over $30b in client revenue and holding a 36% operating margin.

Finally, for FY2025, Intel is projecting that the company will ship a cumulative total of over 100 million NPU-equipped (AI PC) CPUs. Being cumulative, this count does include the past year of Meteor Lake shipments, but with Lunar Lake and Arrow Lake forming a much larger product stack with the Core Ultra 200 series, the bulk of those 100 million chips will be in 2025 sales.

Network and Edge (NEX)

💵 Q4 Revenue $1.6b, up 10% YoY from $1.5b

💵 FY Revenue $5.8b, up 1% YoY from $5.8b

💰 Q4 Operating Income $340m, up from $109m YoY

💰 FY Operating Income $931m, up from $204m YoY

📈 Q4 Operating Margin 20.9%, down from 7.4% YoY

📈 FY Operating Margin 15.9%, up from 3.5% YoY

The runt of the litter for Intel’s current business unit organization, the Network and Edge (NEX) group hasn’t been receiving nearly as much attention as Intel’s other business units. Nonetheless, the spunky group is looking far better than it was a year ago.

For the quarter, NEX booked $1.6b in revenue, which is up 10% on a year-over-year basis. More significant is that its operating margins have improved significantly, jumping from 7.4% in Q4’23 to 20.9% in Q4’24. For Intel’s financial needs this still isn’t quite good enough, but it’s a marked improvement in profitability at a time when most of Intel’s other business units are holding steady or are on the decline.

This is reflected in the FY2024 results as well. While revenue is just above flat at $5.8b, the operating margin for the year was 20.9%, netting Intel $931m in operating income.

Changes are in store for NEX, though. Intel has previously announced that they are moving part of their edge sales into CCG. And curiously, Intel’s presentation slide deck for this quarter says “Edge moving to CCG; Networking to DCAI” with no further information provided in any other Intel documents. If Intel is moving the entirety of its networking operations under the DCAI umbrella, then this would be a major shift for the company, as it would essentially reduce the product side of the company to just two groups: CCG and DCAI. We’ve reached out to Intel for clarification on the matter.

As for product news for NEX, Intel has relatively little to discuss at the moment. The company launched some new Cora Ultra SKUs for edge customers back at CES. But that’s as much as they had to say about the business unit for their Q4 earnings release and prepared remarks.

All Other (Altera, Mobileye, etc)

💵 Q4 Revenue $1042m, down 20% YoY from $1297m

💵 FY Revenue $3.8b, down 32% YoY from $5.6b

💰 Q4 Operating Income $118m, down from $142m YoY

💰 FY Operating Income -$84m, down from $1079m YoY

📈 Q4 Operating Margin 11.3%, down from 10.9% YoY

📈 FY Operating Margin -2.2%, down from 19.2% YoY

Last and least, we have Intel’s “All Other” group, which is not a product group in and of itself, but the amalgamation for Intel’s non-reportable segments. This includes Altera, Mobileye – both of which have been spun-off – start-ups, and divested businesses.

Given that the cash flow from these items is otherwise external business units, Intel’s color commentary here is minimal. Altera continues to weigh down Intel’s financials as customers continue chipping away at the group’s oversized inventory - a problem across almost all FPGA and embedded businesses right now. On the other hand, Mobileye’s profitability has improved over the year, due to better leverage of its portfolio.

All told, all Others accounted for $1042m in revenue for the quarter, which was down 20% from the year-ago quarter. But it was in the black on an operating basis, with an 11.3% operating margin. The full-year results get significantly pulled down by losses in Q1 and Q2 as part of the macro environment, however, adding up to an operating loss for the year of $84m, a sharp dive from the $1b operating income in FY2023.

According to Intel, there will be more color on the finer points of the Altera side of the deal in Q1. We look forward to understanding what those are.

Outlook, Q1 2025

Outlook is as follows:

💵 Q1’25 Revenue, $12.2b, +/- $500m

📈 Q1’25 Gross Margins of 33.8% (GAAP) and 36.0% (non-GAAP)

Looking forward to the rest of Q1’25, Intel is taking a fairly conservative stance, even coming off of the stronger-than-expected Q4.

With Q1 normally being the weakest quarter for the company due to seasonality, Intel is projecting even lower - between $11.7b and $12.7b in revenue, with a GAAP gross margin of 33.8%. Both would be significant quarter-over-quarter declines for the company – and problematic for getting to profitability. There are a few reasons for this.

Intel is now solidly in the middle of their product cycles for all of their major product lines – Lunar Lake, Arrow Lake, and Granite Rapids are all shipping and continuing to ramp up in volume through the first half of this year. So while Intel will ship more of these chips, and their chip mixes will shift accordingly, there is nothing new coming to the table in Q1 to shake things up in what’s normally their weakest quarter anyhow.

For now, Intel is plowing ahead with their product lines and development plans; the big changes will come in the second half of the year as the Intel 18A process node ramps for high volume manufacturing. Even then, Intel Foundry is on a multi-year journey that likely won’t see it reaching break-even status until the end of 2027, but the 18A launch will be the next milestone to see whether Intel can pull that off.

Intel’s Q1 is also down due to a mix of macroeconomic conditions - the potential threat of tariffs does affect Intel in some product categories (it’s not just some of the latest chips at TSMC as Intel has always had ‘some’ business at other foundries), but it has led to some Asian customers accelerating their purchases and increasing inventories just in case. CFO David Zinsner stated that this has pulled some traditional Q1 revenue back into Q4.

As for the long-term aspects of the product side of Intel’s business, the most stunning revelation to come out of today’s earnings release is without a double the quasi-cancellation of Falcon Shores. While Intel provides the majority of CPUs used in AI systems, the AI boom has largely passed the company by due to a lack of datacenter-class GPUs suitable for inference. While the company has just launched Gaudi 3, the response has been lukewarm for a number of reasons – and this has earned the ire of investors and the board of directors for a while now. Canceling the commercial release of Falcon Shores, in turn, means that Intel is now one more generation out from being able to meaningfully participate in (and profit from) the AI training market – for whatever form that is by the time Jaguar Shores ships.

Otherwise, the next major move from Intel will likely be its leadership. While Intel appointed David Zinsner and Michelle Johnston Holthaus as co-CEOs upon Pat Gelsinger’s resignation, the company has made it clear that this is an interim solution, and that they are looking for another CEO as a permanent replacement. This leaves Zinsner and Holthaus as caretakers, in some respects, and while the two of them are implementing some immediate changes at Intel – presumably, changes the board wanted but Gelsinger did not – any bigger changes will come with a new CEO. Which means whether you’re inside or outside of Intel, you’re in a holding pattern to see what direction the next CEO will take the company. Intel confirmed that while the search continues, there isn’t any additional news on this front at this time.

There was also a minor tidbit at the end. The question as to whether Intel Foundry would be spun off (or made into a major owned subsidiary like Mobileye or Altera) has one that investors have been asking since Intel’s fortunes took a turn for the worse and the IDM 2.0 model came around coalescing Foundry into its own business unit. Intel has been fence sitting on this for quite some time, stating that it’s important for Foundry to be accountable for its actions and to treat Intel Products like any other customer - however it’s still a close relationship being under the same parent company.

As part of the call, Zinsner confirmed that Intel Foundry will establish an independent subsidiary structure to provide clear guidance and operational separation. This structure, according to Zinsner, will enable Intel, the parent company, to seek additional funding options from both strategic and financial partners, and that process has already started.

The following is the Financial Analyst Q&A held after the prepared remarks, and is provided for paid subscribers. This transcription is provided as-is, and may contain transcription errors.

More Than Moore, as with other research and analyst firms, provides or has provided paid research, analysis, advising, or consulting to many high-tech companies in the industry, which may include advertising on the More Than Moore newsletter or TechTechPotato YouTube channel and related social media. The companies that fall under this banner include AMD, Applied Materials, Armari, ASM, Ayar Labs, Baidu, Dialectica, Facebook, GLG, Guidepoint, IBM, Impala, Infineon, Intel, Kuehne+Nagel, Lattice Semi, Linode, MediaTek, NextSilicon, NordPass, NVIDIA, ProteanTecs, Qualcomm, SiFive, SIG, SiTime, Supermicro, Synopsys, Tenstorrent, Third Bridge, TSMC, Untether AI, Ventana Micro.

| A guest post by

|