AMD 2025 Q1 Financials

Solid Momentum and Outlook, Despite New Export Rules

Coming into 2025, AMD has been firing on all cylinders. With a new CPU architecture and a new client GPU architecture in their portfolio, and a new server GPU architecture to follow later this year, AMD is in the process of overhauling most of its product stack in a big way. And, judging from AMD’s Q1 2025 financial performance, its customers are liking what they’re seeing, as AMD’s revenue and profitability is once again up significantly over the year-ago quarter, making this AMD’s best Q1 performance ever.

As has been the case for nearly two years now, driving much of these gains for Q1 is the exploding performance of AMD’s Data Center business unit – and specifically, the company’s AI processors. Late 2024 saw the launch of the mid-generation refresh MI325X series of accelerators, which incorporated newer HBM3E memory for higher memory capacities and greater memory bandwidth. And while AI parts still have an outsized impact on AMD’s overall profitability due to their high margins, AMD’s client offerings have been no slouch, either, leading to AMD recording double-digit year-over-year revenue growth in both of its major business units. AMD also saw a much better than expected seasonality in its client business, which may lead to some interesting FY outlook.

Key Takeaways (GAAP)

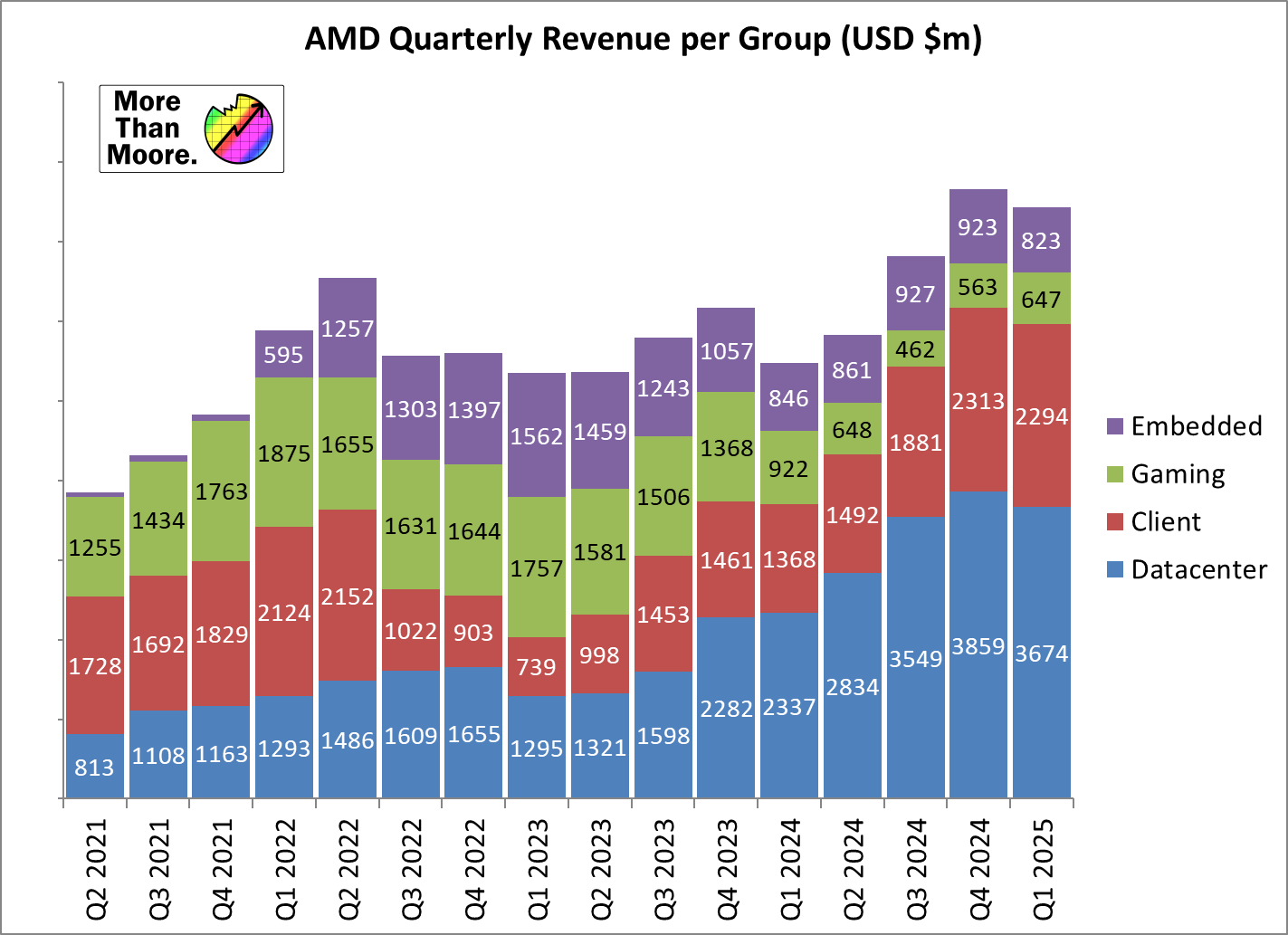

💵 Q1 Revenue, $7.44b, up 36% YoY from $5.47b and down 3% QoQ

📈 Q1 Gross Margin at 50%, up 3pp YoY and down 1pp QoQ

💰 Q1 Net Income of $709m, up 476% YoY from $123m and up 52% QoQ

🪙 Q1 EPS $0.44, up 52% YoY, up 529% QoQ

Financial Overview

Diving into the numbers, Q1 is traditionally the industry’s slowest quarter, and AMD is no exception. But even with that quarterly drag, AMD has once again closed the books on a record Q1 for the company, booking $7.44b in revenue. Compared to Q1’24, AMD has grown revenue by 36% in a single year on the back of significant growth in both Data Center and Client product revenue. This growth has cascaded down to AMD’s overall profitability and margins as well – the company locked in a (GAAP) gross margin of 50% for the quarter, with a total net income of $709m, a mere 476% better than the year-ago quarter.

Otherwise, on a quarterly basis, things were more subdued due to the aforementioned seasonality. Still, with revenues down just 3% versus Q4, AMD has been able to shrug off the usual Q1 nadir. And AMD’s net income situation looks even better: despite the softer revenues, net income is still up some 47% to $227m over Q4.

AMD’s non-GAAP performance tells a similar story. 54% gross margins paint AMD in a very favorable light, and even after shedding the numerous one-off charges that come with GAAP requirements, AMD’s core businesses are generating significantly more net income than the year-ago quarter, with a $1.57b non-GAAP net income marking a 55% improvement over the year-ago quarter.

Still, in the GAAP world AMD’s finance sheets carry many of the same kinds of charges that have hindered their GAAP profitability over the last few quarters. The company is continuing to take amortization charges for acquisition-related intangibles (i.e. Xilinx) – this time for $567m – as well as $364m in stock-based compensation. All told, AMD’s “all other” category that records these charges took an operating loss of $950m for the quarter, a bit less than the usual $1b+ in costs that we’ve seen the last few quarters. Thankfully for AMD, their continued prodigious growth is more than offsetting these changes – and making them a relatively smaller problem overall – but AMD remains an unusual tech company for its significant non-core expenses.

Data Center: EPYC, Instinct

💵 Q1 Revenue $3.67b, up 57% YoY

💰 Q1 Operating Income $932m, up from $541m YoY

📈 Q1 Operating Margin 25%, up from 23% YoY

Now the cornerstone of a modern AMD, the data center business was once again the stand-out performer for the quarter. With an operating margin of 25% coupled with the highest revenues of any AMD business segment, data center continues to drive much of AMD’s revenue and profitability growth.

By the numbers, AMD booked $3.68b in revenue under its data center group for Q1’25, which was up 57% YoY. Operating income was up by even more, with AMD recording $932m in operating income for the group, up 72% from the year-ago quarter.

While AMD doesn’t provide a detailed breakout of EPYC (CPU) versus Instinct (GPU) sales, the high-level comments from AMD indicate that both product lines are still seeing significant growth. With the former, AMD is in the middle of ramping their EPYC 9005 Turin chips, which are built on top of AMD’s Zen 5 CPU architecture. These parts launched late in 2024, and thus with their long ramp time they’re still well in the process of building platforms with customers here at the start of 2025. Though, as eyed by Ian when looking over AMD’s prepared statements, there are signs that the Turin ramp is moving slower than normal for AMD: AMD’s commentary mentions the “initial wave of instances” and how the company expects (in future tense) “more than 150 Turin platforms”. In other words, AMD’s commentary around Turin is mostly forward-looking rather than looking backwards as you’d expect for a product shipping in high volumes. Since Turin’s launch, AMD has spoken about a market mix of 4th Gen and 5th Gen parts, expecting both to exist concurrently based on performance and TCO competitiveness as Turin executes.

Speaking of products that are still ramping, there is also the mid-generation refresh Instinct MI325X. The follow-up act to AMD’s groundbreaking MI300 series, MI325X is a modest (but important) memory upgrade for the family of server AI chips. AMD’s prepared comments on the Instinct line are that it’s continuing to ramp, though they have little else to say about the new chip specifically, spending the rest of their ink on the broader MI300 lineup. While a stronger product overall than MI300, it remains to be seen if MI325X will achieve the same kind of market penetration as the initial MI300 series. With the MI350 series set to launch mid-year (recall that AMD announced in Q4 that they were pulling it in from 2H 2025), there is the risk that AMD’s customers will hold off a couple more quarters for the more substantially upgraded chip.

On which note, AMD has reiterated that MI350 will be launching mid-year. The company began sampling the chips to customers in Q1, which puts them on-track for their mid-year launch. Though we’re expecting this to be another slow ramp-up part, so while MI350 will be an important technology milestone for AMD, its impact on AMD’s revenue is going to be limited until Q4.

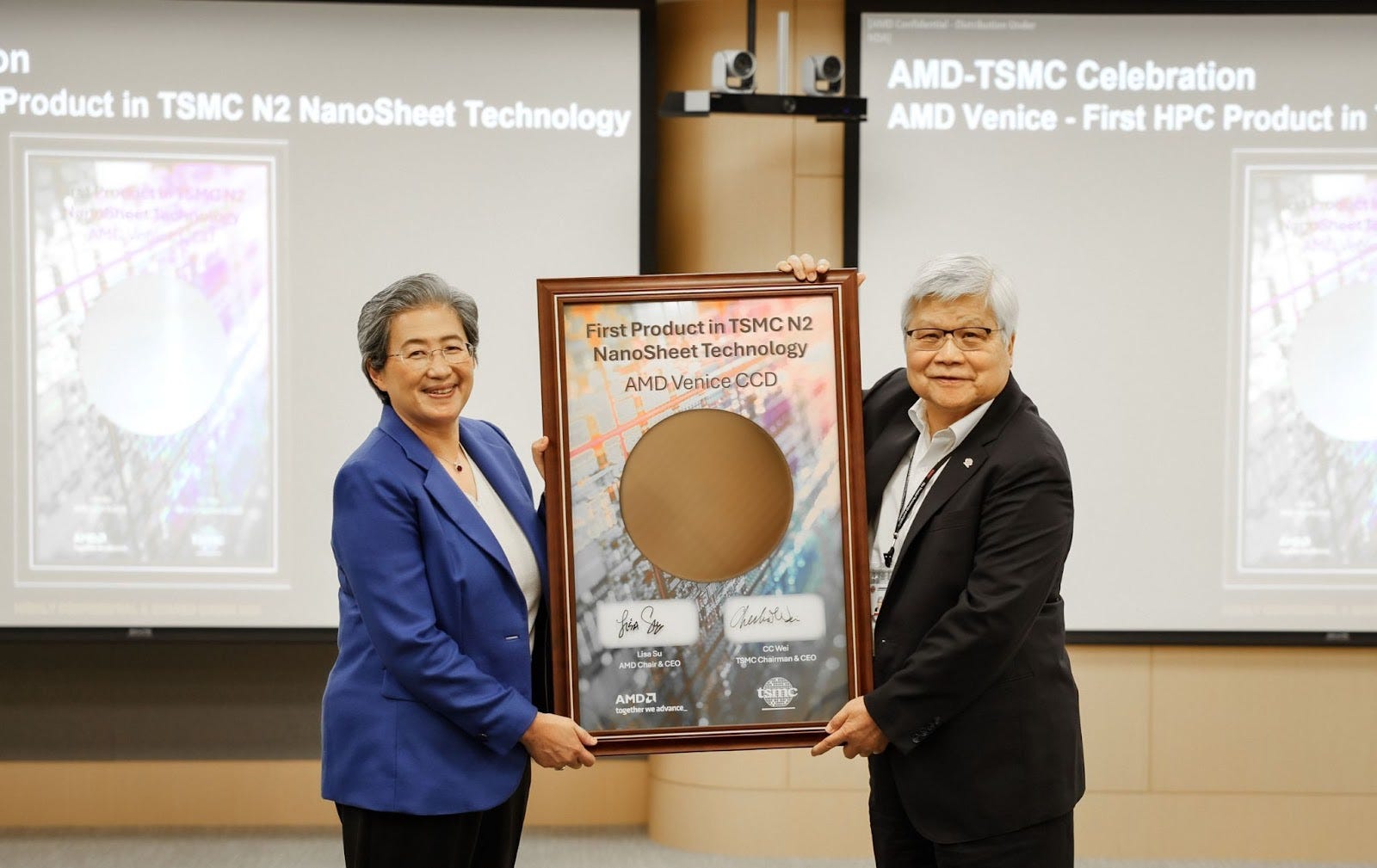

And not to be left out, the already-ramping Turin also marked a new milestone as of last month. TSMC’s Arizona fab has started minting core complex dies (CCDs) for AMD’s Turin processors, marking the first time in several years that a US fab has built server CPU cores for AMD. The first shipments of those domestic dies will take place in the second half of this year. At the same time, AMD also mentioned it will be the lead compute partner for the next generation Zen 6 compute dies built on TSMC N2, due in 2026.

Finally, AMD offered a brief update on its acquisition of ZT Systems, the high-performance server builder. The acquisition itself closed at the very end of Q1, and now AMD is focused on executing the post-acquisition phase of their plan: splitting and selling off ZT’s manufacturing operations. According to AMD, they’ve received “significant interest in ZT’s manufacturing business” and they expect to announce a buyer shortly. While that occurs, AMD has said that revenue from ZT’s manufacturing business will remain separate from the main revenue item and listed under ‘discontinued operations’ - starting from Q2 financials given when the acquisition closed. AMD is expecting $50m of operating expenses due to retained employees transitioning into their new roles.

Client and Gaming: Ryzen, Ryzen Mobile/AI, Radeon, Consoles

💵 Q1 Revenue $2.94b, up 28% YoY

💰 Q1 Operating Income $496m, up from $237m YoY

📈 Q1 Operating Margin 17%, up from 10% YoY

The core of AMD’s classic business operations, AMD’s client business unit has been undergoing an upswing of its own on the back of the strong performance of its Zen 4 and Zen 5 architecture products.

Client revenue is typically impacted by traditional Q1’s relatively weak sales after the holiday season, but for Q1’25 AMD was able to shrug off that seasonality entirely, outright growing revenue by a small degree on a quarterly basis. As a result, AMD was able to book $2.94b in client revenue for Q1’25, a 28% year-over-year improvement. And the business unit’s operating profitability has improved substantially too, with the operating margin jumping from 10% to 17%, pushing the unit’s operating income up by 109% to $496m.

Driving a lot of this has been the ramp of AMD’s various Zen 5-based chip offerings. Though the architecture launched last year, AMD has been expanding the number of SKUs offered, as well as launching new chips based on the technology such as the Ryzen AI Max (Strix Halo) chips. Based in part on these new products – and in particular high-margin desktop and mobile chips – in Q1 AMD set a new record for client CPU average sales prices (ASP). AMD later clarified that in total units, Q1 was down compared to Q4, but the higher ASP resulted in a net sequential gain for the client business. Compared to previous quarters, this is a steady and well-earned improvement for AMD. But looking at the bigger picture and where AMD was several years ago when its client CPU ASPs were nothing short of dire, it’s a remarkable turnaround for the company.

Meanwhile, the other big launch for AMD’s client business unit has been in its GPU division, which in Q1 released the company’s highly-anticipated Radeon 9070 series video cards. Based on the company’s new RDNA 4 architecture, the new Radeon cards have been a critical and financial success story for the company. According to the company, this ended up being a record-setting launch for AMD, with the first week sell-out besting AMD’s previous best Radeon launch by “more than 10x.” And with demand for the cards reportedly remaining strong, AMD’s focus is now on helping their board partners replenish their inventories to keep cards available on store shelves and to meet the overall demand. One question perhaps not addressed was the potential market share gain if AMD had enough inventory to meet demand, but given the update cycle, it’s still a positive to see such high demand for a new generation of products.

It’s fitting, as well, that this is also the first quarter that AMD has begun combining its gaming and client segments, which were previously reported as entirely separate business units. Going forward, the gaming segment is now part of the broader client segment – making the Client and Gaming Segment – which houses everything from Ryzen CPUs to Radeon GPUs to console SoCs. The net impact of this, beside chopping a slide off of AMD’s quarterly slide decks, is that the operating income for the gaming segment is no longer broken out and reported. While AMD is still breaking out revenue by client and gaming for the moment (expect this to eventually go away as well), operating income is being reported solely for the larger client and gaming segment.

For the moment, at least, even with all of these changes AMD is still co-mingling Radeon sales with semi-custom SoC sales in its financial reports, which makes for an especially odd pairing this quarter. While Radeon sales are setting new records, the larger “gaming” segment has seen its revenue drop significantly over the year-ago quarter, declining from $922m to $647m. As with Q4, the blame for this is being placed primarily on the semi-custom SoC business, which remains exceptionally soft. AMD’s clients are still slowly burning through their ship inventories, which has meant that AMD has been unable to sell them much in the way of additional chips.

But, according to AMD, there is a light at the end of the tunnel. Channel inventories for consoles have finally normalized, and to that end the company is expecting semi-custom sales to grow in Q2. If this comes to pass, this would not only break the console SoC malaise, but it would buck seasonality altogether by growing sales in what’s historically a flat quarter for the semi-custom group.

As an aside, even with recent economic turmoil and tariffs leading to higher prices for PCs and game consoles alike, AMD currently expects to weather the storm relatively well. Client products have continued to sell despite the headwinds this creates, and so far, AMD doesn’t expect there to be significant problems here – though this may just mean that growth is handicapped, rather than driving sales backwards entirely. AMD claims to have good visibility into its customer base, and isn’t seeing any panic buying to build inventory at this time.

Embedded - Xilinx, AMD Embedded

💵 Q1 Revenue $823m, down 3% YoY

💰 Q1 Operating Income $328m, down from $342m YoY

📈 Q1 Operating Margin 40%, up from 41% YoY

Covering AMD’s Xilinx products as well as embedded versions of their CPUs/APUs, the embedded unit has faced its own headwinds over the last several quarters, primarily continued post-pandemic inventory digestion. The embedded market is often slower than the consumer markets in dealing with this, and while AMD turned the corner back in Q4, the recovery here remains pretty slow.

For the most recent quarter, AMD booked $823m in embedded revenue, which was down 3% year-over-year. Similarly, AMD’s operating income has dropped over the past year, sliding a bit from $342m to $328m. Nonetheless, with an operating margin of 40%, the embedded segment remains AMD’s single highest margin segment. As a result, even when it’s down, it’s still rather profitable.

At this point, AMD expects the embedded segment to finally return to growth in the second half of the year, primarily on the backs of the Test and Measurement, Communications and Aerospace markets. Helping to drive this return to growth will be, in part, new chips from the former Xilinx operations, with AMD reporting that they have completed initial shipments of both their latest budget Spartan UltraScale+ FPGAs, as well as the second-generation of Versal AI Edge SoCs.

Outlook, Q2 2025

Outlook is as follows:

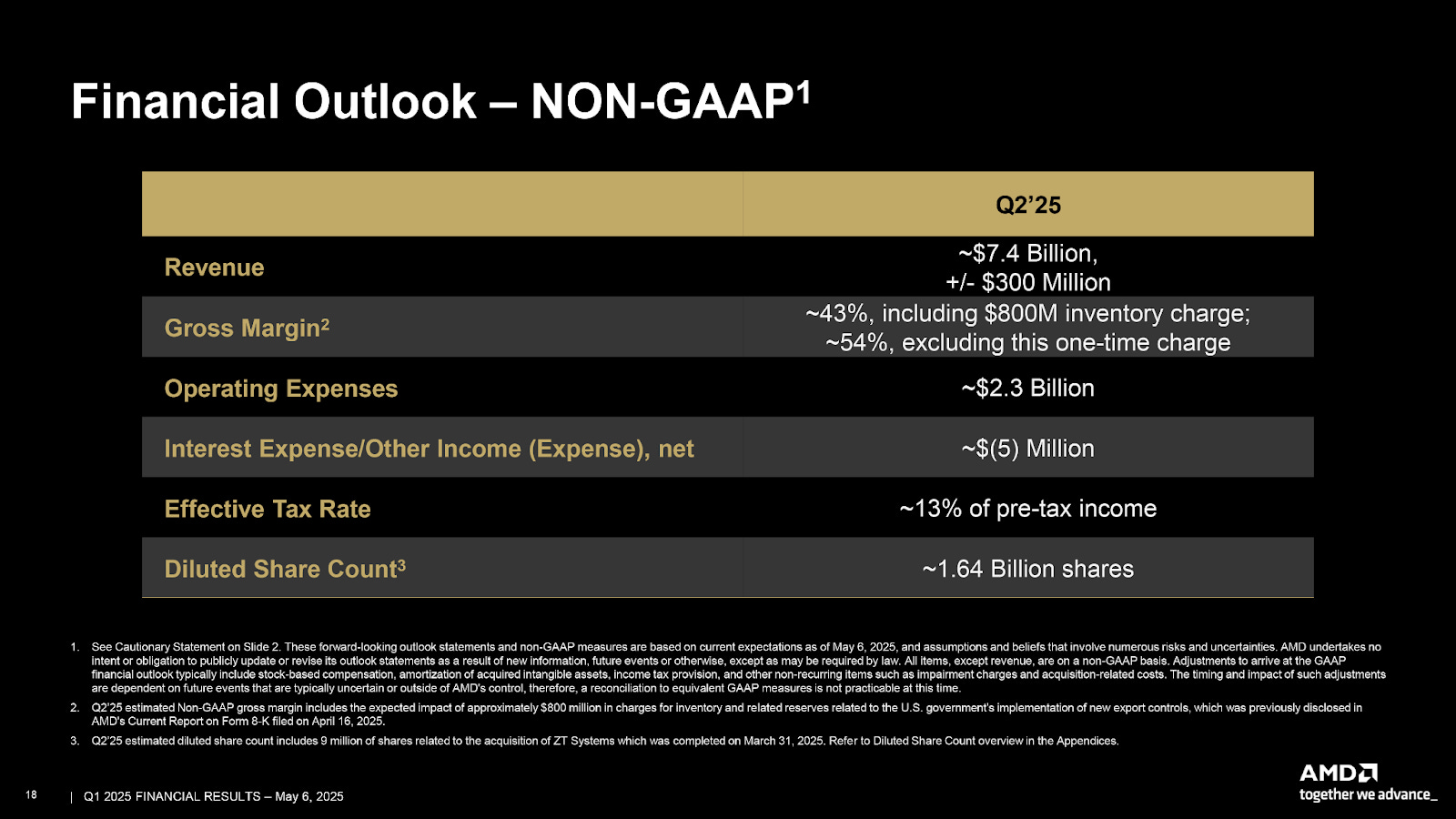

💵 Q2’25 Revenue, $7.4b, +/- $300m

📈 Q2’25 Gross Margins of 43% (non-GAAP), or 54% excluding the MI308X write-down

For the second quarter of 2025, AMD is expecting another strong quarter on a seasonal basis. $7.4b in revenue for Q2 would represent around 27% YoY revenue growth for the company in what is typically their second-slowest quarter of the year.

Gross margins for Q2’25 will be a bit thornier than usual for the otherwise resurgent AMD, however, as the company recently revealed that it is going to have to take a significant charge in relation to export controls on its high-end Instinct MI308X accelerators. As disclosed by the company a few weeks ago in an 8-K filing, the United States has placed fresh export controls on high-end AI accelerators, which in turn have all but halted the continuing sales of AMD’s Instinct MI308X accelerator. Specifically designed for the Chinese market to meet the previous export restrictions, the MI308X is now itself banned for exporting to China as well.

Consequently, AMD is going to have to take $1.5b in changes this year for inventory, purchase commitments and reserves. These charges will take place mostly over two quarters, with AMD taking $800m in charges in Q2, and then a further $700m in charges in Q3. Thus far the company has not disclosed just what has (or will be) done with the MI308Xs that were already in production, but even with their restricted utility someone, somewhere, undoubtedly has a use for the accelerators. AMD is presumably preparing to sell the accelerators to new clients, albeit at reduced prices.

(Ian: it’s worth noting that Deepseek V3 was trained using cut-down versions of NVIDIA chips with reduced networking, and so a smarter way of networking for AI inference was developed for that situation to overcome the deficiencies - if there’s any company that understands enabling innovation due to being put in a limited box, it’s AMD, so I’m sure the MI308X will find a home with some innovative enterprise)

Getting back to AMD’s financials, then, these write-downs will be dogging AMD’s gross margins for the next two quarters, to the point where AMD is going so far as to break down their non-GAAP gross margin outlook to both include and exclude the charges. With the MI308X changes included, AMD is expecting its non-GAAP gross margin for Q2 to be just 43%. Otherwise, if the MI308X charges are excluded, then they’d be looking at a 54% gross margin. MI308X quantity was significant, to say the least.

Interestingly, despite all of this, the impact to AMD’s revenues will be more muted. According to the company, it still expects data center GPU sales to still grow by double-digit percentages for 2025. Otherwise, data center GPU revenue growth will come to a halt in Q2 – it’s unclear if this means revenue will be flat or will outright decline – while data center GPU revenues will quickly return to year-over-year growth in Q3. So, although the MI308X situation is a pain for AMD, the company has grown enough and is diversified enough that it’s not going to be a major blow to the company.

Otherwise, AMD’s Q2 should largely be defined by continued ramp-up of new products across the spectrum, including Instinct MI325X accelerators, EPYC Turin CPUs, and AMD’s latest generation of Ryzen client processors. Even the semi-custom side of the business is looking towards an improved quarter, with an expected return to revenue growth there.

Five Key Takeaways

🏆 Best Q1 ever, with record revenue and profitability.

🧠 Data center revenue dominated by AI, and continues to grow.

🎮 Client and gaming have momentum fueled by competitive parts and high ASPs.

🧩 Embedded segment is still digesting, but recovery expected in H2.

📊 Q2 and FY outlook is strong despite the China AI export rule change.

Beyond the paywall the Financial Analyst Q&A held after the prepared remarks.

More Than Moore, as with other research and analyst firms, provides or has provided paid research, analysis, advising, or consulting to many high-tech companies in the industry, which may include advertising on the More Than Moore newsletter or TechTechPotato YouTube channel and related social media. The companies that fall under this banner include AMD, Applied Materials, Armari, ASM, Ayar Labs, Baidu, Dialectica, Facebook, GLG, Guidepoint, IBM, Impala, Infineon, Intel, Kuehne+Nagel, Lattice Semi, Linode, MediaTek, Next Silicon, NordPass, NVIDIA, ProteanTecs, Qualcomm, SiFive, SIG, SiTime, Supermicro, Synopsys, Tenstorrent, Third Bridge, TSMC, Untether AI, Ventana Micro.

| A guest post by

|