Arm's 2025 Q3 Financial Results

Record Royalties, Big Uptick in Licensees

Companies mentioned: ARM 0.00%↑, NVDA 0.00%↑

As the idiom goes: a rising tide lifts all boats. And that is certainly the image that Arm is projecting for their Q3’2025 earnings report. Citing the AI boom as being a major driving factor to the company’s recent growth, for their latest quarter, Arm has set fresh records for both total revenues, and critically, royalty revenue, underscoring the company’s ability to tap into new market growth opportunities.

The renowned IP provider continues to occupy an interesting spot in the global chip landscape. The company’s IP is at the heart of everything from tiny microcontrollers to smartphones to powerful server processors, with the latter being responsible for much of their recent growth. This gives Arm a unique position, even among pure play IP providers, of having a stake in countless tech segments big and small.

That breadth of reach does mean that Arm has to fight battles on several fronts to maintain its total market share. The RISC-V ecosystem remains a constant competitor for Arm, and particularly threatens Arm’s microcontroller market share. Meanwhile at the other end of the spectrum, well-funded chip designers have increasingly seen it fit to develop their own Arm-based CPU cores. So while the shift from x86 to Arm-based chips in servers has netted Arm new revenues, Arm has also needed to contend with a change in royalties when those customers move from using one part of Arm’s offering to another. All of which means Arm has to very carefully navigate its path in order to continue to grow its IP business.

Which for their recent quarters, at least, Arm has done very well for themselves. The company has set multiple revenue records in the past several quarters, and for Q3’25, they’ve done it once again.

Key Takeaways (GAAP)

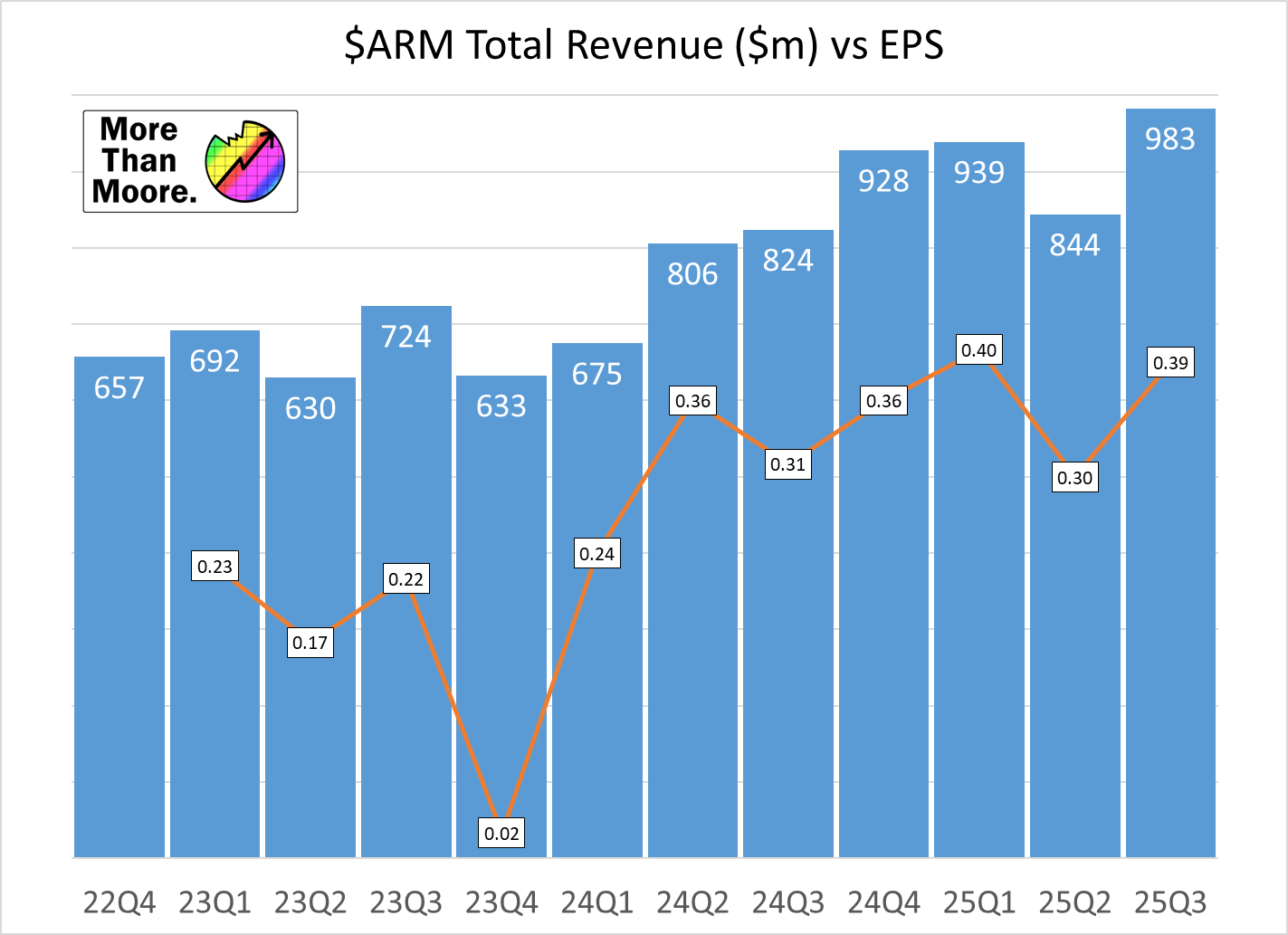

💵 Q3 Revenue, $983m, up 19% YoY from $824m and up 16% QoQ

📈 Q3 Gross Margin at 97.2%, up 1.8pp YoY and up 1.2pp QoQ

💰 Q3 Net Income of $252m, up 190% YoY from $87m and up 136% QoQ

🪙 Q3 EPS $0.24, up 200% YoY, up 140% QoQ

Highlights

💵 Record Quarterly Total Revenue

💵 Record Quarterly Royalty Revenue

📈 R&D Spending Up 23% YoY

📈 Headcount: 7,923, Up 15% YoY

Financial Overview

For the third quarter of Arm’s 2025 financial year, the IP provider booked $938m in revenue. This was a 19% increase year-over-year, and a new record for the company, beating out their previous revenue record of $939m set all the way back in Q1’25.

Because of the pure play nature of Arm’s IP business, virtually all of the company’s gross income is profit, and Q3’25 is no exception. For the quarter Arm recorded a GAAP gross margin of 97.2%, a 1.8pp increase over Q3’24. Meanwhile, even after the significant operating expenses of running an IP provider – including $533m in R&D– the company still closed out the quarter with improved operating margins as well. Compared to the year-ago quarter, Arm’s operating margin increased to 17.8%, for a total operating income of $175m.

More significant gains can be found in Arm’s net income, which hit $252m for the quarter. This is a massive improvement over the year-ago quarter, where Arm only booked $87m in net income. Diving into Arm’s financial statements, while their improved operating income is one big contributor to this growth, the quarter also saw Arm reap the benefits of equity investments and income from interest, all of which has pushed Arm’s net income to over a quarter billion dollars for a single quarter.

Arm’s strong Q3 results also mean that the company has beat their guidance from the start of the quarter. Whereas the top end of Arm’s guidance was $970m, the $983m that Arm actually booked has beat that by over $10m. And on the spending side of the equation, Arm has managed to keep non-GAAP operating expenses a hair below projections as well, spending $522m versus a projected $525m.

Breaking down Arm’s earnings a bit, the company organizes its revenues under two business units: royalty revenue, and then license and other revenue (software, services, support). According to Arm, both came in ahead of their expectations, and as previously noted, Q3 is an outright royalty revenue record for the IP company.

Finally, it’s interesting to note that Arm has significantly expanded their R&D spending and headcount over the past year. The $533m that Arm spent in R&D in Q3’25 is a 23% increase over their Q3’24 spending. And similarly, the company has added another 15% to its headcount over the past year, including over 1,000 engineers. So while the company's revenues are up significantly, the company is also plowing a lot of those gains back into product development.

ARM vs QCOM

Notably, throughout all Arm’s earnings report and prepared remarks, there is no mention of the company’s ongoing lawsuit against Qualcomm - although it is likely mentioned when the 10-K is released. The two companies, long at loggerheads over licensing and royalties, finally went to court last year. While the December ruling in that case didn’t settle all of the claims, Arm lost the major claim that Qualcomm was underpaying Arm on royalties. Meanwhile it remains to be decided whether Nuvia broke its architecture licensing agreement with Arm in the process.

For a podcast breakdown of the interim results of the lawsuit, you can catch it here on The Tech Poutine #13 (a podcast between More Than Moore and Chips and Cheese) around the 10 minute mark.

The topic was addressed in the analyst Q&A, with Arm stating that their predictions since IPO have been ‘forecast as though we were not going to prevail in that lawsuit’. This is quite eye-opening to be honest, and we’re wondering if this is a change in messaging. It makes sense from a financial perspective for sure, but it does open a bit of honesty into the mix. Arm goes on to say that ‘we had assumed that we’ll continue to be receiving royalties [at] basically the same rates that they’ve been paying for in the past’ - which we assume is something along the lines of Arm’s v8 TLA licensing rates.

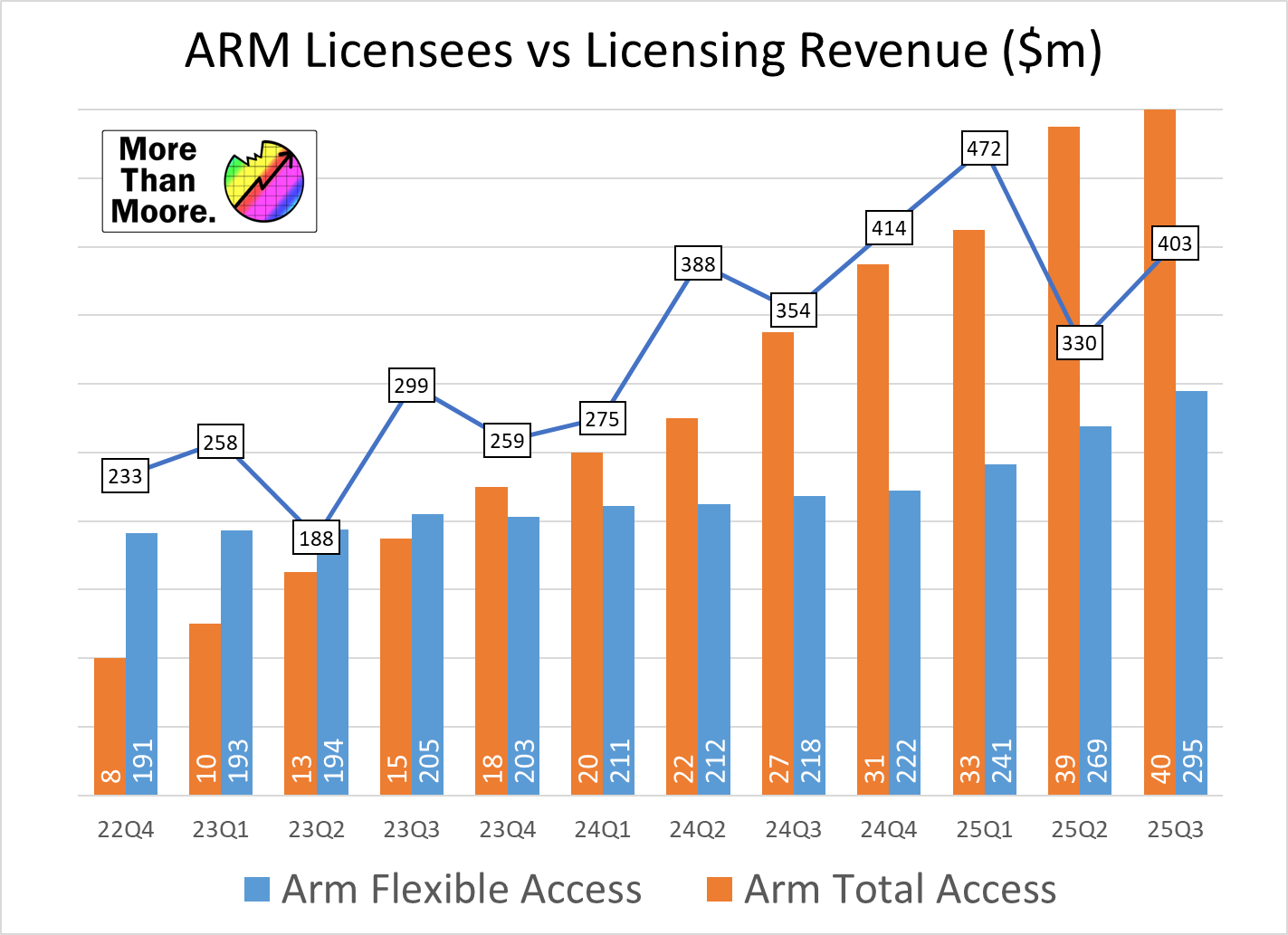

Licensing and Other Revenue

💵 Q3 Revenue $403m, up 14% YoY

Starting with Arm’s Licensing and Other Revenue category, this is traditionally the more volatile of Arm’s two business categories. As it’s not directly tied to hardware shipments or other client hardware success, it varies quite a bit based on when companies sign new or updated license agreements.

Nonetheless, licensing and other revenue was up 14% year-over-year, hitting $403m for the quarter. This isn’t a record for the category, but according to Arm, it is ahead of their expectations.

Digging a bit deeper, Arm’s breakdown on license sales shows that the company has sold new licenses for both its Arm Total Access and Arm Flexible Access license plans. The company sold 1 new Arm Total Access license in Q3, bringing the total to its all-encompassing license plan to 40 active (extent) clients. Meanwhile the company has sold a further 26 of their R&D-focused Arm Flexible Access licenses, bringing that total to 295 - a sizeable jump within a single quarter.

Royalty Revenue

💵 Q3 Revenue $580m, up 23% YoY

Arm’s second major revenue category – and in most quarters, the larger of the two – is Arm’s royalty revenue. Directly tied to the success of clients’ chips and the volumes shipped thereof, Arm’s business model thrives on royalties, especially as the long-term nature of these agreements means that Arm can still collect significant revenues for IP designs 10+ years old.

For the third quarter of Arm’s 2025 financial year, Arm recorded $580m in royalty revenues. This was up 23% from the year-ago quarter, when Arm booked $470m in revenue. It’s also a record in royalty revenues for the company – and significantly so – besting Arm’s old Q4’24 record by $66m.

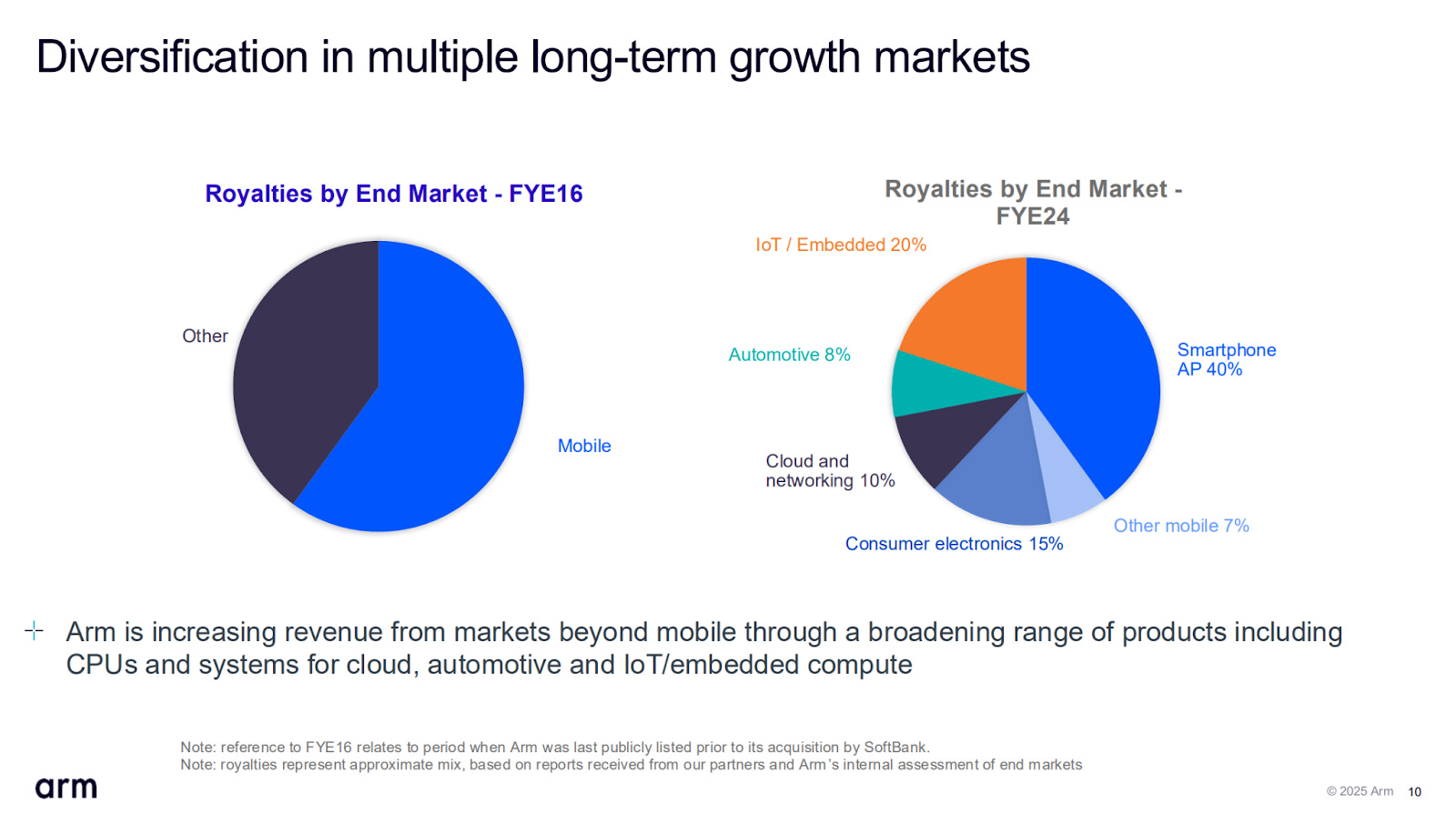

Arm is attributing the bulk of the growth in royalty revenues to four major areas. First has been the increased adoption of the Armv9, which fetches higher royalties per unit than old architectures.

While Arm doesn’t offer an iso-comparison to Q3’24, Arm v9’s percentage share of revenue for Q3’25 is more than 25%, well ahead of the average for FY2024. Though on a quarterly basis for FY2025, things have changed very little in the last couple of quarters, underscoring how the Arm ecosystem is large and relatively slow moving overall. CEO Rene Haas highlighted strong adoption of v9 with its smartphone customers, such as Mediatek in the Dimensity 9400 now found in Oppo and vivo devices. In the analyst Q&A, CFO Jason Child commented that the expectation is v9 to grow to 67-70% of royalties at peak over time.

The second major contributor to Arm’s royalty growth has been the sales of the company’s Compute Subsystems (CSS), pre-assembled IP blocks that include not only Arm CPU cores but other bits of IP, allowing companies to skip that part of the integration process and bring products to market sooner. CSS designs feature more Arm IP, and in line with the additional work Arm does in assembling them, they fetch higher margins per chip than just licensing Arm’s CPU cores or other IP. Arm has 12 CSS licensees thus far, which according to the company is a faster rate of adoption than they were initially expecting. In the quarter, the major contributor to this part of the revenue was Mediatek's Dimensity 9400, with Microsoft Cobalt revenue also starting in the quarter. Additional information on the momentum of CSS designs will be defined on next quarter’s call.

The third major contributor – and the one Arm is most happy to point out – has been the continued growth of Arm CPU usage in the data center space. This goes for both general servers, and in AI systems. In the case of the latter, Arm doesn’t have a high-performance accelerator IP of its own; but because CPUs are still needed to drive AI-focused systems (e.g. Grace + Blackwell), AI system sales still drive the sale of Arm-based chips, all of which pays out as royalties for Arm. Customers (and their chips) in this area include AWS Graviton, Microsoft Cobalt, and Google Axion. Network switch vendors and custom ASIC providers are also using the underlying Neoverse cores to build designs. Arm was keen to point out that >50% of Amazon Web Services new CPU capacity over the last two years was on Arm-based Graviton processors.

Finally, for its fourth and final contributor, Arm is reporting that IoT royalties have improved as well. The company isn’t offering much in the way of details here – whether the growth is mostly coming from higher per-unit royalties or higher chip volumes – but either way, it all adds to Arm’s record royalty revenues.

On the call, a key point was mentioned in the analyst Q&A:

‘The royalty rate of CSS is roughly double that of v9’

‘v9 is roughly double the royalty rate of v8’

‘CSS 2026 royalty rates are not necessarily the same as CSS in 2025 - those rates change year on year when a new solution is offered into the market’

This goes some way into understanding the push of Arm to drive CSS adoption.

Also, it was stated that 25% of licensing revenue is from China.

Outlook, Q4 2025 & FY2025

Outlook is as follows:

💵 Q4’25 Revenue, $1.225b, +/- $50m

💵 FY2025 Revenue, $3.99b, +/- $50m

📈 Q4’25 EPS, $0.52, +/- $0.04

📈 FY2025 EPS, $1.60, +/- $0.04

Rounding out Arm’s Q3 earnings report is their guidance for the final quarter of the financial year, and for the total financial year itself.

At a high level, Arm is expecting significant revenue growth for Q4 on both a quarterly and yearly basis. The company is calling for between $1.175b and $1,275b in revenue, which would dwarf their record Q3, let alone the “mere” $928m in revenue that the company booked in Q4’24. If the midpoint of $1.225b comes to pass, this would represent a quarterly revenue growth of 25% and a yearly revenue growth of 32%.

Meanwhile, the close of Q3 means that Arm’s FY2025 guidance has been narrowed; essentially, the uncertainty in Q4’25 is also the uncertainty for FY2025. That means that Arm’s revenue guidance for the year is in the +/- $50m range, with a midpoint of $3.99b for the quarter and a non-GAAP EPS midpoint of $1.60. As with Q4, this would represent significant growth for the company, with revenues growing by 24% YoY, and EPS growing by 344% YoY. Which, looking at Arm’s guidance for FY2025 at the start of the year, would see Arm landing at the high-end of their original projections.

Past this, the nature of Arm’s business as a IP provider – and a broad one, at that – means that there is no one product or IP release that is going to immediately and uniquely drive sales for the company in the fourth quarter of their financial year. That means that Arm’s growth is going to be fueled by an amalgamation of many of the same factors that drove Q3 growth: data center chip royalties, expanding use of Arm CSS, and other higher royalty uses of Arm’s IP.

Addendum from Ian

Arm’s customer Mediatek had an interesting success last year with the Dimensity 9300 smartphone processor - while it didn’t sell outside of China much, the concept of the design had pivoted from other processors in this market. I highlighted some of the technical decisions (cores, cache) made by Mediatek with Arm IP as to why this chip could be the catalyst to some further innovation for the future of Android smartphones into 2025 and 2026. I created a video explaining the change and why it matters on a wider scale for the premium smartphone market.

More Than Moore, as with other research and analyst firms, provides or has provided paid research, analysis, advising, or consulting to many high-tech companies in the industry, which may include advertising on the More Than Moore newsletter or TechTechPotato YouTube channel and related social media. The companies that fall under this banner include AMD, Applied Materials, Armari, ASM, Ayar Labs, Baidu, Dialectica, Facebook, GLG, Guidepoint, IBM, Impala, Infineon, Intel, Kuehne+Nagel, Lattice Semi, Linode, MediaTek, NextSilicon, NordPass, NVIDIA, ProteanTecs, Qualcomm, SiFive, SIG, SiTime, Supermicro, Synopsys, Tenstorrent, Third Bridge, TSMC, Untether AI, Ventana Micro.

| A guest post by

|

Excellent post!

The key problem ARM still has is the relatively low EPS given the shares' valuation. That is especially noteworthy for a company built on IP licensing, so very low running costs or needed CapEx. It's hard to see how they will get those royalties to go up drastically. And, ARM and its team badly fumbled their lawsuit against Qualcomm, turning what many thought to be a highly likely win into a resounding loss, at least for this round.