Companies mentioned: AMD 0.00%↑, INTC 0.00%↑, NVDA 0.00%↑

After the last few year’s we’ve had, the question on everyone’s lips is if this modern environment has stabilized the market for silicon products, or whether it’s still going to be varied. We’ve gone through boom and bust, talks of 340-360m units/year in consumer being pulled back to 200m then back up again, and whether the enterprise, cloud, or embedded market are feeling the same effects at the same time. 2023 was a year of two halves, depending on which company you spoke to. The advent of AI didn’t stop some serious regressions beyond seasonal falls in the first half of the year, and the question was if that was market forces or simply inventory digestion, with recovery in the second half of the year. AMD is a company that experienced some of that headwind in 1H, but 2H is showing some record numbers.

Before we get into the numbers, CEO Dr. Lisa Su had some prepared remarks on the release, some of which raised a few eyebrows. In particular, the statement that the AI silicon market will be $400b by 2027. The analysts asked about this below the fold.

Overall Results

But the headline numbers are as follows:

💰 Q4 Revenue of $6.168 billion, up 10% year-on-year

💰 FY Revenue of $22.680 billion, down 4% year on year

📈 Q4 Gross Margin of 47%, up 4% year-on-year

📈 FY Gross Margin of 50%, down 2% year-on-year

Showing AMD’s long term revenue charts, we have AMD’s second best quarter ever in Q4 2023. $6.168 billion in a single quarter is more revenue than AMD made in the whole of 2017 ($5.25b). However, the number one quarter, Q2 2022, was during a time of significant boom, whereas Q4 2023 is more akin to a ‘typical’ quarter, indicating AMD’s current portfolio and product strength. That Q2 2022 number also skews the FY22 vs FY23 numbers. One thing worth pointing out here is the gross margins – AMD has been able to keep around to 50-51%, even with increased revenues the past two quarters.

The main reason for AMD’s big performance in Q4 is due to its Data Center BU. In 23Q4, the business unit had its best quarter ever, riding high on the strong performance of the server processor line – EPYC 3rd Generation (Milan) and EPYC 4th Generation (Genoa, Bergamo) are co-existing in the market with a competitive offering. In AMD’s disclosure, call, and follow-up, AMD is confident it has more than 30% of the market for its data center products, and with specific key cloud providers, they have more than 50% of the CPU business. This is a record quarter, even though its AI product MI300X is minimal revenue for now (at least, compared to what it should be by Q4 2024).

Data Center

Q4 2023

💰 Revenue $2.282b, up 38% Year-on-Year

📈 Op Margin 29%, up 2% Year-on-Year

💵 Income $666m, up 50% Year-on-Year

FY 2023

💰 Revenue $6.496 billion, up 7%

💵 Op Income $1.267 billion, down 31%

AMD launched its fourth generation EPYC in Q4 2022, which means during 2H23 we’re seeing revenues grow for that product line as it ramps up – AMD has been clear that its 3rd and 4th generation products will co-exist in the market, feeling that they offer different enough value propositions. One of the reasons for that is 3rd Generation is still using DDR4 memory, whereas 4th Generation is a new platform using DDR5, and for modern high-capacity enterprise deployments, memory cost is bigger than the processor cost (it is shifting, however). Also, 3rd Generation uses a mature platform evolved from the previous two generations, whereas 4th Generation is a new platform, and so while there were some initial growth pains, those seem to have been stamped out. Over 2023, AMD launched Genoa-X, the V-cache product, Bergamo, the cloud density product, and Siena, for telecommunications, filling out the CPU roadmap by being very efficient with its chiplet strategy.

Also in the year, AMD’s MI250X has been the major ‘AI’ chip from the company. While picking up some wins, most publicly in HPC and supercomputers, AMD partners were using it as a chance to build up AI software and infrastructure ahead of the MI300 launch in Q4 2023. When I say launch, it’s more an announcement – AMD has two products, MI300A for HPC and MI300X for AI. In Q4, around $400m of revenue was attributed to a single sale of MI300A to the expected #1 supercomputer in the world, however not much revenue was expected from MI300X, which is expected to come through in 2024. Prior to this call, AMD had stated that they expect $2b revenue from MI300X in 2024 – that has since increased to $3.5b revenue, however some analysts are quoting higher than that. AMD states that it does not have supply chain issues for its MI300X, and these revenue estimates are due to confidence with how its MI300X partners are progressing and expected orders. That being said, CEO Dr. Lisa Su was careful to note in the analyst Q&A that anyone ordering MI300X today, the lead time is around 5-6 months. That’s still less than the main competitor NVIDIA, but confirms that AMD expects its MI300X revenue to be H2 weighted in 2024. AMD confirmed this on the call.

For some forward looking, AMD stated that EPYC 5th Generation, Turin, will be launching in 2024.

Client

Q4

💰 Revenue $1.461b, up 62% Year-on-Year

📈 Op Margin 4%, up 21% Year-on-Year

💵 Income $55m, up from $152m loss Year-on-Year

Client FY 2023

💰 Revenue $4.651 billion, down 25%

💵 Op Income $46m loss, down from +$1.190b

Comparing 23Q4 to 22Q4 for the client computing part of AMD is night and day, and that’s simply because the group had such a bad 22Q4. Over the past twelve months, AMD has filled out its desktop CPU portfolio, offering more cost effective options and processors with more cache, but also the notebook side of the company is making some good sounding waves. AMD was the first x86 notebook vendor to offer an integrated AI engine, called an NPU, into their notebook processors. Now this is a double-edged sword – while I don’t think it drove any sales specifically, AMD is keen to point out that they have up to a million NPU-enabled PCs in the market already, ahead of Intel. This is despite AMD only releasing its software development kit public in late Q4 2023.

If we look at the full-year numbers, client looks like it fell hard. This is because 1H23 was rough for client. I said in the intro about how the market shifted predictions from 340-360m units a year in 2022, to a massive dip of 200m units a year in Q1 2023. This meant that every laptop and desktop vendor had way too much inventory. In order for the inventory to realign, they stopped buying – so AMD (and others) were hit double: customers weren’t buying the increased amount, but they also weren’t buying the regular amount because they had too much. The industry calls this digestion, and all consumer focused products felt the acid reflux in 1H23. The FY22 vs FY23 look doubly bad because FY22 was also a really good year for client sales.

Looking forward, similar to data center, we’re expecting the next generation of Ryzen desktop processors in 2024. The newer generation of notebook processors, the 8040 series, were just launched.

Gaming

Q4

💰 Revenue $1.368b, down 17% Year-on-Year

📈 Op Margin 16%, flat Year-on-Year

💵 Income $224m, down 16% Year-on-Year

Gaming FY 2023

💰 Revenue $6.212 billion, down 9%

💵 Op Income $971m, up 2%

AMD’s Gaming business unit covers all the graphics products but also the gaming-focused semi-custom wins. AMD has three big wins in semi-custom: Sony’s Playstation, Microsoft’s Xbox, and now Valve’s Steam Deck. For the Playstation and Xbox, we are currently in the 4th/5th year of a console cycle. In the past couple of years, due to the pandemic, the demand for consoles has been better than expected, however we are now entering a typical 5th year for the consoles, following the 7-8 year cyclical nature of previous console generations. The Steam Deck is an interesting blip in this, however AMD is clear that Q4 gaming revenues are down due to semi-custom sales, but note that the full year numbers are up due to increased Radeon sales. Over 2023, AMD has added to its Radeon 7000 RDNA3 graphics portfolio, filling out all the spots and offering a price competitive option to NVIDIA in a number of key segments.

In terms of outlook, AMD is clear that it has inventory at customers, and is expecting significant declines in Q1 on top of seasonality.

Embedded

Q4

💰 Revenue $1.057b, down 24% Year-on-Year

📈 Op Margin 44%, down 6% Year-on-Year

💵 Income $461m, down 25% Year-on-Year

FY 2023

💰 Revenue $5.321 billion, up 17%

💵 Op Income $2.628 billion, up 17%

The digestion period we saw for the other markets in 1H23 didn’t seem to affect the embedded market at the time, however we are now coming up to that point – both AMD and Intel are confirming that embedded customers are flush with inventory, and so they’re reducing their orders as a result. AMD’s Embedded team (which includes the Xilinx group) has had some massive quarters in 2023, and so this is a pivot away from those lofty numbers. AMD expects this to continue through Q1 and into Q2, however the company is buoyed by the AMD+Xilinx engagement taking shape. The goal of the Xilinx acquisition was always to pair AMD+Xilinx hardware into embedded sales, and the time for that taking off is going to be in 2024.

In terms of new products, the Embedded group recently announced Versal AI Edge XA and Ryzen Embedded V200A for automotive markets, and Embedded 7000 processors for industrial and edge.

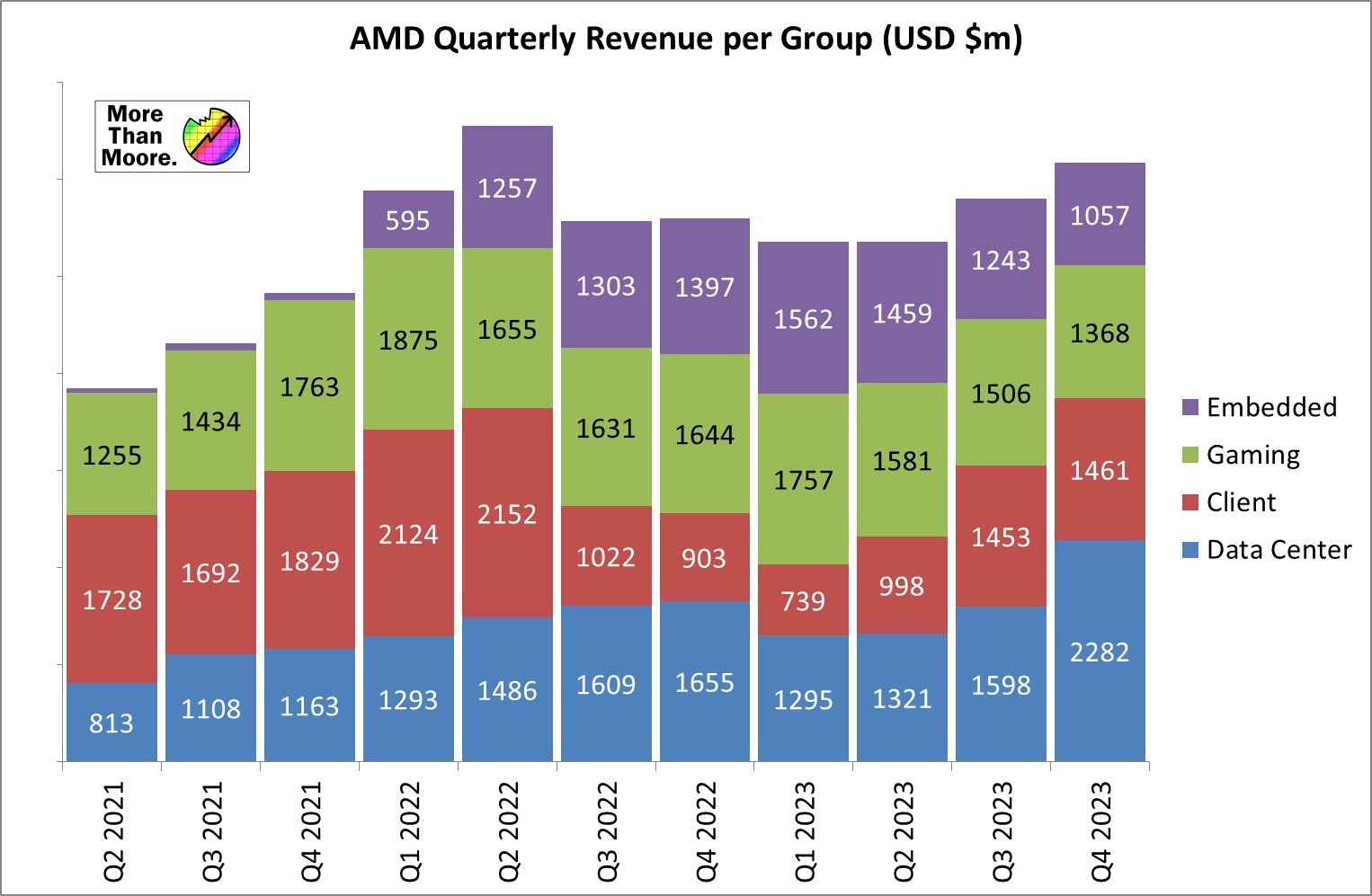

Here’s the quarterly revenue by group since 2021, and as mentioned, we can see that Data Center is having its best quarter ever. Client is far away from that record Q2 2022, however this was its best quarter since. Gaming, while at the lowest point since Q2 2021, isn’t actually too far off, but that console cycle does have a significant effect. Then with embedded, we’ve noted the digestion that’s happening, and it will take at least another quarter (or two) to perhaps realign.

I created this chart to show that DC is taking a bigger portion of the pie. In Q4 2022, it was roughly 30/25/30/15, and now it’s 40/15/25/25. As we go into 2024, that DC portion is likely to grow as AMD ramps up MI300X.

Financial Outlook, Q1 2024

💰 Revenue $5.4 billion, +/- $300m

📈 Gross Margin 52%

💵 OpEx $1.73 billion

Q1 is seasonally weaker than the rest of the year – something that perhaps wasn’t always the case during the pandemic, but if anything is indicative of coming back to a regular cycle, this is probably it. Revenue of $5.4 billion is down around $700m quarter-to-quarter, but in line with Year-on-Year metrics. The upside is the ramp of MI300, the downside is the Embedded digestion. It looks worse when I plot it on a graph.

But on the plus side, the predicted gross margin is higher.

Below the fold is the transcript from the Financial Analyst Q&A that occurred after the call.

I should also note that a couple of days after the financial disclosure, AMD CEO Dr. Lisa Su held an tech analyst Q&A (i.e. for people like me). I’ll be posting the results from that call, and the analysis, in a future article for paid subscribers only. Lisa is wonderfully direct in these sessions, so it’ll be worth a look.