AMD Financials Q2 and Analyst Q&A

On the up

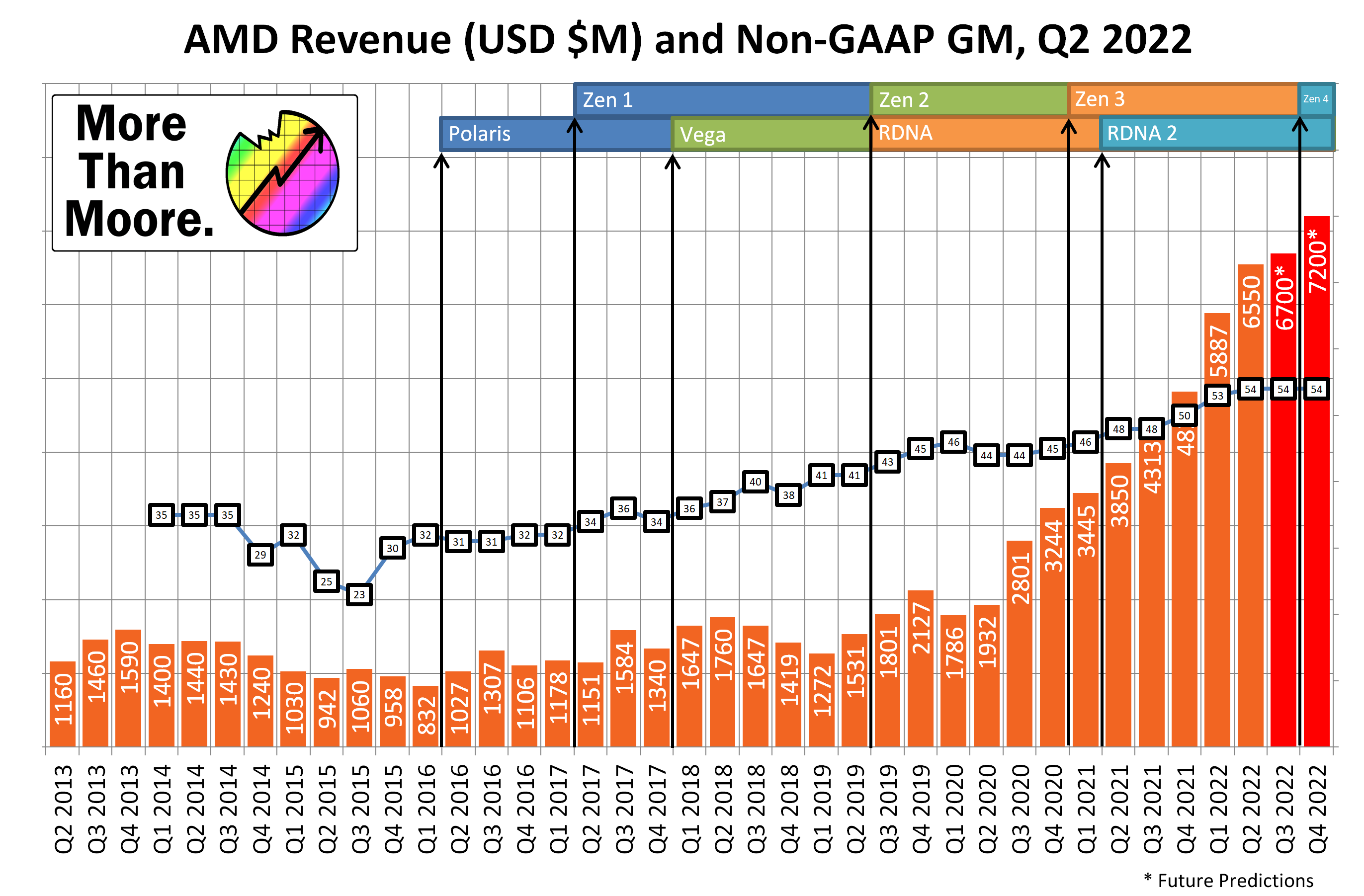

As we’re in financial season, I frequently produce graphs like this showcasing how revenue is changing with the companies I track. I post them to twitter, but also I’ll share them here.

Takeaways from the AMD Q2 Financial call, in no particular order:

5nm Zen 4 launch in Q3, Ryzen (desktop) and Genoa (server)

RDNA 3 launch in Q4

AMD is still supply constrai…