AMD Q4 2024 and FY Financials

Up and to the right

Love it or hate it, the AI boom has resulted in a massive shake-up amongst the major chip firms. The rapid expansion of high-margin, high-powered hardware purchases has been a boon to several companies that have been able to successfully navigate the rapidly changing environment and get their wares in the hands of hungry hyperscalers. While the Big Green usually sucks most of the air out of the room, AMD is playing a strong hand and has the financial results to show for it. This year is a record year for AMD 0.00%↑ ’s revenue, and we also see record quarterly data center and client revenue as well.

As we’ve said time and time again, AMD has been on a tear in the last several quarters – and has continued that tear for quarters to come. Driving a lot of that has been AMD’s Instinct MI300 series of accelerators – AMD’s core AI product – which saw their first full year of sales in FY2024. With AMD ramping up production there, the company has seen its data center sales blossom, all to the benefit of the company’s bottom line. Coupled with strong growth in AMD’s CPU product categories – EPYC for servers and Ryzen for consumer hardware – and AMD is certainly living large as of late.

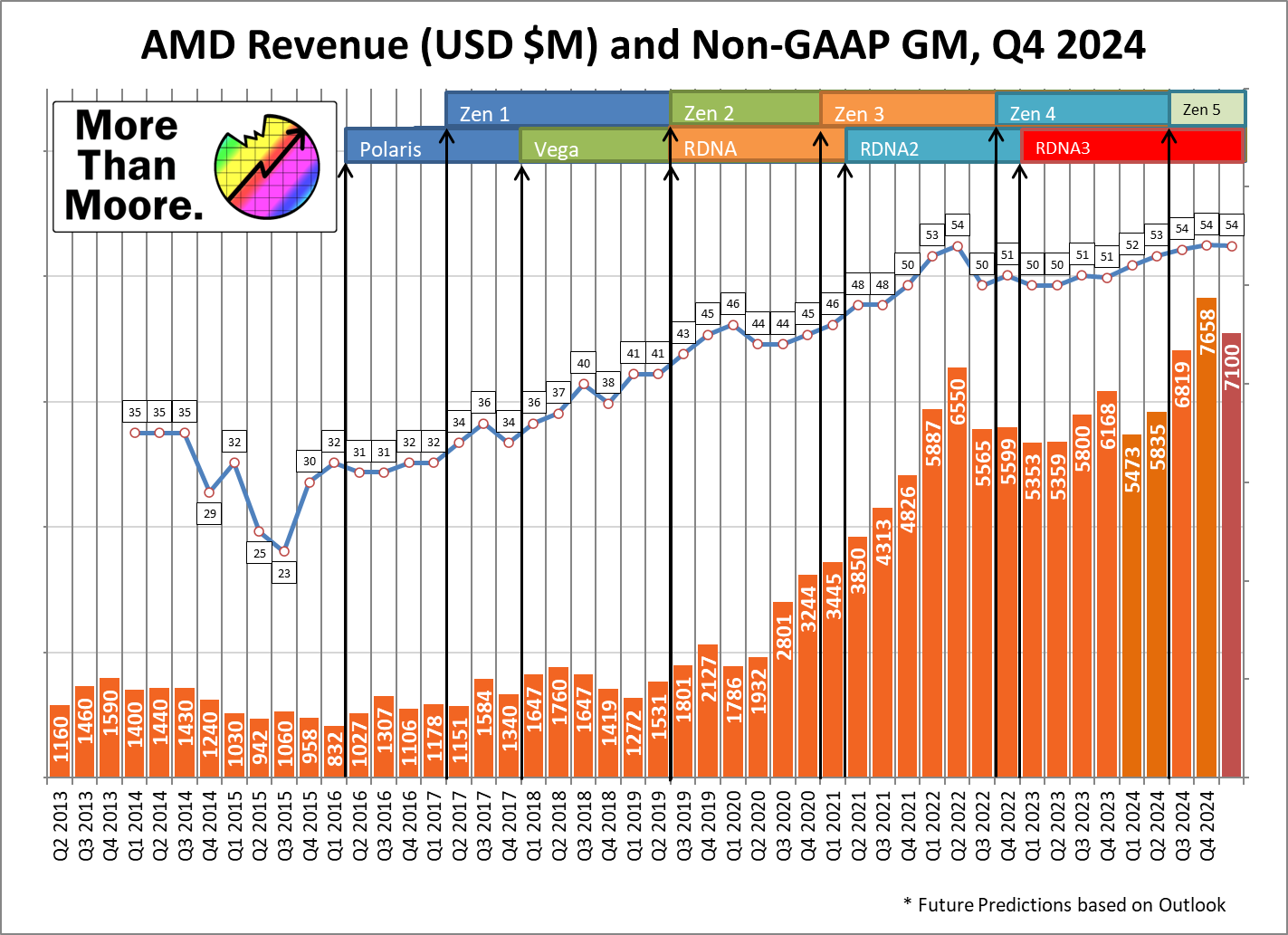

Wrapping up the end of their 2024 financial year, AMD’s financial sheets are once again repeating that chorus. With Q4’24 revenues up 24% year-over-year and full-year revenues up 14%, AMD is closing the book on another record year for the company.

Key Takeaways (GAAP)

💵 Q4 Revenue, $7.66b, up 24% YoY from $6.17b and up 12% QoQ

💵 FY Revenue, $25.8b, up 14% YoY from $22.7b

📈 Q4 Gross Margin at 51%, up 4pp YoY and up 1pp QoQ

📈 FY Gross Margin at 49%, up 3pp YoY

💰 Q4 Net Income of $482m, down 28% YoY from $667m and up 37% QoQ

💰 FY Net Income of $1.64b, up 92% YoY from $854m

🪙 Q4 EPS $0.29, down 29% YoY, down 38% QoQ

🪙 FY EPS $1.00, up 89% YoY

Highlights

💵 Record Quarterly Revenue.

💵 Record Data Center Revenue

💵 Record Client Revenue

(in fact, Q4 DC revenue is higher than 21Q2 full revenue)

➡️ MI350X is being pulled in from the second half of 2025 to mid-2025.

Financial Overview

Closing out AMD’s final (and traditionally strongest) quarter of the year, the company booked $7.66b in revenue. Compared to Q4’23, that’s a 24% improvement in just a single year. And it’s not just AMD’s top-line revenue that has grown, either – the company’s gross margins have further improved, with AMD hitting 54% for the quarter. So on both a revenue and operating cost basis, Q4 has been very good to AMD. They beat both the previous quarterly guidance for revenue and margin, as well as the street expectations.

The only real blemish on an otherwise exceptional quarter are AMD’s GAAP net income and resulting EPS, which took a hit this quarter. The company once again took an amortization charge for acquisition-related intangibles (i.e. Xilinx), which knocked $584m off of their bottom line. AMD expects this to continue for several years. Q4 also saw significant-but-usual charges for employee stock compensation ($339m) and income taxes ($152m). Otherwise the most significant irregular charge was a one-off restructuring charge of $186m for AMD’s November layoffs, which saw the company trim 4% of its workforce. As a result, there’s a significant gap between GAAP and non-GAAP net income, with the GAAP reconciliation devouring about $1.3b of AMD’s $1.78b of non-GAAP net income.

Otherwise, if you’re focused purely on the company’s core non-GAAP performance, then even that was another win for AMD. The $1.78b of non-GAAP net income for the quarter was up 42% year-over-year and 18% QoQ, eclipsing AMD’s overall revenue gains. As we’ll see in the business unit breakdown, this boost in margins and profitability has a lot to do with AMD’s product mix, which is seeing AMD derive more and more of its revenue from high-margin products – while also undergoing a similar drop in low-margin products.

Overall, AMD’s Q4 financial results were right on target with the company’s previous projections for the quarter. At the end of Q3, AMD called for $7.2b to $7.8b in revenue for Q4, with $7.7b falling in the high-end of that range. Meanwhile the non-GAAP gross margin of 54% was a bullseye for AMD, matching their Q3 projection.

As for AMD’s full-year results, it’s much the same story, but with larger numbers. The company booked $25.8b in revenue for FY2024, which was up 14% YoY. And undoubtedly to investors’ delight, all of AMD’s profitability metrics were up even more significantly compared to FY2023. GAAP gross margin for FY2024 hit 49%, up from 46% for the year-ago period. And net income nearly doubled, coming in at $1.64b for the year. As a result, AMD’s EPS has cracked a dollar a share for the first time, coming in at exactly $1.00.

Finally, taking a quick look at AMD’s business unit revenue and associated product mix, we can see how AMD has increasingly shifted towards higher margin products. AMD’s revenue split for Q4’24 has seen data center revenue eclipse all the company’s other major business units combined, cementing AMD’s shift towards becoming a data center-driven company.

Data Center: EPYC, Instinct

💵 Q4 Revenue $3.86b, up 69% YoY

💵 FY Revenue $12.6b, up 94% YoY

💰 Q4 Operating Income $1.16b, up from $666m YoY

💰 FY Operating Income $3.48b, up from $1.27b YoY

📈 Q4 Operating Margin 30%, up from 29% YoY

📈 FY Operating Margin 28%, down from 20% YoY

AMD’s flagship division has only continued to grow in its dominance of AMD’s financials over the past several quarters – and with its high margins, consequently the company’s profitability. As noted earlier, FY2024 has been the first full year of revenue for AMD’s Instinct MI300 accelerators, the first highly successful generation of accelerators from AMD. As a result, AMD has been able to grow its data center revenue by leaps and bounds over the past year.

By the numbers, AMD booked $3.86b in revenue under its data center group for Q4’24, which was up 69% YoY. With Instinct boosting AMD’s numbers, operating income and operating margins were up by even more, with AMD hitting a 30% operating margin and $1.16b in operating income from the group.

Unfortunately, AMD doesn’t provide an explicit break-out of GPU (Instinct) versus CPU (EPYC) revenue, but according to the company, EPYC has also done very well for itself for this quarter. With AMD having previously launched their Zen 5 CPU architecture and associated EPYC chips (Turin) in the later half of 2024, the company is reporting “strong growth” of EPYC CPU sales for Q4’24. They attribute that to the last three generations still finding good traction - 5th Gen Turin, 4th Gen Genoa, and 3rd Gen Milan. CEO Lisa Su stated that ‘we've expanded the design points of each of the generations - cloud native, enterprise optimized, performance, low core, perf/$’, which has been contributing to the increase. The other comment of note is that AMD now says it has >50% x86 CPU share with its hyperscaler customers.

And while MI300X sales have spent most of FY2024 ramping, AMD’s manufacturing efforts have already turned to the MI325X, which was launched in Q4 and is itself now further ramping as part of its volume production. The updated MI300 family part features HBM3E memory, allowing for both higher memory bandwidths and higher memory capacities for AMD’s flagship accelerator, helping to alleviate the memory bottlenecks typically associated with model training.

Looking at AMD’s data center numbers overall, the one surprise here is that, despite the explosive growth in sales of high-margin Instinct accelerators, AMD’s operating margin for the quarter was only 1 percentage point higher than the year before, at 30%. Digging through AMD’s financials and prepared remarks, it looks like AMD is investing a lot of those margins back into R&D, an expensive undertaking that the company will expect to pay even bigger dividends down the line. This includes both hardware R&D as well as software R&D, with the latter being especially notable as software has traditionally been a weak point for AMD compared to its rivals.

Looking forward, as part of today’s earnings release, AMD is offering a few choice updates on its data center GPU product plans for 2025 and beyond. First and foremost, AMD is pulling in the release of its MI350 accelerator. Previously scheduled for a H2’25 launch, AMD is bringing it in by roughly a quarter, as it is now scheduled for production shipments to go out “mid-year.”

Based on AMD’s CDNA 4 architecture, AMD is touting MI350 as the “biggest generation leap in AI performance in our history”. Under the hood, CDNA 4 will bring support for lower-precision FP4 and FP6 number formats to the table, which has become the latest optimization target for AI firms trying to squeeze out ever-more performance from their GPU racks. According to remarks from CEO Dr. Lisa Su, the early silicon for MI350 has come up “very well,” which coupled with customer interest have driven AMD to accelerate its launch.

Meanwhile, AMD is also confirming that MI400, its true next-generation successor to the MI300/MI325/MI350 families, remains on track for its 2026 launch. Still going by the architecture codename “CDNA Next”, AMD is reiterating its data center scale design goals and ambition to take industry leadership in terms of FLOPS.

It should also be noted that in the prepared remarks, CEO Lisa Su stated that the regulatory approval process for the acquisition of ZT Systems is going ahead smoothly, with the acquisition expected to complete later this year. AMD will divest the manufacturing part of ZT Systems after the acquisition.

Client: Ryzen, Ryzen Mobile/AI

💵 Q4 Revenue $2.31b, up 58% YoY

💵 FY Revenue $7.1b, up 52% YoY

💰 Q4 Operating Income $446m, up from $55m YoY

💰 FY Operating Income $897m, up from a loss of $46m YoY

📈 Q4 Operating Margin 19%, up from 4% YoY

📈 FY Operating Margin 12.7%, up from -1% YoY

For all of the attention given to AMD’s data center operations in their Q4 earnings announcement, you could be forgiven for thinking that it’s the only good news the company has to speak about today. But, in fact, the client segment of AMD’s business operations has been undergoing a boom of its own, that has seen AMD’s revenues and operating margins within this business finally and fully rebound from the client contraction that started almost two years ago.

For Q4’24, AMD booked $2.31b in client revenue, which is up 58% YoY, setting a new record high for the group for the first time since Q2’22. More significantly still, AMD’s operating metrics are all vastly improved: the company’s operating margin has gone from 4% in Q4’23 to 19% in the most recent quarter. And on a yearly basis the company has swung from an operating loss to a more-than-respectable (albeit not data center level) operating profit of $897m for the year.

Driving these gains, AMD is citing strong demand for both Ryzen desktop (Ryzen 9000) and mobile (Ryzen AI 300) processors. The company launched its first Zen 5 generation client processors in the second half of 2024 for both desktop and mobile, which has been driving higher revenues and higher profit margins. Of particular note, according to AMD the company believes that it hit a record OEM PC sell-through share for Q4, thanks in part to the Ryzen AI 300 ramp. It should be noted that AMD also stated the demand for its new high-performance gaming CPUs was so strong that it was a struggle to keep them in stock and are still catching up with demand into Q1. Also, one question was posed as to whether the macroeconomic concerns (administration, tariffs) had caused accelerated sell-through in Q4 as reported by competitors, that might lead to a weaker Q1 - AMD stated that they hadn’t seen any evidence that this was the case.

Past this, AMD isn’t offering much in the way of direct commentary on client sales performance for FY2024. The company seems to have had a banner year in terms of sales, and is happy enough to leave it at that for the purposes of its financial earnings report. With higher client revenues AMD has finally gotten ahead of its costs for the client segment, allowing for the client segment to once again be a meaningful contributor to AMD’s overall profitability.

As for AMD’s 2025 client products, the company is currently focused on the recent launch of the rest of its Zen 5 Ryzen products, which were launched back at CES and include the Ryzen AI Max (Strix Halo), Ryzen 9000X3D, and Ryzen Z2 processors. And while AMD has their Zen 6 architecture in the works, the company is being all but mum for the time being.

Fittingly, AMD’s projections for client sales for the rest of the year are also a bit conservative. AMD expects to grow client revenue well ahead of the market as a whole, but with the total addressable market for client PCs only expected to grow by a “mid-single digit percentage,” AMD is not making any promises of repeating their impressive 2024 gains.

Gaming: Radeon, Consoles

💵 Q4 Revenue $563m, down 59% YoY

💵 FY Revenue $2.6b, down 58% YoY

💰 Q4 Operating Income $50m, down from $224m YoY

💰 FY Operating Income $290m, down from $971m YoY

📈 Q4 Operating Margin 16%, up from 9% YoY

📈 FY Operating Margin 11%, up from 16% YoY

While Q4’24 and FY2024 have been great for AMD overall, it has not been an even period for all of the company’s business units. The gaming unit, which encompasses AMD’s semi-custom APU sales for consoles as well as their Radeon video cards, has been a laggard all year, and Q4 has not improved on this. Thanks to a drop in sales for both console APUs and video cards, AMD’s gaming segment has delivered one of its worst Q4 performances in years, and even compared to a regular cycle, but there is a reason for this.

By the numbers, AMD booked $563m in gaming revenue for the quarter, which was down 59% YoY. The business unit’s operating income has also dropped significantly as well, coming in at just $50m, less than one-quarter what it was a year ago. The one silver lining in all of these figures, at least, is that AMD’s operating margin for the quarter has improved significantly to 16%, which even with these reduced sales is enough to keep the business unit in the black on an operating basis.

As with Q3, the big problem here is that demand for all of AMD’s gaming products remains low. Microsoft and Sony have both kept APU orders to a minimum for much of the past year, as they’ve been working to normalize their own channel inventories. The companies over-purchased post pandemic, and are now shoring up those numbers. AMD expects the console cycle to return to its regular ‘6th year’ position.

(Note from Ian: I asked if anything is being planned ahead of a GTA6 release, expected in Q4 or if we’re unlucky, Q5. Normally a GTA release drives console sales, however no additional insight was provided.)

Meanwhile on the Radeon side of matters, AMD has continued to lose market share to NVIDIA. Coupled with that, the current Radeon RX 7000 series of products have become dated and are going to be replaced shortly, leading to very soft video cards in what is otherwise a seasonally strong quarter for these kinds of products.

The good news, at least, is that AMD’s gaming segment should be nearing the bottom of its decline. On the console APU front, AMD believes that Microsoft and Sony are finally done normalizing their inventory, and that semi-custom APU sales should pick back up in 2025 and return to “more historical patterns” in 2025.

Meanwhile on the video card front, AMD is preparing to launch its next generation Radeon RX 9000 video cards in March. Based on AMD’s RDNA 4 architecture, the updated video cards should significantly improve AMD’s competitiveness in this market with better ray tracing and AI performance, though ahead of the launch there are some questions about what kind of margins AMD can attain. Regardless, cards were already spotted to be trickling into retailers early in Q1, so AMD seems to be on track to have plenty of inventory ready for next month’s launch.

Embedded - Xilinx, AMD Embedded

💵 Q4 Revenue $923m, down 13% YoY

💵 FY Revenue $3.56b, down 33% YoY

💰 Q4 Operating Income $362m, down from $461m YoY

💰 FY Operating Income $1.42b, down from $2.63b YoY

📈 Q4 Operating Margin 44%, up from 39% YoY

📈 FY Operating Margin 40%, up from 49% YoY

The other laggard among AMD’s business units for Q4’24 and FY2024 has been the company’s embedded business unit. Covering AMD’s Xilinx products as well as embedded versions of their CPUs/APUs, the embedded unit has faced its own headwinds over the year, primarily continued post-pandemic inventory digestion. The embedded market is often slower than the consumer markets in dealing with this, however last quarter AMD said they expected a corner had been turned.

For the most recent quarter, AMD booked $932m in embedded revenue, which was down 13% year-over-year. Similarly, AMD’s operating income has dropped over the past year, sliding from $461 to $362. Nonetheless, with an operating margin of 44%, Q4’24 was actually better than Q4’23 in this regard, and this reflects one of the core strengths of the embedded segment for AMD’s finances: even when it’s down, it’s still rather profitable. In fact, of all of AMD’s business units it has the higher operating margins.

Looking forward, AMD’s guidance at the end of Q4 was very similar to the end of Q3. In short, the embedded market should turn around… eventually. AMD believes they have gained market share in the adaptive computing market for 2024 overall, which isn’t paying much in the way of dividends at the moment, but would position the business unit for more significant growth once the market does pick up. As business picks up over 2025, we also expect to see more color on the growth areas. AMD did say that simulation and emulation were recovering quicker than other verticals, reducing the blow due to softness in industrial and communications.

Two key highlights for the quarter were the Versal Gen 2 product lines, one of the first to support both CXL 3.1 and PCIe Gen 6, being made available, as well as the next-generation Alveo card for high-frequency trading.

Outlook, Q1 2025

Outlook is as follows:

💵 Q1’25 Revenue, $7.1b, +/- $300m

📈 Q1’25 Gross Margins of 54% (non-GAAP)

For the first quarter of 2025, AMD is expecting another strong quarter on a seasonal basis. $7.1b in revenue for Q1 would represent around 30% YoY revenue growth for the company in what is seasonally their weakest quarter. Meanwhile, AMD is expecting to be able to maintain their recent 54% non-GAAP gross margins for another quarter.

With AMD’s recent spate of product launches in the second half of 2024, most of Q1 should be dominated by ramp-ups and continued shipments of existing products, particularly EPYC CPUs and MI325X accelerators. The quarter should also see some significant movement on the client side, with increased shipments of AMD’s latest Ryzen processor models, and at the tail-end of the quarter, the Radeon RX 9000 series video card launch.

Looking more broadly at 2025, AMD is expecting all of their business units to grow in 2025 – not just the high-flying data center and client units, but also the gaming and embedded units as well. Data center and client will remain the stand-out units, with AMD expecting strong growth in both businesses. Still, with projections of “modest” growth for the gaming and embedded businesses as well, 2025 would mark a return to simultaneous growth for all of AMD’s business units.

That said, AMD is definitely being a bit more conservative in voicing their 2025 projections. The company is calling for “strong double digit percentage” revenue growth for the year, though not being any more specific than this. Meanwhile, unlike 2024, the company isn’t offering any sales estimates for their Instinct data center GPUs. In lieu of that, the company is forecasting $5b in total AI product revenue for the year.

Beyond the paywall the Financial Analyst Q&A held after the prepared remarks.

More Than Moore, as with other research and analyst firms, provides or has provided paid research, analysis, advising, or consulting to many high-tech companies in the industry, which may include advertising on the More Than Moore newsletter or TechTechPotato YouTube channel and related social media. The companies that fall under this banner include AMD, Applied Materials, Armari, ASM, Ayar Labs, Baidu, Dialectica, Facebook, GLG, Guidepoint, IBM, Impala, Infineon, Intel, Kuehne+Nagel, Lattice Semi, Linode, MediaTek, NextSilicon, NordPass, NVIDIA, ProteanTecs, Qualcomm, SiFive, SIG, SiTime, Supermicro, Synopsys, Tenstorrent, Third Bridge, TSMC, Untether AI, Ventana Micro.

| A guest post by

|