$INTC Doubling Down, Again

Can It Work? 1Q 2023 Financial Breakdown

Intel INTC 0.00%↑ showcased its latest financial quarter with a string of interesting numbers. A good number of investors and analysts are picking over them, not only because of how Intel is changing its internal structures in light of investment, but also with respect to the macroeconomic conditions. To bring everyone up to speed on what these are:

Client PC unit sales are at a nadir – from 350m estimated units in 2022 at the start of that year, down to 200m equivalent by Q4. The outlook for 2023, depending on who you talk to, is 240m-270m. That’s quite a swing from the 350m high. It also depends if you count sell-in compared to sell-through, and is a big reason for undershipping.

Datacenter sales are similarly affected, however for different reasons. Economic contraction has businesses pulling back from investments and updates, along with system deployment delays, but the promise/threat of artificial intelligence and machine learning has them wanting to invest. China is still a sore topic, although Intel’s CEO makes comments about this which we’ll cover.

Q1 (and Q2) is typically considered an annual weak point in both client and datacenter globally, compared with the race to spend budgets in Q4/new Q4 products and as companies ramp through the year. This muddies some of the softness in macro, how much is seasonal vs market shifts.

Also, for Intel, there are reporting changes.

AXG Split For Reporting, Two New Names in CGFX and AXG (?!)

For this quarter, Intel has officially dissolved the reporting of the Accelerated Compute Group (AXG), which is where the recent push in graphics has been tracked, and no longer report a direct P&L.

Instead, the group still exists as two internal teams. Now it’s important to understand what’s going on here because Intel is going to confuse a lot of people. Instead of AXG, we now have:

CGFX: Client Graphics, which manages the consumer graphics hardware and software for desktop and mobile. This is headed up by Lisa Pearce, and is a segment reported as part of CCG.

AXG: Accelerated Compute, which manages the enterprise grade accelerators as well as all the architecture and engineering segments to do with graphics and compute. This is a segment under DCAI, and only covers three segments: Flex GPU (for video), Max GPU (Ponte Vecchio, Falcon Shores), and Max CPU (Sapphire Rapids with HBM). Essentially think of this as only for accelerators, not graphics, even though they’re called GPUs - because they’re not actually for playing games. The fact that Max CPU is in there is because it’s a HPC play. This division is run by Deepak Patil, although the Flex GPU/Max GPU is headed by AXG DC Compute lead Jeff McVeigh.

The fact that new AXG has the same name as old AXG but doesn’t include the ‘gaming graphics’ part of the business is going to confuse a lot of people for a long, long time.

This change is margin decretive to both CCG and DCAI. For context, in Q4 ’22, AXG had $247m in revenue and $441m in losses – at the time Intel said it was due to higher supercomputing revenue offset by integrated client graphics decline, which we assumed to mean attachment rates of mobile Intel GPUs into systems.

Intel has provided a ‘recast’ document for FY21, FY22, and each quarter of 2022 showing the revenue equivalents without AXG on their investor relations website.

‘Other’ Category Gets Two New Divisions

Due to Intel exiting specific markets, both Silicon Photonics and Automotive Foundry are reported under ‘Other’, rather than NEX and IFS respectively. This is somewhat confusing of a change for both.

In terms of Silicon Photonics, we have to differentiate here that there are two angles to it. There’s the connectivity site of photonics, the transceivers going from switch to switch inside a network, or Integrated Photonics, where you have a chiplet attached to a big chip that can enable photonics without any non-Photonics traces.

The connectivity part of Silicon Photonics is still going strong, but Intel last quarter scrapped its network switching division, which derived from its Barefoot acquisition several years prior. The networking division had a very strong roadmap with its Tofino switching silicon, and it was due to be a big recipient of Intel’s integrated photonics research for putting optical networking into big chips. Intel is still going forward with its integrated photonics research, although it looks like a future Xeon or GPU will be the first chip enabled.

As far as I understood, the connectivity element was reported under NEX, and the integrated research was under Intel Labs, as part of R&D. The fact that Intel showed off detach/re-attach photonics at Intel’s Innovation event last year shows that they’re still committed to SiPh as part of the future of the company. Now it seems it might all be reported under ‘Other’.

On Automotive Foundry, I would have assumed this would be filed under IFS, Intel Foundry Services. For whatever reason, this has been migrated to other – whereas if it is foundry related, it really should be under the foundry division. We’ll explore the segment a little bit later, as revenue at IFS dropped considerably, but herein lies an important crux of Intel’s future strategy. Right now, when Intel sells a chip, all the revenue goes into the product business unit, not to foundry – every fabless semi company by contrast can report the margin on their chip, and the foundry they work with can report margin on wafers – Intel has to bundle those two margins into one. Right now it can ‘afford’ to move some foundry financials around, but as IFS gets serious, it will have to decide what part of its margin goes where, and keep everything foundry related under IFS.

But for now, let’s look at the financial quarter.

Intel 1Q23 Financial Release YoY (vs 1Q22)

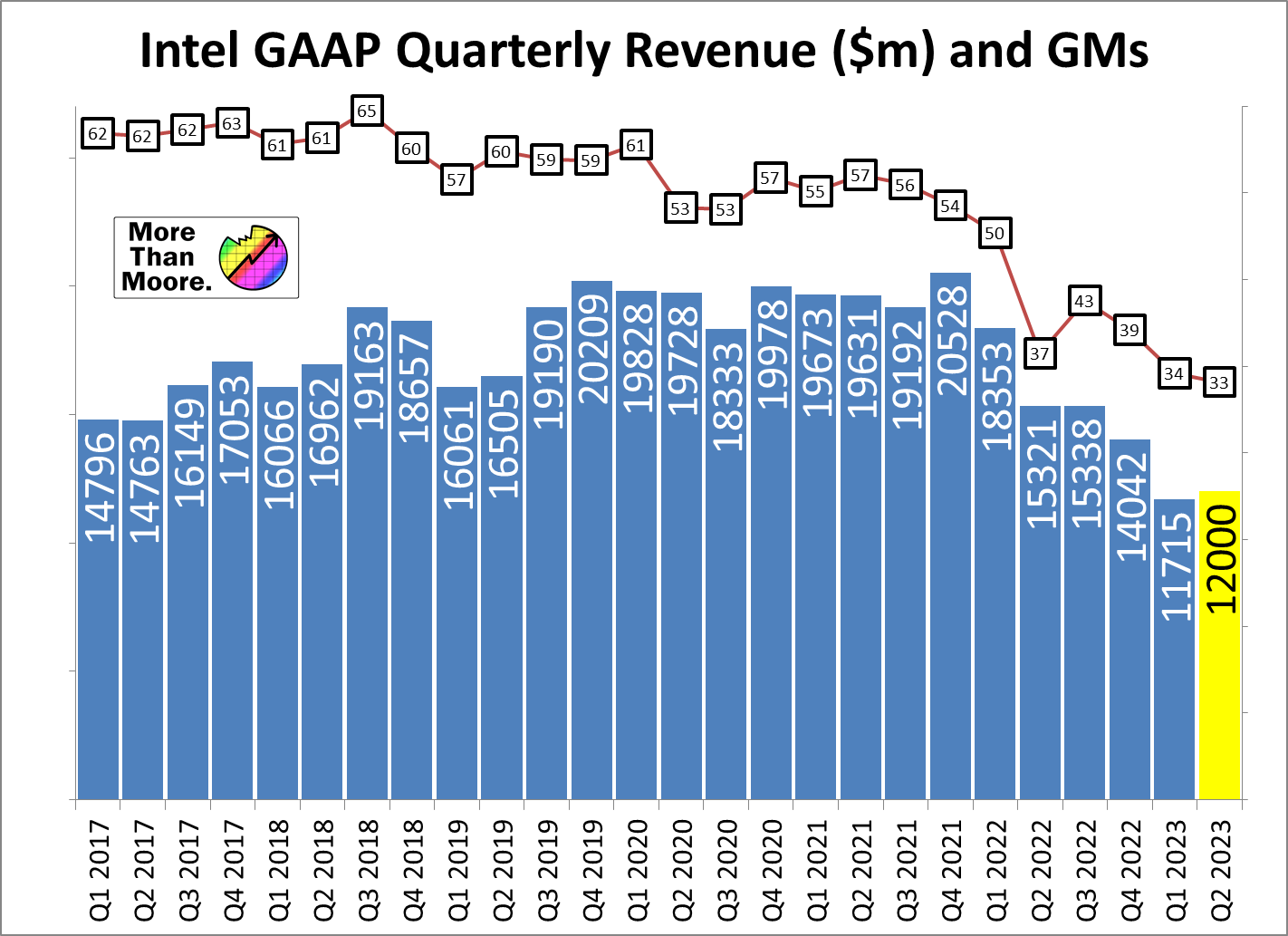

Revenue $11.715b, down 36% from $18.353b

Gross Margin GAAP 34.2%, down 1620bps from 50.4%

Non-GAAP 38.4%, down 1470bps from 35.1%

R&D and MG&A GAAP $5.4b, down 11% from $6.1b

Operating Margin GAAP -12.5%, down 3620bps from 23.7%

Net Income loss of $2.8 billion, down $10.9 billion

EPS -$0.66, down from +$1.98

Paid Dividends of $1.5b, zero change

These are all the headline numbers, with the big drop in quarterly revenue and margins. These are actually in-line with Intel’s guidance from last quarter: revenue at the mid-point and GMs at the low-end, but still within guidance and looking at the market, better than expected. Intel CEO Pat Gelsinger also stated that for the two key revenue generating segments, both outperformed expectations. We’ll get into those individually in a bit.

I will address the Gross Margins here though, given that Intel has a long historic view of high 50s/low 60s, even hitting as high as 65% in Q3 2018. Semiconductor manufacturing is a capital intensive business, and so if you are a foundry and you primarily (95%+) make your own product, having a severe drop in sales has a double effect on GMs as the factories end up underloaded. The nature of a weak market where customer inventory is high is that you undership to the market to help everyone adjust their stock levels, so in actual fact manufacturing ends up doubly impacted. When Gelsinger initially set out his IDM 2.0 strategy, there was the expectation that margins would drop down into the low 50s, maybe the mid-to-high 40s, but here we are in the 30s. The financial highlighted some of the reasons for this drop is due to specific headwinds that are suppressing the number. PG highlighted the following specifically for upcoming Q2, although I’m sure they apply well for Q1 also.

300 basis points due to factory underloading

250 basis points due to inventory reserves of upcoming MTL and EMR products

40 basis points due to increased sampling costs

So we’re talking a 5.1% margin loss due to these factors. We just covered factory underloading being a unique issue for Intel, which if demand returns then it will be a net positive. However the other two parts are worth probing.

The 250 basis points depression is for ‘pre-PRQ’ products, i.e. early inventory stock of upcoming launches. Typically a company like Intel will build silicon of its next generation product as it is fine tuning the final version of that silicon – when the only changes to be made are firmware and software. Building up silicon allows the company to meet launch day demand, but only if the version of the silicon is *truly* ready as they are made before those final changes. PG states that this 250bps loss may unwind and the products launch (MTL = Meteor Lake, EMR = Emerald Rapids), however given Intel’s product cycle being rapid over the next couple of years, it is uncertain if this loss will go away or come again another day (or, every other Q).

On the final point about sampling costs, Intel is putting more effort into supporting its partners, primarily with Emerald Rapids. In speaking with some big customers, there’s some wavering about Intel’s ability to deliver competitive products in the future given the delays of Sapphire Rapids and bring up over many cycles of silicon that platform produced. Intel is set to launch five DC Xeon products by the end of 2025, and although they are on two platforms, it’s a lot of work to partners and so I can only assume that this is extra resource/funding/support needed to help keep those platforms on track. Again, this might be another GM depression that’s going to be consistent over the next couple of years as confidence returns to Intel’s portfolio.

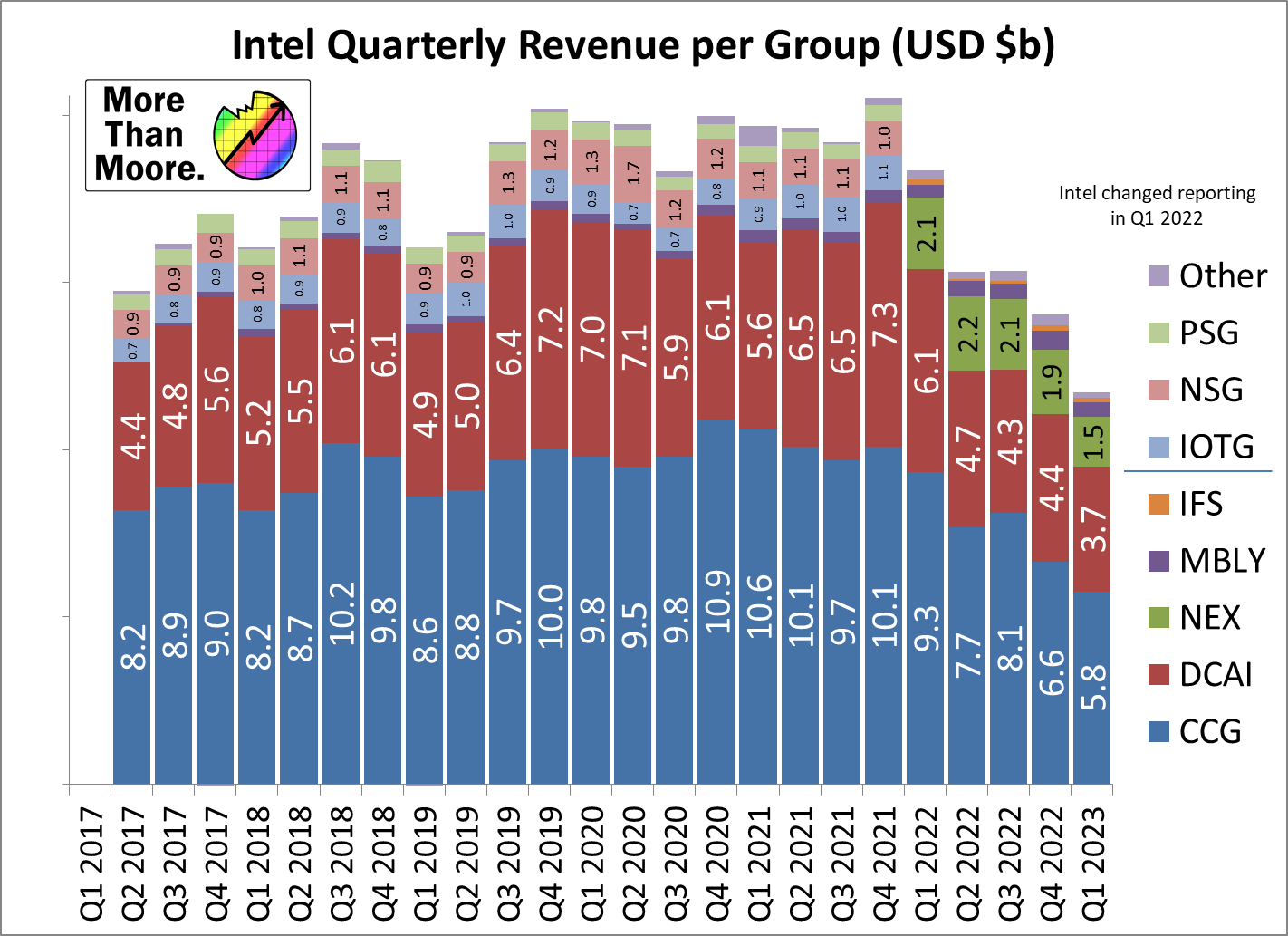

With that, let’s head into each business unit. Intel now lists five business units:

CCG, Client Computing Group (consumer desktop and laptop CPUs/GPUs)

DCAI, Datacenter and AI (Xeons, enterprise GPUs, FPGAs)

NEX, Network and Embedded/Edge

MBLY, Mobileye Automotive

IFS, Intel Foundry Services

Other

CCG, Client Computing Group (vs 1Q22)

Revenue $5.767 billion, down from $9.322 billion

Operating Income $0.5 billion, down from $2.7 billion

Operating Margin 9%, down from 29%

The big client adjustment we knew about going into this quarter is due to undershipping into the market. Distributors and partners went from having a good amount of stock that was suitable for high demand, to too much stock during a period of low demand, and as a result bought less from Intel than they were shipping to keep stock levels suitable. As a result, Intel sells into the market less than the sell through ratio. Intel believes that the sell-in rate for the year will be around 240m units, whereas sell-through will be at around 270m units, or 10m higher than AMD predicts.

With the market depressed, it also means a lower total addressable market regardless of market share, and Intel also stated in the call that end-users are pivoting to cheaper solutions as their wallets are also feeling the pinch. This means not only are unit sales down, the market is contracting, but average selling prices (ASPs) are decreasing as the mix of units being sold pivots to the cheaper end of the market. Intel breaks the segment down further into client type:

Desktop $1.879 billion, down from $2.641 billion, down 29%

Notebook $3.407 billion, down from $5.959 billion, down 57%

Other $0.481 billion, down from $0.722 billion, down 67%

Desktop faired the best, while notebook has a massive hit. Some might also point out that it was claimed Intel pre-loaded the client channel last quarter with older stock, and this is why it’s feeling the effects of lower ASPs today as partners are digesting that stock.

Intel is expecting a recovery in this market in the second half of the year but it’s clear that it still won’t be back up to Q1/Q2’22 levels any time soon. Intel states that with its visibility into its customer planning, they expect the market long term can support a 300m unit/year run rate, which it hopes to be sometime in 2023. Everyone in the industry is making similar noises more or less, but for Intel we’re going to see the first EUV products in Meteor Lake coming out by the end of the year. New technology, new process node, new packaging, new features, but will it be competitive in performance and power? We’re hoping to hear more about it in a few months, at a specific Meteor Lake architecture day I can assume, but there are still murmurings about cost given it is multiple chiplets, some from Intel and some from TSMC, along with expensive packaging, and what parts of the client market it will actually be applicable. Intel is trying a lot of things with Meteor Lake for the first time, and have a lot of balls to juggle.

DCAI, Datacenter and AI Group vs 1Q22

Revenue $3.718 billion, down from $6.074 billion

Operating Income loss $0.5 billion, down from +$1.4 billion

Operating Margin -14%, down from 23%

With revenue down 39%, Intel’s fixed costs showcase a full 137% drop in operating income which is now an overall loss for the company. Given Intel’s lead in enterprise processors only a few years ago, and with strong market share leadership in Intel’s historic strongholds, it seems extremely odd to say that the segment is losing money for the company. There are a number of reasons why.

Intel states that many of the factors that affected the client business also affected the DCAI business. Inventory digestion at partners leading to underselling, but also a market contraction in the amount of business available and on top of that, lower average selling prices. Intel actually specifies ‘competitive pressure’ in its slide deck affecting revenue, leading to lower sales. Intel’s in an odd situation with Sapphire Rapids – it’s expensive to make with 1600mm2+ of silicon on an expensive process node, and with customers looking at perf/watt as well as perf/$ and TCO metrics, I suspect there’s going to be a sizeable push to Emerald Rapids if it can supply better fundamentals over Sapphire Rapids.

(As an aside, I fully believe that EMR will be better for Intel to manufacture. We saw at the latest DCAI update that EMR is a two die solution rather than four in SPR. This means lower cost for packaging, fewer EMIB connections. It does mean bigger silicon dies though, which are more expensive to produce, but it’s expected that Intel will leverage core redundancy to ensure a high enough yield. EMR should be on Intel’s ‘last’ fully non-EUV process on Intel 7, so we should see some manufacturing kinks worked out, and potentially a more cost effective platform for manufacturing. Intel 7 isn’t going to IFS for external customers though like Intel 3, which I suspect showcases that the Intel 3 product lines are where it Intel can test its ability recoup its cost-effective manufacturing IDM strategy.)

For operating income, the loss comes from both the lower revenue, but Intel also states that it has higher unit costs now. I can only assume this is due to inflation in the supply chain rather than supply chain itself given how much has been invested into securing supply chain economics over the last few years. Intel also states it has excess capacity charges, perhaps due to the market contraction and partners having clauses as it pertains to sell-in and sell-through.

NEX, Network and Edge Group vs 1Q22

Revenue $1.489 billion, down from $2.139 billion

Operating Income loss of $300m, down from +$416 million

Operating Margin -20%, down from +19%

These comparisons exclude the NEX revenue from silicon photonics, but show a substantial ~$700m swing in operating income on the year for around a ~$700m loss in revenue. This time last year, we were talking about some of Intel’s latest networking developments, however this time around the company states the lower revenue is down to slow consumption at customers and inventories remaining high. With some markets, especially vRAN, Intel is claiming a near market complete capture, which shows that new markets need to be targeted for some products.

The fact that revenue and income dropped at around the same amount showcases that NEX needs a $1.8 billion revenue per quarter in order to have at least net zero income and not lose any money. Intel’s competitors have their own networking solutions – NVIDIA has Mellanox, AMD has Pensando, so we might be in a situation here where Intel needs to keep NEX for its overall offerings, but find markets to expand into with the same technology. The loss of the switch silicon reduced some of the losses, but it does raise questions if Intel will either cut other NEX sub-divisions, or roll it into something like DCAI in the future. Intel needs a networking solution for the market, so it can’t get rid of it entirely.

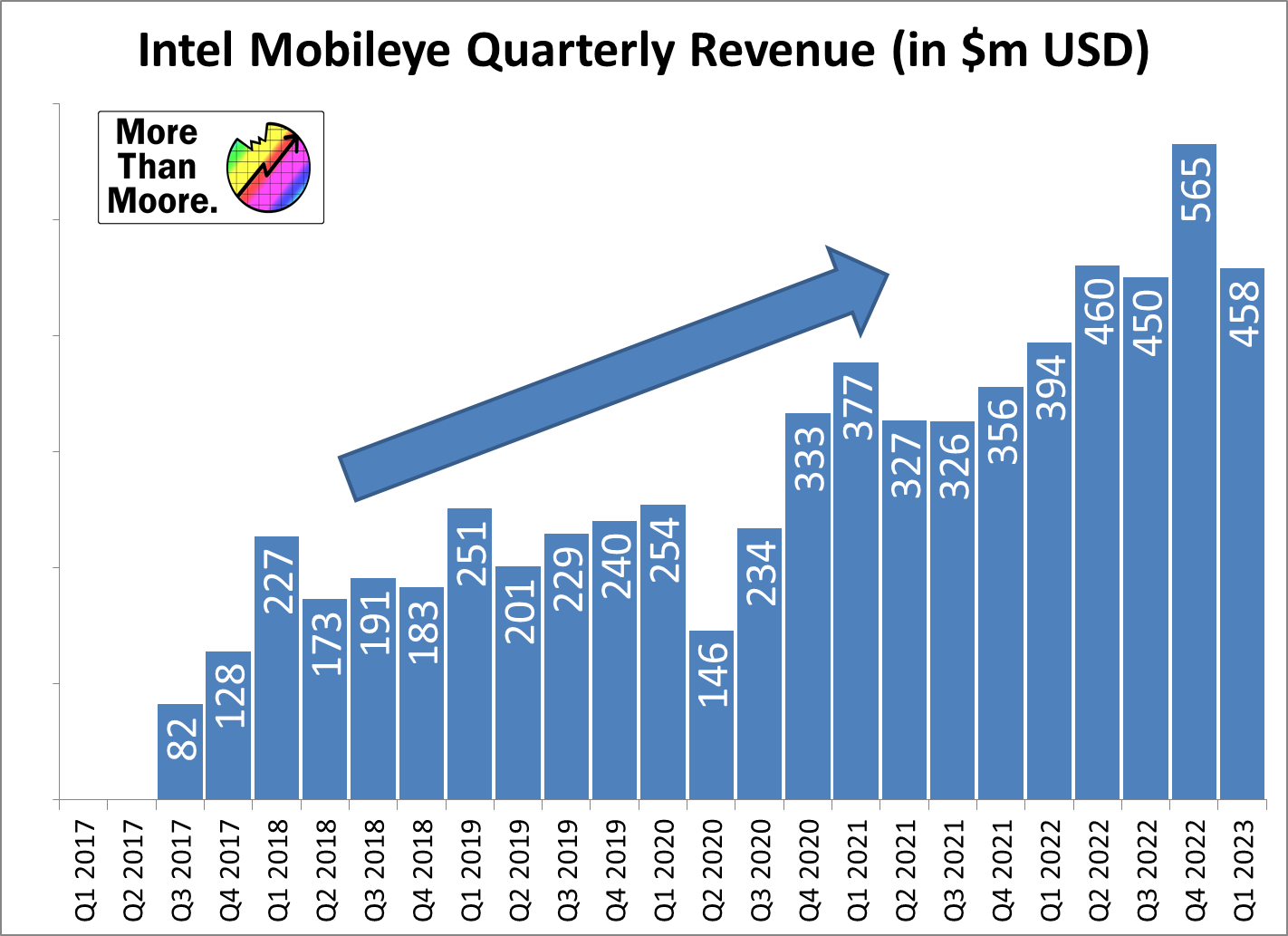

MBLY, Mobileye vs Q1’22

Revenue $458 million, up from $394 million

Operating Income $123 million, down from $148 million

If there’s one division of Intel that is at least consistent, it has been Mobileye. Revenue is up, which is good and Intel attributes that to higher demand for EyeQ, but operating income is down, which Intel attributes to investment in the future product portfolio. We know that Mobileye has been working on bringing the costs of LIDAR down, and has two significant new silicon products due in the market over the next few years: EyeQ6 and EyeQ Ultra, which help simplify solutions at lower power as well as providing more capability.

I updated this graph from the last quarter version, and while the Mobileye revenue is down QoQ, it is still an upward trajectory.

IFS, Intel Foundry Services

Revenue $118 million, down from $156 million

Operating Income loss of $140 million, down from $23 million loss

With the movement of automotive foundry into the ‘Other’ category, IFS is still getting some revenue due to licensing and the current deals it has with specific partners. There is likely some investment going on with big players who want to perhaps get access to future foundry nodes – big names to express interest include Qualcomm, Mediatek, and Amazon, with Amazon already using Intel’s packaging. The fact that foundry is quite small still belies the fact that Intel’s manufacturing operation is massive, and at some point that is going to shift as both IFS and CCG/DCAI/everything will get its own margin divisions.

One of the key things missing from IFS right now is Intel’s acquisition of Tower Semiconductor. It was meant to have completed for the Q4 financials earlier this year, but we’re still waiting for it to complete and pass regulatory hurdles. As I’ve stated several times before, people seem to get confused as to why Intel is buying Tower. Tower is a ~2m wafers/year business, mostly legacy process nodes and technologies, with thousands of customers and a low gross margin overall, even for a foundry. But therein lies the value – Tower has experience in managing thousands of customers, the supply chain economics, and has a wealth of partners who might be willing to jump onto Intel’s offerings with a familiar guiding hand. Intel’s economy of scale can improve Tower’s base business, of that I have no doubt, but the value in Tower is the expertise of running foundry.

There has been speculation as to why Tower hasn’t completed. As far as we’re aware, the hold-up to close out this acquisition is still China. But there seems to be some fine lines with this – China wants Intel to invest in the fabs on their soil, whereas one of the dependencies for parts of the CHIPS Act money may be limited-to-zero investment in semiconductor manufacturing in China. If the Tower doesn’t complete due to regulatory issues on Intel side, the agreement has a $353m clause payable from Intel to Tower. The date for that original clause was February 15th 2023, but we believe that has been extended six months.

Ultimately, Intel could do foundry which CHIPS money and without Tower, but they’ve tried going it alone before and a problematic 10nm node screwed over some major players according to reports. They could instead acquire Tower and not get any CHIPS Act money, but then that money would likely end up in the hands of direct competitors, and I have to assume that some of Intel’s balance sheet is reliant on getting a chunk of change, however sizeable, from the government.

I would also add on this point that Intel and Arm made a recent announcement about enabling Arm cores on Intel’s 18A process. It’s listed in the reports from Intel this quarter as ‘low power compute SoCs’, which to Intel could easily mean smartphones, but we should provide some color on this. Arm is an IP company, and it benefits from having validated IP at all the various foundries for its customers. If Arm can guarantee that its latest Cortex core works with PDK version 2.3 at foundry XYZ, that allows Arm’s customers to approach that foundry with a design that leverages the PDK and cost structure. This means that the agreement with Arm is a minor thing for Arm – they already have plenty of IP validated at every other foundry. But for Intel, it’s a big deal. There are thousands, tens of thousands, of Arm customers that would like another foundry option. But, as I’ve said before, if Intel is only going to offer its latest high-performance process nodes for foundry, then it’s going after the big fish, not the smaller customers. More on this for paid subscribers later.

Other

Revenue $165 million, down from $268 million

Operating Income loss of $1.153 billion, down from loss of $315 million

As stated repeatedly, the other number now includes Silicon Photonics and Automotive Foundry. This segment has a sizeable drop in revenue, but now has the largest operating income loss out of all the divisions. Intel does not go into why this is the case, and do not even address it in the financial opening statements, which I find kind of odd. It might come down to write-downs of the various shuttered departments and the loss of supply agreements, but who knows.

Important Aspects in the Filing

Aside from the BU breakdown, there are some other segments in the 10-K worth highlighting

Inventories $12.993 billion, down from $13.224b vs Q4’22

$160m less raw materials, now $1.358b

$150m less work in progress, now $7.415b

$78m more finished goods, now $4.220b

Accounts Receivable $3.847 billion, down from $4.133 billion in Q4’22

I put these in for discussion as during the Analyst Q&A, PG stated that Intel ideally aims for 150 days of inventory. Nominally it was inferred that he’s referring to finished goods, and that sum will adjust for the specific mix of products ready to go. The talk on the call was about bringing down that inventory, and despite fewer raw materials and work in progress, finished goods is still higher. A cursory reading might suggest that Intel actually has more finished goods ready to go today than they did last quarter, despite under production. Then again, we have to match this up with the comments regarding building pre-PRQ silicon for upcoming launches such as Meteor Lake and Emerald Rapids, so it also depends on the progression of those two product ramps.

Property, Plant and Equipment Net $85.734b, up from $80.860 billion

Additions to Property, Plant and Equipment in Q: $7.413 billion

Net Capital Expenditure of $7.0 billion

Free Cash Flow loss of $8.8 billion

‘Gross CapEx weighted in 1H, offsets in 2H, with FCF to improve QoQ’

Intel is consistently talking about their capital expenditure strategy with its fab roll-outs. The cost to build or extend fabs is high, and falls under all three segments of property, plant, and equipment. Intel has made multiple public commitments, such as Ohio, Germany, Italy, and expansions at current facilities. We’re also seeing a change in how equipment is depreciated, with last quarter showcasing it was extending from the standard 5 years to 7-8 years. So while Intel has a $7.4 billion investment in the quarter in new property, plant, equipment, the net value only went up around $5.0 billion. The additional spend will decrease through the year.

GAAP Net Income loss of $2.8 billion, down $10.9 billion YoY

Total debt: $48.836 billion, up from $37.684 billion in Q4’22

Issuance of long-term debt: $10.968 billion

One thing that also popped out of the page for me was the substantial drop in net income – a $10.9 billion loss year on year, even with the macroeconomic factors and shrinking markets. But one byline almost hidden in the filing is the debt issuance – Intel generated almost $11 billion of capital through long-term debt issuance. Yet despite this, they still came out with a free cash flow loss of $8.8 billion. Perhaps this isn’t a massive thing to think about – Intel is only increasing its debt burden by 30%, and is clearly leveraging its facility build-out for future potential. It is worth noting that Brookfield is taking half the risk at the Ohio facility, unconfirmed reports state that deeper discussions are needed in Germany, and Intel is still probing the US and EU governments for money from the various CHIPS acts or equivalents.

Guidance 2Q23

Revenue of $11.5-$12.5 billion, down 22% YoY

Non-GAAP Gross Margin 37.5%, down 730 bps YoY (with 5.1% of headwinds)

GAAP GM of 33.2%

Non-GAAP EPS of ($0.04), down 114% YoY

GAAP EPS of ($0.62)

For the guidance, Intel is guiding slightly higher on revenue for Q2, but slightly lower in GAAP gross margins, which would also be their lowest GMs in my spreadsheets that Intel has ever had. Intel does offer multiple explicit points regarding its outlook:

Lifespan of equipment was extended from five to eight years in Jan 2023, with depreciation expenses expected to be reduced by $4.1 billion in 2023.

As a result:

$2.3 billion increase to GM

$0.4 billion decrease to R&D

$1.4 billion decrease to ending Inventory

Q2 guidance includes

$0.5 billion benefit to operating margin from this

$0.10 benefit to EPS from this, split 80/20 to cost of sales and OpEx

The equipment depreciation will not count towards targeted cost savings ($3b in 2023, $8-10b exiting 2025)

This means that if we compare pre-and-post depreciation metrics, expected revenue outlook is down sequentially. Intel initially said that Q1/Q2 are going to be the weakpoints of 2023, and when you peer through the numbers, we’re really starting to see it, especially during a period of intensive capital spending.

After the split for paid subscribers, I have some additional thoughts on Intel’s position, as well as a full rundown of the Analyst Q&A in the call. I’ll also cover roadmaps and quarterly highlights.